US ECONOMICS

CORONAVIRUS

U.S. Department of State. 04/15/2020. Secretary Michael R. Pompeo’s Call with New Zealand Foreign Minister Peters

The following is attributable to Spokesperson Morgan Ortagus:

Secretary of State Michael R. Pompeo spoke with New Zealand Foreign Minister Winston Peters today. Secretary Pompeo thanked Foreign Minister Peters for New Zealand’s support for repatriating American Citizens. Secretary Pompeo and Foreign Minister Peters emphasized the importance of U.S.-New Zealand and international coordination to contain the COVID-19 pandemic and to address the public health risk caused by the outbreak. The two also discussed the importance of a strong international response to the outbreak in the Indo-Pacific region.

U.S. Department of State. 04/15/2020. Secretary Pompeo’s Call with Australian Foreign Minister Payne

The below is attributable to Spokesperson Morgan Ortagus:

Secretary of State Michael R. Pompeo spoke with Australian Foreign Minister Marise Payne today about the continued strong U.S.-Australia and international coordination to contain the COVID-19 pandemic. The two highlighted the importance of increased vigilance and cooperation to prevent a deterioration of the security and health situation in the region, particularly in Southeast Asia. Secretary Pompeo thanked Foreign Minister Payne for Australia’s support for repatriating American citizens, not just from Australia but from all around the region.

U.S. Department of State. 04/16/2020. Secretary Michael R. Pompeo With Martha MacCallum of Fox News. Michael R. Pompeo, Secretary of State

QUESTION: All right, so we begin this evening. We’re glad to be joined by Secretary of State Mike Pompeo. Secretary Pompeo, thank you very much for being with us tonight. Your thoughts, I guess first of all, just your reaction to that story and that question from John Roberts. What do you say to that?

SECRETARY POMPEO: Well, Martha, thanks for having me on the show tonight. The mere fact that John had to ask the question, the mere fact that we don’t know the answers, that China hasn’t shared the answers, I think is very, very telling. To your point, the President said that there are multiple sources. What we do know is we know that this virus originated in Wuhan, China. We know that there is the Wuhan Institute of Virology just a handful of miles away from where the wet market was. There’s still lots to learn. You should know that the United States Government is working diligently to figure this out.

But what we really need, Martha, we really need the Chinese Government to open up. They say they want to cooperate. One of the best ways they could find to cooperate would be to let the world in, to let the world’s scientists know exactly how this came to be, exactly how this virus began to spread.

Today you saw further evidence that there were days – days that went by – from when the Chinese Communist Party, the leadership there, knew about this virus before they told the public writ large. That’s dangerous. A lot of cases, a lot of movement, a lot of travel around the world before the Chinese Communist Party came clean about what really transpired there.

These are the kind of things that open governments, democracies don’t do. It’s why there is such risk associated with the absence of transparency. We need it still today.

QUESTION: I mean, it’s hard to imagine, giving everything that so many countries have been through, how different it might have been if China had immediately been clear about what they knew about the origin of this virus and if they had shut down all of the travel at that point. There were tens of thousands of people who flew out of the Wuhan area after that point. So how does this not have a very negative, heavyweight impact on our relationship with China going forward?

SECRETARY POMPEO: Well, Martha, I’ll say this. I’ve talked to my counterparts all across the world over the past handful of days. They all see this too. It’s very difficult to make the case that there was anything but absence of shared information in a timely fashion. It didn’t just put Americans at risk; it put people all across the world at risk. It wasn’t until the end of January when we brought the first Americans home, the roughly 800 people that we got back from Wuhan itself. They were at risk for an awfully long time.

The Chinese Government needs to come clean. It needs to be accountable. It needs to explain what happened and why it is the case that that information wasn’t made more broadly available. We could have done things differently. The world would have responded quickly. Frankly, the international health organizations didn’t do us any favors either in making sure this information was broadcast in a way that it needed to be with transparent and full information.

QUESTION: Yeah. I mean, the President has made a lot of effort to be very supportive of his friendship and his relationship with President Xi, even on January 24th saying that he hopes it works out well, he appreciated the efforts and the transparency on the part of the Chinese Government, he wanted to thank President Xi for that. I mean, can those kind of statements go forward anymore? I know the President talks a lot about the trade deal and making sure that they don’t renege on their promises there. It almost feels like that’s the one piece that is holding that relationship together at this point, because we’re counting on those trade agreements and those trade relationships with China.

SECRETARY POMPEO: Well, we’ve seen the President be serious about righting the disaster that was the trade relationship before he came to office. He’s made it more fair and reciprocal. We have an expectation that they will live up to their obligations under the phase one trade deal. It was a good deal for both parties.

As for the relationship, we want to cooperate. It’s 1.5 billion people in China. We want the Chinese people to be successful. But it requires leadership that’s prepared to engage in the international community on a fair and reciprocal basis and to share information the way we expect every nation to do that. It doesn’t appear that that happened here. The President talked about their data today and he asked if anybody believed the numbers of deaths and the numbers of cases inside of China.

But that’s the kind of doubt and uncertainty that happens when you close down, when you kick journalists out of your country. All we’re asking is for the Chinese to cooperate and share that information with us. It would be very helpful to the United States. It’d keep us safe. Frankly, it’d keep the Chinese people safer too.

QUESTION: Do you trust what you hear from the Chinese officials when you deal with them?

SECRETARY POMPEO: It varies. I try to take them at their word, but we’re always in every relationship we have trying to make sure we verify everything. It’s not about words; it’s about actions. We need to make sure that every country lives up to the commitments that they made.

QUESTION: So I want to ask you about these cables, this story that came out a couple of days ago in The Washington Post by Josh Rogin that said that there were cables that were highlighting very big concerns about what was going on in these Wuhan labs, that they felt that there weren’t enough people there given the highly contagious and dangerous materials that they were dealing with with these bats and these viruses. They said that it was highly likely that a pandemic could result from how mishandled everything was there.

What happened to those cables? Who received them in the State Department? Who went over them in the State Department two years ago?

SECRETARY POMPEO: Martha, I appreciate you want to ask about that. I can’t comment on the cables tonight. I can say this. This is a laboratory that contained highly contagious materials. We knew that. We knew that they were working on this program. Many countries have programs like this. And in countries that are open and transparent, they have the ability to control and keep them safe and they allow outside observers in to make sure all the processes and procedures are right. I only wish that that had happened in this place. We would know more about it and we would know more about what has transpired there, if anything, today.

QUESTION: Is that something that you’re looking into, what happened with those bits of information and who followed up on them?

SECRETARY POMPEO: Absolutely, Martha. We’re doing a full investigation of everything we can to learn how it is the case that this virus got away, got out into the world, and now has created so much tragedy, so much death here in the United States and all around the world, and at enormous cost to the global economy as well.

QUESTION: Yeah. I mean, one person who is obviously also very involved in world health is Bill Gates. He takes issue with the American decision, the President’s decision, to stop funding them at least temporarily until we get some answers on all of this. Here’s what he said: “Halting funding for the World Health Organization during a world health crisis is as dangerous as it sounds. Their work is the spread of COVID-19 and if that work is stopped no other organization can replace them. The world needs the WHO now more than ever.”

What do you say to that, given the President’s decision?

SECRETARY POMPEO: Well, what the world needs is an institution, an organization, that actually delivers on the mission set, right? The thing the President – caused the President to make this decision was the fact that the World Health Organization didn’t do that, that for an awfully long time it said that there wasn’t a pandemic, it delayed announcements about things that it knew inside of China that were going on. That’s about politics, not science. We need a scientific organization that is engaged in the medical, epidemiological, and health work that it was designed to do. The President has now put a pause on funding. We’re going to evaluate how best that this mission be executed and is designed to make sure we protect America and protect American taxpayers too.

QUESTION: Yeah. Before I let you go, I want to ask you about this Iranian Islamic Revolutionary Guard Corps vessels that have conducted what are called dangerous and harassing approaches to several U.S. warships in the Persian Gulf, coming as close as 10 yards away. We have some video that we’re showing right now. What can you tell us about what happened here and what the ramifications of this will be?

SECRETARY POMPEO: I’ll leave it to the Department of Defense to talk about the details of that, but we have seen this before where the Iranians behaved in ways that were inconsistent with international law. I think the American people know that President Trump is serious about protecting Americans, protecting our military, protecting our Navy. I am very confident that we’ll make decisions that do that. And I’ll leave it to the Department of Defense to talk about the details of how we’re thinking about that at this point.

QUESTION: All right. Any State Department discussion on that at this point with you and the Defense Department or with Iran for that matter?

SECRETARY POMPEO: Oh yes, we’ve talked as a team. We’ve talked across the interagency. We’re evaluating how best to respond and how best to communicate our displeasure with what took place.

QUESTION: All right, we’ll be watching.

SECRETARY POMPEO: Thank you, Martha.

QUESTION: With all of this virus going on, there’s a lot of other things going on in the world too, so we appreciate you responding to that. Secretary Pompeo, good to see you tonight. Thank you very much, sir.

SECRETARY POMPEO: Thank you, Martha. You have a wonderful evening, ma’am.

QUESTION: You too. Stay well.

ENERGY

U.S. Department of State. 04/15/2020. Briefing with Assistant Secretary for Energy Resources Francis R. Fannon On U.S. Diplomacy in Oil Markets. Francis R. Fannon, Assistant SecretaryBureau of Energy Resources. Via Teleconference

MS ORTAGUS: Hey, thank you so much. Good afternoon, everybody. Hope everyone’s healthy, doing well. Welcome to our Wednesday daily briefing. Thank you – thanks for joining us. With me today I have my friend, Assistant Secretary Frank Fannon, who many of you have already met. He leads our Bureau of Energy Resources. Just a reminder that today’s call is on the record but it is embargoed until the end of the call.

Today we’ll be discussing the announcement over Easter weekend that the world’s largest oil producers have agreed to an unprecedented cut in output. This decision represents a major victory for the United States, President Trump, and our energy diplomacy, and it’s the product of a whole-of-government approach by the United States to support the global oil market. Assistant Secretary Fannon will begin with some opening remarks per usual and then we will take a few questions. Just a reminder to press 1 and then 0 if you would like to ask a question, and again, this call is on the record but it is embargoed until the end of the call.

Go ahead, Frank.

ASSISTANT SECRETARY FANNON: Thanks, Morgan. Thank you, everyone, for joining me on the call today. I’m delighted to be here. I’m especially pleased to share this diplomatic victory with all of you, a victory led really from the very top, from President Trump himself. Thanks to the President’s leadership, the United States was able to reach this historic energy agreement this past weekend.

We went through a rocky period of uncertainty in global oil markets over the past few weeks, but this latest deal, agreement provides an ability to restore a sense of calm, and it’s critical that we did so. Coronavirus’ effect on the global economy is severe and we still don’t know for how long. Therefore, it’s critical that the nations – that all nations take the measures to reduce market volatility, given this uncertainty, as much as possible.

This supply glut, this oil supply glut was something that was within our control, and that oversupply has affected United States companies, as is well reported, but it’s also affected other nations that disproportionately depend on oil revenues to power their economies and for their citizens. International Energy Agency has spoken to this issue and noted that some of these are fragile or near-fragile states. As such, it was critically important that the G20 nations and like-minded countries, as well as producing countries, take necessary actions.

Secretary of State Pompeo certainly recognized this situation. On March 24th he spoke with the crown prince of Saudi Arabia and it was – we have a public readout of that that was issued the following day on the 25th. But in that call the Secretary and the crown prince focused on the need to maintain stability in global energy markets amid this worldwide response to COVID-19. The Secretary stressed that as a leader of the G20 and an important global energy leader, the Kingdom of Saudi Arabia has a real opportunity to rise to the occasion and reassure global energy and financial markets when the world faces such significant economic uncertainty.

In coordination across the interagency and certainly, as I mentioned, led by the President himself and the White House, the State Department was engaged throughout the course of this last several weeks, and we’re very pleased that the kingdom went forward and called a G20 extraordinary energy ministers meeting to come to a consensus to help stabilize the energy sector. The ministers reached important cooperative agreements that allowed our work to remain – the United States work in particular – to remain market-focused and to complement the work being done by the various energy ministers from major producing states. They all acknowledged the importance of international cooperation in ensuring the resilience of energy systems and recognized that energy security is a key enabler for economic activity and a cornerstone of global market stability.

Again, the outcome of this – the last several weeks led by the President really is a huge victory for diplomacy. Our energy strength in the United States has certainly increased our ability to weigh in and affect the global energy international mechanisms to support the reduction of volatility, but also to increase our partnership, our energy partnerships with like-minded countries around the world.

I just want to underscore this important point from the deal, as it were: The U.S. has been clear that it remains a free market economy and that the U.S. production cuts – and there’s a considerable amount of media coverage on what that will look like – is a direct response to markets, not the government dictating private sector behavior.

My last in closing – again, underscore that this is a broader victory for energy resilience and confidence which really is based on the United States’s enduring innovation and ability to tap into that entrepreneurial spirit as well as our resources effectively.

And with that, I’d be happy to take some questions. Thank you.

MS ORTAGUS: Great, thanks so much. And again, it’s just 1 and 0, guys. I think you know the drill by now, but just in case.

Okay, first up in the queue we have Humeyra from Reuters.

QUESTION: Hello, Frank. Thanks, Morgan. I just wanted to ask you about how you see the oil markets going forward because the demand – the cuts in the demand is far higher than the production cuts. We’ve got 30 million barrels off and you’ve got 15 million or some sort production cuts and some of them are voluntary. And say like Fitch today, for example, says some of it may not materialize, the voluntary bit, so they expect an oversupplied market. How do you see that impacting the U.S. companies as well going forward, and can I just get your thoughts on that? Thank you.

ASSISTANT SECRETARY FANNON: Yeah, sure. Well, I guess as a general matter it’s too early to tell because if it’s – we’re trying to base – I suspect the modelers that you’re referencing are trying to model something that they have zero understanding of what’s going to happen in terms of the demand picture and the global economic recovery in the United States and elsewhere, which is why I think it was so important that the President, Secretary of State, the interagency called on this collective action, which is a measure that we can control, which is the oversupply situation.

The U.S. – I can’t speak to how some of these models eventuate, the conclusions they come to, but when you see U.S. companies cutting, idling rigs, laying down rigs, cutting CAPEX 30 percent, billions and billions of dollars of money that’s not being invested, that there’s I think a pretty clear correlation in terms of particularly short-cycle production. So I’m pretty confident from all the numbers that we were seeing, and I think just today the IEA issued its report where it’s projecting the U.S., Canada, Brazil, Norway – they have a number here – it’s going to decline 3.6 million barrels. The timing is going to be a bit variable because of the cycles of the business cycle, but I have the greatest degree of confidence in the U.S. business and the private sector to do what they need to do in response to market conditions. I mean, the entire shale revolution as it were was based out of the private sector and responding to the market. I have every confidence that the private sector will respond in the opposite direction. Thanks.

MS ORTAGUS: Great, thank you. Let’s go over to Matt Lee.

QUESTION: Hey, Morgan, thanks. And Frank, thank you. A couple things very briefly. One is when exactly do you expect to see this quote/unquote “historic deal” actually have an impact other than the price of oil continuing to decline. Again today it’s down – it’s down again. And then secondly, you’re very quick to congratulate the President and the Secretary, but in fact is it not the case that a group of lawmakers – Republican lawmakers – really were the ones who (inaudible) this to make– force the administration to take note by directly intervening with the Saudis and really, like, taking it to them? Thanks.

ASSISTANT SECRETARY FANNON: Well, I guess I was just speaking to – I can’t speak to the time horizon. I mean, Congress has a role. They’re an independent branch of government and certainly have been vocal about their — across the various policy prescriptions as well. And they have a role to play, and they certainly have played that. And I know that they continue to monitor and want to see action, so this will be an evolving situation based on the — when we all get back to work, when we can do this in person again.

But I think that the – there’s going to be a latency in terms of the supply buildup and how that works its way out. And so the market reactions on every one day, I can’t speak to that. But what we’re talking about is huge stores of a physical commodity that has amassed over time, and there’s going to be a latency effect because of the price situation sending a signal to the private sector to curb, and you’ve already seen the announcements on pulling CAPEX. There’s going to be a latency effect, so I think the system just has to work its way through as a natural evolution of that. The various – some of the other producing states will continue, and I – in terms of their future curtailments. They’ve already announced that, 23 percent reductions beginning immediately, and so I think that it’s all going to kind of work its way, but right now I think we just have this oversupply. We’ve got to get through this and then we’ll proceed.

MS ORTAGUS: Okay, Frank, did we lose you there? Are you still on?

ASSISTANT SECRETARY FANNON: I’m still here, thanks.

MS ORTAGUS: Oh, okay, good. Sorry, it sounded like it cut off for a second. Okay, Emily Meredith from Energy Intelligence.

QUESTION: Hi, Frank. Thanks for taking the time to do this. So, I wanted to ask you to put this in a bit of historical perspective. Obviously, to see President Trump helping to facilitate discussions among OPEC members is really a shift from an historical perspective. Is – do you think that this is the U.S. at a turning point where its interests are essentially the same as those of OPEC members and their allies because of the size of U.S. output, or was this more of a function of this specific moment in time?

ASSISTANT SECRETARY FANNON: Yeah, I guess – excuse me – and a lot of you and perhaps others have written about kind of the evolution of the U.S. approach to OPEC, and certainly the President in particular. What I think is this is a stark recognition that there can be some flexibility and some – an evolution of thinking because – to serve the country, and I think that’s a key component of real leadership.

The scale of the oil patch, as it were, as in the breadth of it and the direct or indirect jobs and the broader economic impact it has for the United States, is significant and I don’t think we fully appreciate its importance overall. Historically, politicians of every stripe laud low gas prices and they historically say, oh, it’s like a tax cut. But if no one’s driving, if no one has anywhere to go, it’s effectively a tax cut that has no benefit.

And so it seems like to me it’s certainly injurious to the United States, but I think it’s more – like as I mentioned before, there are a lot of countries that are dependent on oil revenues, disproportionately so, and if they lack a means to provide for themselves, then it creates a whole host of additional potential foreign policy challenges, especially if they’re near-fragile states.

So there’s a lot of I think foreign policy reasons why this deal and the forward path is so important (inaudible) why we all have to continue to monitor it and continue to maintain close collaboration across the countries, because there’s a lot at stake here. Thanks.

MS ORTAGUS: Okay, great. Let’s see, we have Stephen Cunningham from Bloomberg.

QUESTION: Given, Frank, that oil is trading below it was before the deal was announced, is there any sense that the deal didn’t go far enough or perhaps more cuts will be needed in the future? And also has the threat of tariffs and other retaliatory action been completely taken off the table?

ASSISTANT SECRETARY FANNON: Yeah, thanks. I’ve – I think I’ve spoken to the point about the time horizon. Again, these are big – these are big-scale types of endeavors. We already have supply buildups and that has to work its way through the market. I can’t speak to the daily variances of trading. That’s a different thing.

In terms of the tariffs, I think it continues to be something that’s on the table. It’s certainly something the President had weighed but he consistently said it was a lever he didn’t think he would need to pull.

So I think that where we are right now in this collaboration – it’s a really critically important time, it’s an unprecedented type of an agreement, and it’s encouraging that it was able to come together as it did. Certainly the President’s involvement was critical to that success, but it’s still something to monitor and watch, and I think we will all be monitoring it closely, constantly engaging with our partners around the world to ensure that we reduce the volatility that is in the market, we create a sense of calm and a degree of resilience as we all get through this corona-induced demand destruction.

MS ORTAGUS: Great, thanks. Okay, next we have Josh Siegel from the Washington Examiner.

QUESTION: Yes, thanks for doing the call. I appreciate it.

So my question is: I’m wondering – you spoke to the U.S. free market system earlier. As I’m sure you know, Texas had a hearing yesterday to consider prorationing and potentially forcing producers there to hold back production. Oklahoma is looking at the same in a few weeks. And yeah, one of the companies that has called for that in the shale – in the Texas shale area said that they are hearing that the Saudis did want something more official from the U.S.

I mean, in general, like, I know – I mean, obviously you’re in the federal government, but do you – I mean, what do you think of states considering these kind of ideas? Do you think that type of escalation is necessary considering the deal that just went through?

ASSISTANT SECRETARY FANNON: Yeah, thanks for the question. I kind of – when this talk was started, I was reflecting on some of Larry Kudlow’s statements on this, and I think he provides a really good direction and reminding of how the United States remains a free market economy.

But we also respect – tend to respect states’ rights, and if states – if that’s the direction some states want to go, that’s – in my view, that’s certainly outside the purview of the State Department, and that’s – if the states, whether they’re Texas or Oklahoma or others, that’s for them to kind of figure out. But at the federal level, you’ve heard time and time again the recognition that we are strong supporters of markets and market reactions. That has the best – the private sector and the market reactions are the best way forward.

MS ORTAGUS: Great, thank you. Tracy Wilkinson.

QUESTION: Thanks. I wondered if you see in this any implications for the U.S-China trade deal. Would China still be willing to buy U.S. oil or not? Would the U.S. maybe end up exporting rather than import – I mean importing rather than exporting? Do you have any thoughts about that? Thanks.

ASSISTANT SECRETARY FANNON: Yeah. I’m sorry, Tracy. I’m going to have to kind of defer on this one and refer you to some other agencies that are most closely following that. I mean, my initial thinking is if the country signed up to make certain purchases, I would think that there would be an expectation that they fulfill their commitments and those obligations. But beyond that, I’d have to defer you to other – the more trade-focused partners in the interagency. Thanks.

MS ORTAGUS: Thanks. Ryo Nakamura from Nikkei.

QUESTION: Thank you for this call. I want to ask you about your view on the demand recovery. We are now used to working from home and doing telephone conference instead of taking a drive to the office or taking a long flight to attend an international conference. Do you think those changes of our behavior would affect the demand recovery for oil? Do you think the recovery could be slower than a normal economic depression?

ASSISTANT SECRETARY FANNON: Yeah, so what you’re – I guess you’re asking do we think there’ll be a behavioral change coming through this. And I don’t have a good – I don’t have a really good sense of that, I’m sorry to share. I mean, I can just speak kind of personally, and there’s so much work that we do that really requires face-to-face meetings. I mean, if you speak to going to a conference, the actual conference agenda is just a part of that. It’s also some of the other discussions that take place.

So, I – from where I sit, I think that there will be a robust return, maybe not quite to the way things used to be because we have to – as we follow the guidance of health experts on managing exposure. But to the extent that we can, I would think that we’d be eager to get back more to the way things had been.

I know. I have three kids and they certainly want to get back to school, which I will remind them of when they complain when they go to school in some months. Thanks.

MS ORTAGUS: Thanks. Okay. Tim Tuko, Wall Street Journal. Tim, do we have you?

QUESTION: (No response.)

MS ORTAGUS: Okay. Let’s go over to Lara Jakes, then.

QUESTION: What the .

OPERATOR: Tim is open. Your line is open.

QUESTION: Right, okay. Can you hear me now?

MS ORTAGUS: (Laughter.) Yes, we can hear you.

QUESTION: All right, guys. Thanks.

ASSISTANT SECRETARY FANNON: That’s the good part, so —

QUESTION: Frank, I appreciate you doing this. I want to clarify something that you said before, because it sounded like you were saying that the private sector is going to be responsible for a glut from here. You expect private sector decisions to guide how that – that glut gets drained away.

But I want to be very clear that the deal is for 10 million barrels, demand is down somewhere between 25 and 30, there’s a real sign that all this is going to play out the same way in these oil companies, and all the OPEC-plus nations are going to look to Trump and the Trump administration to do the same thing. I don’t see how that’s avoidable.

Are you guys going to tell them the private sector will deal with this, or what is your plan when these requests come to you all again for intervention?

ASSISTANT SECRETARY FANNON: Well, the – our system works differently. I mean, do you have – I have greater faith – I have the greatest faith that if a company announces billions of dollars in investment curtailment, that that will realize a less volume of production. And the others have assessed – there’s assessments, I think at the G20, we’re talking two-plus million barrels that will not be produced in the U.S. because of this – two to three. And so I have every expectation that that will make its way.

Now, other countries may find our free market system – they might find that disconcerting, but that’s not new. The – our – we don’t control our energy production and our companies the way they do, and that’s not going to change. The – just in a similar way that a low price is – creates a behavioral change, forces a degree of rationalization in the market and the efficiencies, so do higher prices. High prices led to the creation of the deep broader offshore industry. Higher prices led to the creation of the shale industry.

So that’s the way in which we approach it, and we – I have every confidence that the United States will respond to the market in a rational way. We’re already seeing that and hopefully we’ll be able to do it without the – fewer and fewer of those kinds of announced bankruptcies and that, and companies can manage the way they do, but this will force a degree without question of efficiency in the producer, and the U.S. producers will be stronger and more resilient for it.

MS ORTAGUS: Thanks. Let’s take one more from Lara Jakes. Lara, you still on? Okay, let me just do a check. I think if we have – oh, we (inaudible).

OPERATOR: Just a second, she’s still on. Lara is still on. Just one second. There you go.

QUESTION: Hi.

MS ORTAGUS: Hi.

QUESTION: Okay. Thanks. So I know the State Department thought that one impact of the feud between Russia and Saudi Arabia had a kind of a silver lining for the pressure campaign against Nicolas Maduro in Venezuela, and that it increased more pressure on him as the prices were low. And so now that there’s a deal, I’m wondering what effect you think that’s going to have on the framework that was announced last month.

ASSISTANT SECRETARY FANNON: Yeah, thanks for the question. I – yeah, I think the low oil price has affected every producer around the world, and Venezuela’s not exempted from that market reality. With respect to Russia, United States initiated sanctions to prevent Russian entities from the illicit trading of oil that helped the former Maduro regime continue to perpetrate its abuses, which by the way has created the – a greater refugee crisis than in Syria. The scale of what is occurring there because of the illegal Maduro regime continues. And so we have increased our pressure campaign on the regime, which included the sanctioning of entities – Russian entities – that facilitated his hold to power through the trading of oil. That’s not stopping; we’re continuing that.

I think with respect to the announcement toward a democratic transition, the – that’s the consistent position we’ve had. We’ve – and we welcome that to happen as fast as possible. We continue to maintain our position with respect to anyone who trades illicit oil to fuel this human rights crisis behind Maduro, and we encourage all countries to come onside and not participate in that behavior. We’re hopeful that Russia will be a responsible actor in that regard as well, and we’re continuing on our pressure campaign. Thanks.

MS ORTAGUS: Great, thanks so much everybody for dialing into this call. We appreciate it and we will speak to you later. Thanks.

ASSISTANT SECRETARY FANNON: Bye-bye.

FED. April 16, 2020. Federal Reserve announces its Paycheck Protection Program Liquidity Facility is fully operational and available to provide liquidity to eligible financial institutions

The Federal Reserve on Thursday announced that its Paycheck Protection Program Liquidity Facility is fully operational and available to provide liquidity to eligible financial institutions, which will help support small businesses.

The Small Business Administration's Paycheck Protection Program, or PPP, guarantees loans extended by qualified lenders to small businesses so that those businesses can keep workers employed. The Federal Reserve's facility will support the effectiveness of the PPP by extending credit to financial institutions that make PPP loans, using such loans as collateral. Supplying financial institutions with additional liquidity will help increase their capacity to make PPP loans.

FULL DOCUMENT: https://www.frbdiscountwindow.org/generalpages/emergency%20credit%202020

UNEMPLOYMENT

DoL. BLS. REUTERS. 16 DE ABRIL DE 2020. Pedidos de auxílio-desemprego nos EUA superam 5,2 milhões na semana passada

Por Lucia Mutikani

WASHINGTON (Reuters) - Mais 5,2 milhões de norte-americanos solicitaram auxílio-desemprego na semana passada, elevando o total de pedidos pelo benefício no último mês para acima de 20 milhões, o que destacava a profunda crise econômica causada pelo surto do novo coronavírus.

O Departamento do Trabalho dos Estados Unidos informou nesta quinta-feira que 5,245 milhões de novas reivindicações de auxílio-desemprego foram registradas na semana passada, abaixo do número de 6,615 milhões (dado levemente revisado) na semana anterior.

De acordo com uma pesquisa da Reuters com economistas, esperava-se que os pedidos iniciais caíssem para 5,105 milhões na semana encerrada em 11 de abril. As estimativas da pesquisa chegaram a até 8 milhões.

________________

ORGANISMS

IMF. The Day 7 Briefing of our 2020 Virtual Spring Meetings newsletter.

HAPPENING NOW

We just started streaming the press briefing with International Monetary and Financial Committee Chair Lesetja Kganyago and IMF Managing Director Kristalina Georgieva. Watch it live.

LATER TODAY

Today at 1:30 PM EDT, we will livestream the press briefing on the economic outlook for the Western Hemisphere with Director Alejandro Werner.

GLOBAL AND REGIONAL REPORTS

It's hard to keep track of all our new economic reports, press conferences, blogs, podcasts and more—all published in the last few days—so we've put together a handy list below.

- Managing Director's Global Policy Agenda

- World Economic Outlook

- Global Financial Stability Report

- Fiscal Monitor Report

- Sub-Saharan Africa Economic Outlook

- Middle East and Central Asia Economic Outlook

- Asia and Pacific Outlook

- European Outlook

THE ECONOMIST AND THE EPIDEMIOLOGISTS

Yesterday, we broadcasted a virtual conversation between Managing Director Georgieva and Imperial College epidemiologists Neil Ferguson and Azra Ghani. They focused on how best to save lives and livelihoods. Watch the 25-min discussion.

IN CASE YOU MISSED IT

During the G20 Finance Ministers and Central Bank Governors meeting yesterday, Managing Director Georgieva discussed ramping up the IMF's crisis response for emerging markets and developing countries: "To assist our low income countries, we plan to triple our concessional lending. We are therefore urgently seeking US$18 billion in new loan resources for the Poverty Reduction and Growth Trust, and will also likely need at least US$1.8 billion in subsidy resources." Read the full statement.

Managing Director Georgieva was interviewed by CNBC's Sara Eisen to discuss the state of the global economy and how monetary policy can help combat the coronavirus pandemic. Watch the 7-minute segment.

Also, Chief Economist Gita Gopinath was interviewed by CNBCTV18 to discuss the global economic outlook with a focus on India. Watch the 20-min segment.

THE IMF AND COVID-19

We recently launched a hub for all of our COVID-19 content, including our latest analytical work on the economic impact of the pandemic, a global policy tracker that now covers 193 economies, a series of notes produced by IMF experts to help members address the economic effects of COVID-19, and recent news including press releases, speeches and more. If you are interested in the IMF's response to COVID-19, please read our latest Q&A.

The IMF also just approved immediate debt service relief to 25 member countries. "This provides grants to our poorest and most vulnerable members to cover their IMF debt obligations for an initial phase over the next six months and will help them channel more of their scarce financial resources towards vital emergency medical and other relief efforts," said Managing Director Kristalina Georgieva.

In addition, our new lending tracker showcases emergency assistance approved to member countries facing the economic impact of the pandemic. For upcoming discussions on emergency financing requests, see the meetings calendar of the Executive Board.

Lastly, to help member countries with strong fundamentals deal with pandemic, we just announced that our Executive Board has approved the creation of a new short-term liquidity line.

THE FINAL NEWSLETTER

Tomorrow we'll send the final daily update of this special Spring Meetings newsletter, rounding up highlights of the week and how you can stay in touch moving forward. How did we do? Did you find these newsletters useful? Please write to us directly with feedback.

Finally, we recently launched a new mobile app that houses our latest flagship reports in an easy-to-read format. Now you can search and discover our latest analysis on the go. Download now from the Apple App Store and the Google Play Store.

CORONAVIRUS

IMF. 04/16/2020. COVID-19 PANDEMIC AND THE ASIA-PACIFIC REGION: LOWEST GROWTH SINCE THE 1960s

By Chang Yong Rhee, Director of the IMF's Asia and Pacific Department

This is a crisis like no other. It is worse than the Global Financial Crisis, and Asia is not immune. While there is huge uncertainty about 2020 growth prospects, and even more so about the 2021 outlook, the impact of the coronavirus on the region will—across the board—be severe and unprecedented.

Growth in Asia is expected to stall to zero percent in 2020. This is the worst growth performance in almost 60 years, including during the Global Financial Crisis (4.7 percent) and the Asian Financial Crisis (1.3 percent). That said, Asia still looks to fare better than other regions in terms of activity.

Downward revisions are substantial, ranging from 3.5 percentage points in the case of Korea—which appears to have managed to slow the spread of the coronavirus while minimizing prolonged production shutdowns—to over 9 percentage points in the case of Australia, Thailand and New Zealand—all hit by the global tourism slowdown, and in the case of Australia by lower commodity prices. Within the region, Pacific Island countries are among the most vulnerable given the limited fiscal space, as well as comparatively underdeveloped health infrastructure.

Double slowdown

In addition to the impact from domestic containment measures and social distancing, two key factors are shaping the outlook for Asia:

- The Global slowdown: The global economy is expected to contract in 2020 by 3 percent—the worst recession since the Great Depression. This is a synchronized contraction, a sudden global shutdown. Asia’s key trading partners are expected to contract sharply, including the United States by 6.0 percent and Europe by 6.6 percent.

- China slowdown: China’s growth is projected to decline from 6.1 percent in 2019 to 1.2 percent 2020. This sharply contrasts with China’s growth performance during the Global Financial Crisis, which was little changed at 9.4 percent in 2009 thanks to the important fiscal stimulus of about 8 percent of GDP. We cannot expect that magnitude of stimulus this time, and China won’t help Asia’s growth as it did in 2009.

Prospects for 2021, while highly uncertain, are for strong growth. If containment measures work, and with substantial policy stimulus to reduce “scarring,” growth in Asia is expected to rebound strongly—more so than during the Global Financial Crisis. But there is no room for complacency. The region is experiencing different stages of the pandemic. China’s economy is beginning to get back to work, other economies are imposing tighter lockdowns, and some are experiencing a second wave of virus infections. Much depends on the spread of the virus and on how policies respond.

Policy priorities

This is a crisis like no other. It requires a comprehensive and coordinated policy response.

The first priority is to support and protect the health sector to contain the virus and introduce measures that slow contagion. If there is not enough space within countries’ budgets, they will need to re-prioritize other spending.

Containment measures are severely affecting economies. Targeted support to hardest-hit households and firms is needed. This is a real economic shock—unlike the Global Financial Crisis—and requires protecting people, jobs, and industries directly, not just through financial institutions.

The pandemic is also affecting financial markets and how they function. Monetary policy should be used wisely to provide ample liquidity, ease financial stress of industries and small and medium-sized enterprises, and, if necessary, relax macroprudential regulations temporarily.

External pressures need to be contained. Where needed, bilateral and multilateral swap lines and financial support from the multilateral institutions should be sought. In the absence of swap lines, foreign-exchange market interventions and capital controls may be the alternatives.

Targeted support, combined with domestic demand stimulus in a recovery, will help to reduce scarring, but it needs to reach people and smaller firms.

Asian economies have taken several initiatives in this direction with direct support for health sectors, direct fiscal stimulus packages—which in some advanced Asian economies are substantially bigger than the response during the Global Financial Crisis. And many economies have put in place measures aimed at helping small and medium-sized enterprises.

Central banks across the region have moved to provide ample liquidity, cut interest rates and some have used quantitative easing. For example, the Bank of Japan has expanded its repurchase operations, coordinated with other central banks around the world in efforts to ensure smooth functioning of the market, and introduced measures to facilitate corporate financing.

But additional actions may be needed for emerging-market Asian economies that have limited space for increased spending in their budgets. If the situation deteriorates, many emerging economies may to be forced to adopt a “whatever it takes” approach, despite their budget constraints and non-internationalized currencies. In many cases, they will face policy trade-offs.

For example, central bankers are considering buying government bonds in the primary market to support critical financial lifelines to smaller firms and households to avoid mass layoffs and defaults. An alternative to direct monetization could be to use the central bank’s balance sheet more flexibly and aggressively to support bank lending to small and medium-sized enterprises through risk-sharing with the government. In doing so, there can be a role for temporary outflow capital controls to help ensure stability in the face of large capital flows, balance sheet mismatches, and limited scope to use other policy tools.

IMF support

Since the outbreak of COVID-19, we are in continuous contact with the authorities in the region to offer advice and assistance. The Fund has several tools at its disposal to help its members surmount this crisis and limit its human and economic cost, and more than 15 countries from across the region have expressed interest in our two emergency financing instruments—the Rapid Credit Facility and the Rapid Financing Instrument.

FULL DOCUMENT: https://blogs.imf.org/2020/04/15/covid-19-pandemic-and-the-asia-pacific-region-lowest-growth-since-the-1960s/?utm_medium=email&utm_source=govdelivery

IMF. 04/16/2020. ECONOMIC POLICY IN LATIN AMERICA AND THE CARIBBEAN IN THE TIME OF COVID-19

By Alejandro Werner, Director of the IMF’s Western Hemisphere Department.

As of today, about 3,000 people have died from the COVID-19 virus in Latin America and the Caribbean. While the pandemic continues to spread across the region, countries are facing the worst economic recession since countries started producing national accounts statistics in the 1950s. The challenging external environment, coupled with much-needed measures to contain the pandemic, have led to a plummeting of economic activity across Latin America—where growth is poised to contract by 5.2 percent in 2020.

Given the dramatic contraction in 2020 and as countries implement polices to contain the pandemic and to support their economies—as emphasized in our previous blog—a sharp recovery in 2021 can be expected. Yet, even under this quick recovery scenario, the region faces the specter of another “lost decade” during 2015–25.

With atypical supply and demand shocks, a health crisis, and high financing costs across Latin America, the required actions to mitigate the human and economic costs of this crisis will be quite daunting and will require an unprecedented approach.

Governments respond to the crisis

Although with different speed, by now most countries in the region have taken significant public health measures to contain the spread of the virus, such as social distancing and restrictions on nonessential activities. They have also increased the amount of fiscal resources allocated to healthcare, including tests, beds, respirators, and other equipment, which is an overarching priority given that many countries are still underprepared to face the worst of the pandemic.

On the economic policy front, actions have varied. Countries have relied on direct transfers to vulnerable households (including an expansion of existing programs), relaxation of access requirements and expansion of unemployment insurance schemes, employment subsidies, temporary tax breaks and deferrals, and credit guarantees.

Sizeable packages have been announced by Brazil, Chile, and Peru, and others are expected to follow or enhance existing measures. Countries with better credit quality, as reflected in market spreads, have generally been more aggressive in their response to the pandemic.

Central banks in the region have reduced policy rates and taken measures to support liquidity and to counteract disorderly conditions in domestic financial markets. To ensure adequate liquidity conditions, some central banks have expanded the size of their liquidity provision operations, sometimes also allowing the participation of nonbank financial intermediaries and the use of highly-rated private sector securities. Several central banks (Brazil, Chile, Mexico, and Peru) have also intervened in foreign exchange and other financial markets to address disorderly conditions.

Moreover, bank regulators have taken a number of measures to facilitate the continued provision of credit in an uncertain and recessionary environment. They have made regulations less stringent, including by lowering reserve requirements, loan loss provisions and allowing the drawdown of countercyclical capital buffers on a temporary basis to facilitate the roll-over and/or restructuring of existing loans. Public banks in Brazil and Colombia have extended credit to small and medium-sized enterprises and firms in sectors particularly affected by the lockdowns, while Brazil, Chile, Peru and other countries have provided loan guarantees to help affected firms maintain and gain access to credit.

Implementation challenges

While we are in uncharted territory and policy responses are still evolving, policymakers are facing significant implementation challenges. For example, governments might be unable to reach vulnerable households through traditional transfers where there are no extensive social assistance systems already in place and where informality is prevalent. Moreover, smaller firms and those in the informal sector are harder to reach. Given the high level of informality in the region, countries should use all possible registries and methods to reach smaller firms and informal workers and firms.

Additionally, given that the pandemic, the recession, and the required policy responses will cause significant increases in public deficits and debt, countries will need to create fiscal space in the budget by reducing nonpriority expenditure and increasing the efficiency of spending.

Countries will need to ensure that policies taken in response to the crisis are not perceived as permanent and become entrenched and generate distortions—especially regarding targeted assistance to certain sectors. Several countries with fiscal rules on permissible deficits and/or on how much their governments can spend have rightly invoked escape clauses to allow for extraordinary increases in government spending and deficits (Brazil, Chile, Peru, among others), but policy makers should communicate a clear path back towards compliance with these rules over the medium term.

To provide much needed additional revenue to help finance all these initiatives, increased taxation of petroleum products at a time when world prices are lower could be appropriate insofar that they do not increase domestic prices to end users. Moreover, the tension between what is needed and what is possible is also subject to change by policy action. Those countries that can credibly commit to a sustainable fiscal policy by changing their tax, expenditure, and fiscal frameworks that guarantee corrections once the economy is back on track, will unlock significant fiscal space in the present to address the fall out.

Monetary policy actions

There is scope for further cuts in policy rates and liquidity support. Large output gaps and lower-for-longer rates in advanced economies suggest some central banks in the region could cut rates further, but large capital outflows may pose constraints on further policy easing.

Commercial banks may be wary to lend to risky sectors in a deep recession, so credit risk could be mitigated by direct lending or explicit guarantees provided by the government through development banks or special purpose vehicles set up to fulfill this objective.

Prudent and temporary use of regulatory flexibility, such as providing debtors some breathing space before classifying loans as past due and postponing associated costly provisions, has been applied in some countries to facilitate rollovers.

How the IMF can help

Several countries in the region will not be able to access sufficient resources on their own to cover the large external financing. So far, out of close to a 100 countries that have requested emergency financing from the IMF, 16 are from Latin America and the Caribbean. Additionally, other Latin American and Caribbean countries have requested new programs or the augmentation of existing ones, such as Honduras.

As this is an unprecedent crisis, the IMF is actively engaged and fully committed to help our member countries fill this gap through several tools. These include using its 1-trillion-dollar balance sheet, expediting the approval of lending facilities, increasing the limits of existing facilities, and providing debt relief to the poorest and most vulnerable member countries hit by the pandemic under the revised Catastrophe Containment and Relief Trust. Besides the emergency facilities, the Fund is ready to deploy its more traditional arrangements (such as Stand-by and Extended Fund Facilities) as well as its contingent credit lines (such as flexible credit lines and precautionary credit lines).

As our Managing Director, Kristalina Georgieva, has noted, saving lives and protecting livelihoods ought to go hand in hand. We cannot do one without the other. We at the IMF are working on making sure that there is a strong response to the health crisis as well as protecting the strength of economies.

FULL DOCUMENT: https://blogs.imf.org/2020/04/16/economic-policy-in-latin-america-and-the-caribbean-in-the-time-of-covid-19/?utm_medium=email&utm_source=govdelivery

________________

ECONOMIA BRASILEIRA / BRAZIL ECONOMICS

CORONAVÍRUS

FGV. IBRE. FGV - Impactos do COVID-19. Os direitos de imigrantes e refugiados em tempos de pandemia

Como fica a situação dos imigrantes e refugiados em tempos de pandemia, com fronteiras fechadas em diversos países? Afinal, eles têm direito à plena igualdade pela constituição a direitos iguais. Tem sido necessária uma proteção humanitária para todos que necessitam de ajuda, como imigrantes, migrantes e refugiados, e a migração internacional está trabalhando para que eles consigam dignidade básica, garantindo alimentação e itens de higiene. Saiba mais sobre o assunto com o professor Thiago Amparo, da FGV Direito SP e da FGV RI – Escola de Relações Internacionais.

VÍDEO: https://www.youtube.com/watch?v=4e2Ge0S6cDw&feature=youtu.be

ECONOMIA

FGV. IBRE. 16/04/20. Indicador de Incerteza da Economia. Prévia do IIE-Br de abril: Incerteza da Economia deve subir e atingir maior nível da série histórica

Apuração prévia extraordinária com dados coletados até o dia 14 deste mês sinaliza que o Indicador de Incerteza da Economia (IIE-Br) da Fundação Getulio Vargas subiria 44,5 pontos em abril, para 211,6 pontos, maior nível da série histórica. O resultado se seguiria a uma alta de 52,0 pontos em fevereiro. O nível atingido pelo indicador nesta prévia é 75 pontos superior ao registro máximo do IIE-BR antes da atual crise, de 136,8 pontos em setembro de 2015.

Os dois componentes do IIE-Br sinalizam, nesta prévia, forte alta em abril. O componente de Mídia, subiria 35,5 pontos, para o nível recorde de 196,5 pontos. O componente de Expectativa, subiria 62,6 pontos, para 226,1 pontos, o segundo maior nível da série, ficando abaixo apenas do nível de outubro de 2002, quando o indicador chegou a 257,5 pontos.

DOCUMENTO: https://portalibre.fgv.br/navegacao-superior/noticias/previa-do-iie-br-de-abril-incerteza-da-economia-deve-subir-e-atingir-maior-nivel-da-serie-historica.htm

INFLAÇÃO

FGV. IBRE. 16/04/20. Índices Gerais de Preços. IPC-S. Comportamento dos itens "Gasolina" e "Roupas" influenciam recuo da inflação pelo IPC-S

O IPC-S de 15 de abril de 2020 variou 0,34%, ficando 0,04 ponto percentual (p.p) abaixo da taxa registrada na última divulgação.

Nesta apuração, dois das oito classes de despesa componentes do índice registraram decréscimo em suas taxas de variação. A maior contribuição partiu do grupo Transportes (-0,44% para -0,97%). Nesta classe de despesa, cabe mencionar o comportamento do item gasolina, cuja taxa passou de -2,07% para -3,68%.

Também registrou decréscimo em sua taxa de variação o grupo: Vestuário (-0,16% para -0,23%). Nesta classe de despesa, vale destacar o comportamento do item: roupas (-0,13% para -0,30%).

Em contrapartida, os grupos Despesas Diversas (0,09% para 0,34%), Educação, Leitura e Recreação (0,22% para 0,41%), Alimentação (1,60% para 1,65%), Habitação (0,33% para 0,38%), Saúde e Cuidados Pessoais (0,47% para 0,50%) e Comunicação (0,05% para 0,06%) apresentaram avanço em suas taxas de variação. Nestas classes de despesa, vale citar os itens: serviços bancários (0,01% para 0,33%), passagem aérea (3,30% para 7,40%), laticínios (2,18% para 3,01%), condomínio residencial (0,37% para 0,62%), medicamentos em geral (0,06% para 0,22%) e mensalidade para internet (0,07% para 0,27%).

DOCUMENTO: https://portalibre.fgv.br/navegacao-superior/noticias/comportamento-dos-itens-gasolina-e-roupas-influenciam-recuo-da-inflacao-pelo-ipc-s.htm

COMÉRCIO EXTERIOR BRASILEIRO

BACEN. 16 Abril 2020. Circulares aprovadas na Reunião de Diretoria de 15/04/2020. BC amplia prazos de contratos de câmbio relativos ao comércio exterior

O Banco Central ampliou para 1.500 dias o prazo máximo entre a contratação e a liquidação do contrato de câmbio de exportação. No caso de liquidação do contrato de câmbio realizada após o embarque da mercadoria ou após a prestação do serviço, também deve ser observado o prazo máximo de 1.500 dias entre os dois eventos.

O prazo máximo anterior era de 750 dias e, durante o seu decorrer, o exportador ainda tinha que observar o prazo intermediário de 360 dias para embarcar a mercadoria ou prestar o serviço. Com a mudança, o exportador passa a ter prazo único de até 1.500 dias entre a data da contratação e liquidação da operação, permitindo também que o embarque possa ocorrer dentro desse período.

A medida permite que o exportador tenha mais tempo para produzir e providenciar o embarque da mercadoria ou para prestar o serviço, além de trazer maior flexibilidade para renegociar e estender a data em que receberá o pagamento do importador estrangeiro.

Tendo em vista os potenciais efeitos da crise provocada pelo Covid-19 sobre o comércio exterior brasileiro, a nova regra vale para os contratos de câmbio celebrados a partir de 20 de março de 2020, bem como para os contratos de câmbio celebrados em data anterior que estivessem com a situação regular em 20 de março de 2020, data da publicação e da entrada em vigor do Decreto Legislativo n° 6, que reconhece a ocorrência do estado de calamidade pública. O uso da nova regra depende também da concordância das partes no contrato de câmbio.

Houve também aumento de prazo para o pagamento antecipado de importação. O prazo anterior era de 180 dias e, com a nova medida, passou a ser de 360 dias. A medida permite ao importador renegociar as condições pactuadas com o exportador estrangeiro. Essa alteração do prazo se aplica também aos pagamentos antecipados de importação que já foram efetuados.

Circular 4.002: https://www.bcb.gov.br/estabilidadefinanceira/exibenormativo?tipo=Circular&numero=4002

INDÚSTRIA

IPEA. 15/04/2020. Ipea aponta queda de 1% no consumo de bens industriais em fevereiro. As importações cresceram 0,2% no período

O Indicador Ipea de Consumo Aparente de Bens Industriais, que mede a produção industrial interna não exportada, acrescida das importações, teve recuo de 1% no mês de fevereiro desde ano, em relação a janeiro, na série com ajuste sazonal. O dado foi divulgado nesta quarta-feira (15) pelo Instituto de Pesquisa Econômica Aplicada (Ipea). Na comparação com fevereiro de 2019, o Indicador cresceu 1,2%.

Com a queda de 1%, resultado que sucedeu alta de 11,1% no mês anterior, o trimestre móvel encerrado em fevereiro, apresentou recuo de 3,4%. Entre os componentes do consumo aparente, foi registrada retração de 1,4% na demanda interna por bens industriais nacionais e avanço de 0,2% nas importações. Já no acumulado em doze meses encerrados em fevereiro, houve ligeira queda no consumo aparente (-0,1%), enquanto a produção industrial, medida pelo IBGE, acumulou baixa de 1,2%.

Em fevereiro deste ano, o desempenho foi heterogêneo entre os segmentos das grandes categorias econômicas, na comparação com janeiro: alta no consumo aparente de bens de capital (+ 6,2%) e de bens de consumo duráveis (+ 1,1%) e queda nos bens intermediários (- 1%).

Nas classes de produção, a demanda interna por bens da indústria de transformação teve alta modesta de 0,4% de janeiro para fevereiro. Enquanto isso, a indústria extrativa mineral voltou a apresentar comportamento volátil, com recuo de 12,1% no mesmo período (apesar do avanço de 28,3% em janeiro). Dez dos 22 segmentos da indústria de transformação avançaram em fevereiro, com destaque positivo para o segmento de máquinas e equipamentos, que cresceu 9,8%.

Indicador: http://www.ipea.gov.br/cartadeconjuntura/index.php/2020/04/15/indicador-ipea-de-consumo-aparente-de-bens-industriais-fevereiro-de-2020/

CNI. 15/04/2020. Confiança dos empresários é a menor da história com pandemia de Covid-19. O Índice de Confiança do Empresário Industrial registrou queda recorde entre março e abril, de 25,8 pontos. Entre janeiro e abril o recuo foi de 30,8 pontos

Levantamento da Confederação Nacional da Indústria (CNI) revela que, em meio à pandemia da Covid-19, a confiança da indústria brasileira é a mais baixa da história. O Índice de Confiança do Empresário Industrial (ICEI) registou queda recorde de 25,8 pontos e ficou em 34,5 pontos, numa escala de 0 a 100.

É o menor patamar e a maior baixa da série histórica iniciada em 2010. O índice também já havia recuado em fevereiro e março; o recuo acumulado foi de 30,8 pontos.

“A queda na confiança dos empresários pode contribuir para a paralização dos investimentos, ou seja, para o agravamento da crise econômica”, avalia o diretor de Desenvolvimento Industrial da CNI, Carlos Abijaodi. “Há dificuldades no fluxo de insumos, mercadorias e trabalhadores e as medidas de isolamento social e o consequente 'desaparecimento do consumidor' resultou em forte queda na receita das empresas”, explica o relatório técnico do ICEI, que também pontua a redução e o encarecimento do crédito, enquanto as despesas fixas continuam.

Antes da queda de 25,8 pontos, registrada entre março e abril, o maior recuo num único mês havia sido de 5,8 pontos, em junho de 2018, como consequência da greve dos caminhoneiros. A atual redução traduz o cenário atual de queda forte contração na atividade e elevada incerteza em razão da pandemia da Covid-19.

O ICEI é o resultado de dois componentes: as condições atuais e as expectativas. A queda registrada no último mês está mais relacionada com as expectativas que são negativas e geram incertezas do que com as condições atuais, que são de redução da atividade até o momento. O índice de Condições Atuais caiu 20,2 pontos, para 34,1 pontos, enquanto o índice de Expectativas, caiu 28,6 pontos, para 34,7 pontos.

ICEI por região

A queda da confiança é generalizada entre as regiões geográficas do Brasil, mas é mais sentida entre os empresários da Região Sul, cujo índice acumulou uma queda de 34,6 pontos entre janeiro e abril. No Norte foi registrada a menor queda na mesma base de comparação, mas ainda significativa, de 26,8 pontos.

ICEI por atividade

A falta de confiança alcança todos os setores de atividade industrial. O indicador de confiança é menor entre os empresários da Indústria de Transformação (34,3 pontos) e de Construção (34,8 pontos) e um pouco maior entre os da Indústria Extrativa (39,1 pontos).

Entre os setores da Indústria de Transformação, aqueles com maiores indicadores de confiança são Perfumaria, sabões, detergentes, produtos de limpeza e de higiene pessoal; Farmoquímicos e farmacêuticos; e Alimentos, com índices de, respectivamente, 42,9 pontos; 42,4 pontos; e 40,5 pontos.

No outro extremo, temos produtores de bens de consumo duráveis como Móveis (26,0 pontos), Vestuário e acessórios (29,1 pontos), Calçados e suas partes (29,4 pontos) e Produtos têxteis (30,0 pontos).

DOCUMENTO: https://noticias.portaldaindustria.com.br/noticias/economia/confianca-dos-empresarios-e-a-menor-da-historia-com-pandemia-de-covid-19/

INOVAÇÃO

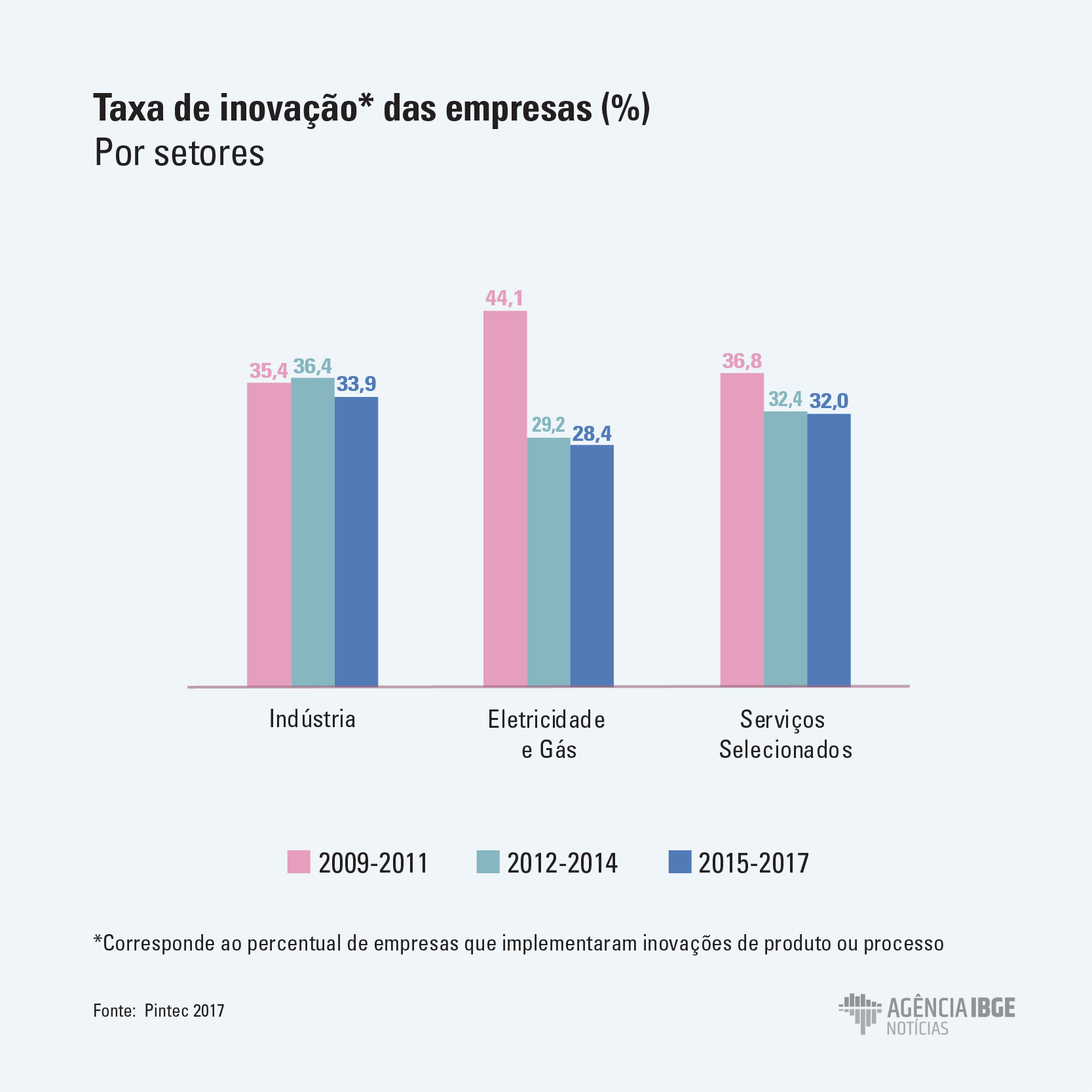

IBGE. 16/04/2020. Pintec 2017: caem a taxa de inovação, os investimentos em atividades inovativas e os incentivos do governo

Entre 2015 e 2017, 33,6% das 116.962 empresas brasileiras com dez ou mais trabalhadores fizeram algum tipo de inovação em produtos ou processos, taxa 2,4 pontos percentuais abaixo da apresentada no triênio anterior (de 2012-2014), quando atingiu 36,0%. É o que revela a Pesquisa de Inovação (Pintec) 2017 do IBGE. A indústria foi a mais afetada, com o percentual de empresas inovadoras caindo de 36,4% em 2014 para 33,9% em 2017, o menor patamar das três últimas edições.

O investimento nas atividades inovativas chegou a R$ 67,3 bilhões em 2017, representando 1,95% da receita líquida das empresas, com uma queda de 17,42% em relação aos R$ 81,5 bilhões investidos em 2014, equivalentes a 2,5% da receita líquida. Do total de gastos, R$ 25,6 bilhões foram para atividades internas de P&D, atingindo 0,74% da receita de vendas. Outros R$ 21,2 bilhões foram aplicados na aquisição de máquinas e equipamentos, 0,62% da receita de vendas, e R$ 7,0 bilhões na aquisição externa de P&D, 0,20% da receita de vendas.

A pesquisa destaca também que o percentual de empresas beneficiadas com algum incentivo do governo recuou de 39,9%, em 2014, para 26,2%, em 2017. O financiamento à compra de máquinas e equipamentos, principal mecanismo de incentivo à inovação, foi a modalidade que mais perdeu relevância, caindo de 29,9% empresas beneficiadas para 12,9% no mesmo período.

Já a participação de mulheres ocupadas em atividades de P&D nas empresas inovadoras subiu de 20,9% em 2014 para 23,6% em 2017.

Quase 40 mil empresas inovaram entre 2015 e 2017

No triênio 2015-2017, das 116.962 empresas com dez ou mais pessoas ocupadas, 39.329 implementaram produtos ou processos novos ou significativamente aprimorados. A taxa geral de inovação foi de 33,6%, 2,4 p.p. abaixo do verificado no triênio 2012-2014 (36,0%).

A indústria foi a mais afetada ao registrar 33,9% de empresas inovadoras, o menor patamar das três últimas edições. Os setores de eletricidade e gás e de serviços selecionados mantiveram a tendência de queda apresentada a partir do triênio 2012-2014, caindo de 29,2% para 28,4% e de 32,4% para 32%, respectivamente.

Empresas investem R$ 67,3 bilhões em atividades inovativas

Em 2017, o dispêndio das empresas nas atividades inovativas foi de R$ 67,3 bilhões, 1,95% da receita líquida – queda de 17,42% em relação aos R$ 81,5 bilhões investidos entre 2012 e 2014, equivalente a 2,5% da receita líquida.

A indústria teve a terceira queda consecutiva no dispêndio com atividades inovativas, caindo de 2,12% das receitas líquidas em 2014 para 1,65% em 2017. As atividades internas de P&D receberam 0,62% das receitas líquidas. A maior queda foi nos gastos na aquisição de máquinas e equipamentos, 0,51%, ante 1,11% em 2011 e 0,85% em 2014.

Nas empresas de eletricidade e gás, 0,66% das receitas líquidas foram para atividades inovativas, ligeiro aumento em relação à 2014 (0,57%) e queda em relação à 2011 (1,28%). A participação dos gastos em aquisição externa de P&D sobre a receita recuou para 0,16%, ante 0,83% em 2011 e 0,26% em 2014. Em 2017, a aquisição de máquinas e equipamentos subiu para 0,32% da receita líquida, após queda, entre 2011 e 2014, de 0,16% para 0,09%.

Nos serviços selecionados após crescimento em 2014 (7,81%) comparativamente a 2011 (4,96%), houve queda em 2017 para 5,79%. No tocante à aquisição de máquinas e equipamentos, após significativo crescimento entre 2011 e 2014 (de 1,38% para 3,50%), a intensidade dos gastos sobre a receita caiu para 1,80% em 2017. Mas, nas atividades internas de P&D, o setor manteve a sequência no crescimento registrado entre 2011 e 2014 (1,82% para 2,13%), ao subir para 2,40% em 2017.

Investimentos nas atividades internas de P&D assumem a liderança, ao atingir 0,74% da receita líquida das empresas

Em 2017, destaca-se a perda de posição relativa da categoria máquinas e equipamentos (de 42,4% em 2011 e 41,1% em 2014 para 31,5% em 2017) em favorecimento dos gastos em P&D interno, que assume a liderança na composição, passando de 30,8% em 2011 e 30,3 em 2014 para 38,1% em 2017. A intensidade dos gastos das empresas inovadoras nas atividades internas de P&D foi de 0,74% das receitas líquidas.

Na indústria, houve perda de participação dos gastos em máquinas e equipamentos (de 40,2% para 31,1% entre 2014 e 2017), acompanhada pelo aumento da participação dos gastos nas atividades internas de P&D (de 31,5% para 37,4%).

Nos serviços selecionados, a participação das máquinas e equipamentos entre 2014 e 2017 caiu de 44,8% para 31,0%, e os dispêndios nas atividades de P&D interno subiram de 27,2% em 2014 para 41,6% em 2017.

Já nas empresas de eletricidade e gás, o movimento foi oposto, com perda da participação dos dispêndios em aquisição externa de P&D de 46,0% em 2014 para 24,5% em 2017. E aumento na aquisição de máquinas e equipamentos, de 15,5% em 2014 para 48,6% em 2017. Os dispêndios nas atividades internas de P&D caíram de 30,0% em 2014 para 21,1% em 2017.

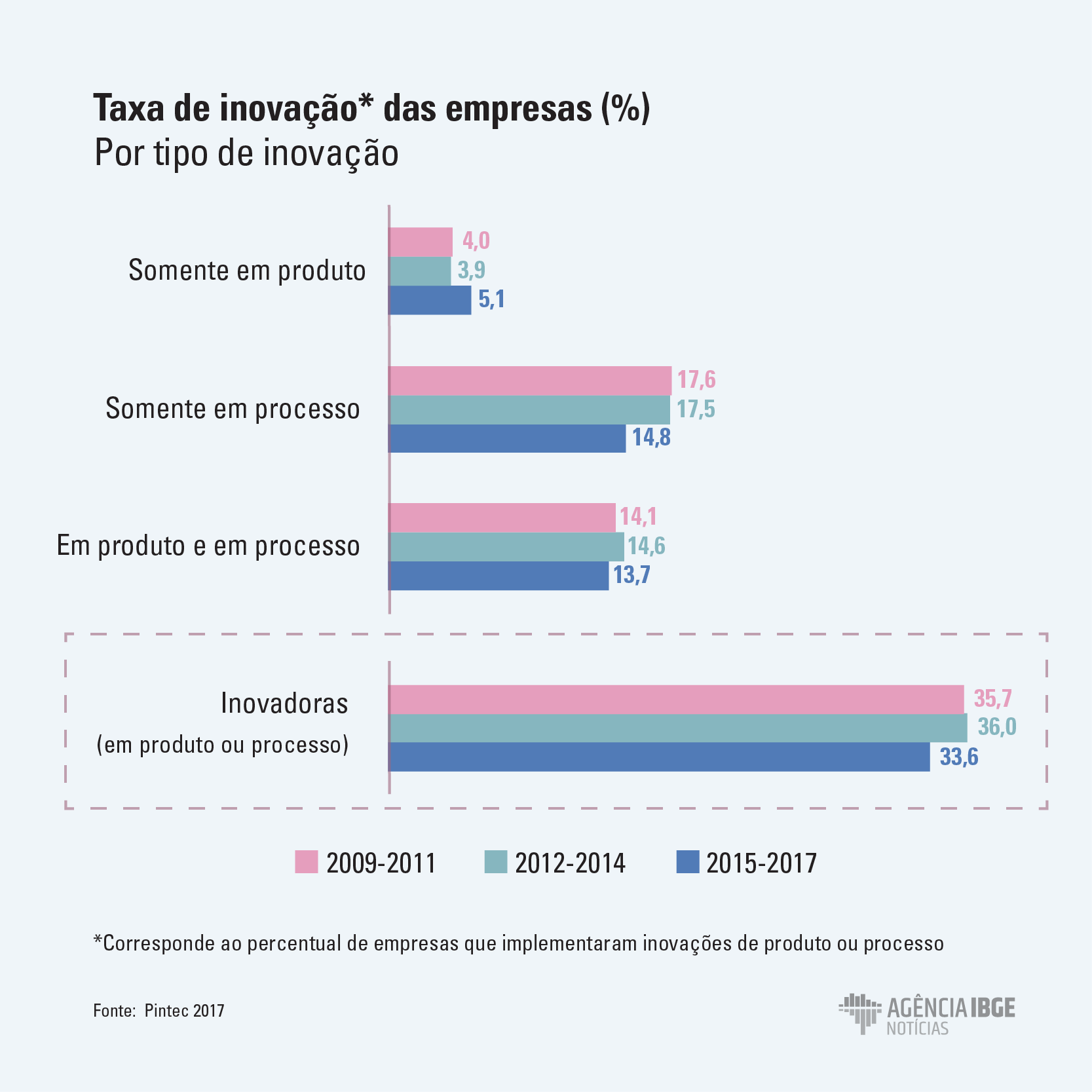

Cresce a proporção de empresas que inovam só em produto

A queda expressiva nos dispêndios em máquinas e equipamentos pode guardar relação com a queda nas taxas de inovação em processo. A aquisição de máquinas e equipamentos, seja para modernização tecnológica ou para produção de novos produtos, configura-se na modalidade mais comum de inovação de processo no Brasil.

Na Pintec 2017, a participação das empresas que inovaram apenas em processo diminuiu de 17,5% em 2014 para 14,8%. O percentual de empresas que inovaram conjuntamente em produto e processo também reduziu, mas em menor intensidade (-0,9 p.p.), de 14,6% para 13,7%. Por outro lado, cresceu a proporção de empresas que inovaram apenas em produto: de 3,9% em 2014 para 5,1% em 2017.

Caem gastos do governo, mas cresce percentual de empresas que recorrem à Lei do Bem

Apesar do aumento das empresas que se beneficiaram da Lei do Bem (de 3,5% em 2014 para 4,7% em 2017), a diminuição do apoio total do governo tem sua tendência influenciada pela diminuição do apoio para aquisição de máquinas e equipamentos.

No triênio 2015-2017, 26,2% de empresas inovadoras foram beneficiadas com algum tipo de apoio à inovação, queda em relação aos triênios 2009-2011 e 2012-2014, quando as proporções foram de 34,2% e 39,9%, respectivamente.

O financiamento para a compra de máquinas e equipamentos ainda é o principal mecanismo de incentivo à inovação, mas foi a modalidade que mais perdeu relevância nas empresas beneficiadas, recuando de 29,9% para 12,9% no período.

Na indústria, o percentual de empresas inovadoras que utilizaram financiamento para aquisição de máquinas e equipamentos caiu de 31,4%, entre 2012 e 2014 para 14,1% entre 2015 e 2017. Apesar disso, essa modalidade continua sendo a principal do setor. Por outro lado, o percentual de empresas inovadoras que se beneficiaram da Lei do Bem aumentou de 3,2% para 4,3%.

Nos serviços selecionados, o incentivo à aquisição de máquinas e equipamentos caiu para 3,8%, ante 16,1% no triênio anterior. No caso da Lei do Bem, houve um aumento de 6,1% para 6,7%, tornando essa modalidade a principal fonte de apoio à inovação nessas atividades no triênio 2015-2017.

Nas empresas de eletricidade e gás, 3,2% tiveram apoio para aquisição de máquinas e equipamentos, ante 11,1% em 2014. O aceso à Lei do Bem subiu de 28,8% em 2014 para 34,9% em 2017.

Serviços selecionados e indústria concentram os impactos positivos da inovação

Os impactos relacionados à melhoria da qualidade e à manutenção da participação de mercado ainda foram os mais destacados pela indústria e por empresas de serviços selecionados. Os investimentos em atividades inovativas melhoraram a qualidade dos bens e serviços para 92,8% das empresas de serviços selecionados, 82,6% das indústrias e 48,8% das empresas de eletricidade e gás.

Também permitiram manter a participação de mercado para 80,7% das empresas de serviços selecionados e 83,1% das indústrias. E assegurou a ampliação de participação de mercado para 73,7% das indústrias e 71,0% das empresas de serviços selecionados.

Outro impacto destacado é o aumento da produção e da prestação de serviços, apontado por 75,5% das indústrias, 75,2% das empresas de serviços e 54,8% das empresas de eletricidade e gás. Também aumentou a flexibilidade de produção para 74,1% das indústrias, 68,9% das empresas de serviços selecionados e 50,6% das empresas de eletricidade e gás.

Serviços selecionados tem maior proporção de profissionais com dedicação exclusiva em P&D

Em 2017, entre os profissionais ocupados nas atividades de pesquisa e desenvolvimento, 61,3% estão em regime de dedicação exclusiva; e 38,7% parcial; ante 61,4% e 38,6% em 2014, respectivamente. O setor de serviços selecionados concentra o maior percentual de dedicação exclusiva: 72,1% ante 57% na indústria e 14,4% em eletricidade e gás.

Mais de 70% das pessoas ocupadas nas atividades de P&D têm pelo menos graduação. Nas empresas de eletricidade e gás, há maior percentual de graduados (69,3%), e pós-graduados, (17%).

Cresce a proporção de mulheres nas atividades de P&D

Apesar de menos de um quarto das pessoas ocupadas em cargos de pesquisadores nas empresas brasileiras ser do sexo feminino, houve um aumento nessa proporção em relação ao triênio anterior. Entre 2012-2014, as mulheres eram 20,9% do pessoal ocupado, percentual que subiu para 23,6% em 2015-2017.

Entre os setores onde as mulheres pesquisadoras eram maioria, destacam-se: confecção de artigos do vestiário e acessórios (75,5%); fabricação de sabões, detergentes, produtos de limpeza, cosméticos, produtos de perfumaria e higiene pessoal (62,3%); produtos farmoquímicos (53,7%); e farmacêuticos (60%).

Avançam iniciativas de cooperação para inovar

A Pintec 2017 mostrou que 15,6% das empresas inovadoras realizaram algum tipo de atividade inovativa com outras organizações. No setor de eletricidade e gás, o percentual subiu de 55% no triênio 2012-2014 para 70,1% em 2017. Na indústria, variou de 14,3% para 14,9%. Nos dois setores, os fornecedores foram os principais parceiros. Em serviços selecionados, o percentual caiu de 23,6% em 2014 para 18,4% em 2017. Nesse setor, a interação com clientes e consumidores foi a principal forma de parceria.

Na indústria e nos serviços selecionados, a internet e os clientes continuam a ser as principais fontes de informação para às atividades inovativas. No setor de eletricidade e gás, as fontes provêm dos fornecedores e outras empresas do grupo.

Chama a atenção o aumento relativo da importância do departamento de P&D para os três setores: em 2017, ele foi considerado importante fonte para 45,6% das empresas de eletricidade e gás e para 16,4% das indústrias – ante 26,6%, e 11,8%, respectivamente, em 2014. Já nos serviços selecionados, a proporção recuou de 30,5% para 24,2%, no período.

Para 82% das empresas inovadoras, riscos econômicos são principal obstáculo à inovação

No período 2015-2017, os riscos econômicos excessivos ganharam importância, configurando-se como principal obstáculo à inovação para 81,8% das empresas inovadoras, após ocupar a terceira e segunda posições nos triênios 2009-2011 e 2012-2014.

Em contrapartida, os elevados custos para inovar caíram da primeira colocação, em 2011 e em 2014, para a segunda, sendo indicado por 79,7% das empresas inovadoras.

A falta de pessoal qualificado foi indicada por 65,5% das empresas inovadoras, despontando como terceiro obstáculo no ranking, ganhando espaço em relação à escassez de fontes apropriadas de financiamento (63,9%), que caiu para a quarta posição.

Em relação às empresas que não inovaram, as condições de mercado permanecem como principais entraves para a não realização da inovação: 60,4% ante 54,9% no triênio anterior. Em seguida, destacam-se as inovações prévias, com perda de importância entre os triênios (de 20,3% para 16,7%). Por fim, outros fatores são apontados por 22,9% das empresas, com ligeira queda em relação a 2012-2014 (24,8%).

Na edição 2017 da Pintec, observou-se aumento no percentual de empresas inovadoras que realizaram atividades de biotecnologia (4,6% ante 3,4% do período anterior) e nanotecnologia (2,3% contra 1,8%). Em ambos os casos, são nas grandes empresas em que mais se desenvolvem essas atividades.

Com menos investimento, cai para 33,6% quantidade de empresas inovadoras. Pesquisa mostra que uma em cada três empresas inovaram em produtos ou processos entre 2015 e 2017

A recessão econômica e a queda nos investimentos em bens de capital tiveram impacto direto nas atividades de inovação. Segundo a Pesquisa de Inovação (Pintec 2017), divulgada hoje (16) pelo IBGE, o percentual de empresas que inovaram caiu de 36% no triênio encerrado em 2014 para 33,6% (uma em cada três) entre 2015 e 2017, em um universo de 116.962 companhias com dez ou mais trabalhadores.