CANADA ECONOMICS

INTERNATIONAL TRANSACTIONS

StatCan. 2017-06-16. Canada's international transactions in securities, April 2017

Foreign investment in Canadian securities

$10.6 billion, April 2017

Canadian investment in foreign securities

-$9.9 billion, April 2017

Source(s): CANSIM table 376-0131.

Foreign investment in Canadian securities totalled $10.6 billion in April, mainly acquisitions of government debt instruments. At the same time, Canadian investors reduced their holdings of foreign securities by $9.9 billion, the largest divestment since January 2016.

As a result, Canada's international transactions in securities generated a net inflow of funds into the Canadian economy of $20.5 billion in April.

Foreign investment in Canadian securities has exceeded Canadian investment in foreign securities by $49.1 billion since the beginning of 2017, following a record annual net inflow of $151.9 billion in 2016. Significant foreign purchases of Canadian private corporate instruments led the inflow of funds during this period.

Foreign investment in Canadian bonds strengthens

Foreign investment in Canadian securities slowed to $10.6 billion in April, from $15.1 billion in March. Overall, foreign investors acquired Canadian bonds but reduced their exposure to equities and money market instruments in April.

Chart 1 Chart 1: Foreign investment in Canadian securities

Foreign investment in Canadian securities

Foreign acquisitions of Canadian bonds amounted to $13.0 billion in April, the largest such investment since July 2016. Foreign investors acquired $6.7 billion of federal government bonds, after reducing their exposure to these instruments for three straight months. They also added $4.3 billion of Canadian private corporate bonds to their holdings, largely new issues denominated in foreign currencies. Canadian long-term interest rates were down by 11 basis points in April, a third consecutive monthly decline.

Non-resident investors reduced their holdings of Canadian money market instruments by $1.1 billion in April, following investments totalling $2.9 billion in March. The reduction was mainly in private corporate paper. Foreign acquisitions of federal government paper moderated the overall divestment in April. Canadian short-term interest rates edged down and the Canadian dollar was down by 1.9 US cents against its US counterpart in the month.

Foreign holdings of Canadian shares were down $1.3 billion in April, following strong investments in the first quarter. This divestment resulted mainly from sales on the secondary market. Canadian stock prices edged up over the month.

Canadian investors reduce their holdings of foreign securities

Canadian investors sold $9.9 billion of foreign securities in April, after four straight months of acquisitions. The divestment was in both foreign debt securities and equities.

Chart 2 Chart 2: Canadian investment in foreign securities

Canadian investment in foreign securities

Canadians reduced their holdings of foreign shares by $5.7 billion in April, following record acquisitions of $26.2 billion in the first quarter. The reduction in April targeted both US and non-US foreign shares, while acquisitions in the first quarter focused on US instruments. US stock prices were up 0.9% in the month and 6.6% since December 2016.

Canadian holdings of foreign debt securities were down $4.1 billion in April, a second consecutive monthly divestment. Significant sales of US Treasury bonds were moderated by acquisitions of US corporate bonds in the month. US long-term interest rates were down by 18 basis points while short-term rates were up by six basis points in the month.

FULL DOCUMENT: http://www.statcan.gc.ca/daily-quotidien/170616/dq170616a-eng.pdf

HOUSING BUBBLE

The Globe and Mail. Jun. 15, 2017. Hidden tax savings for homeowner heirs

TIM CESTNICK

My friend, William, is the executor of his father’s estate. His father, Jack, passed away two months ago. Jack was a hoarder. He loved the thrill of getting a deal on things. He once bought a year’s supply of oatmeal because it was on sale. He also bought big-ticket items when he found a great price (a life-size wax replica of Willie Nelson, for example) – even if he didn’t need or want the stuff. When Jack passed away, he had a home and seven storage units full of junk.

Today, William has the job of selling the home. Once the home is cleaned up, it’ll be worth a lot of money because it’s in a desirable neighbourhood in Toronto. I shared with William that there could be some tax savings when selling his father’s place. And, like William, if you sell the home of a deceased loved one, you, too, could create some tax savings that will end up in the pockets of the heirs.

The idea

Jack’s home is worth significantly more than its original cost. He paid $200,000 for the place many years ago and, at the time of his death, it was worth $1.2-million. At the time of Jack’s death, the $1-million capital gain on his home was realized since, under our tax law, you’ll be deemed to have sold all your capital property immediately before your death.

There are a few ways to defer or eliminate the tax on your assets when you pass away. Leaving your assets to your spouse is the first line of defence. Jack didn’t have that option since his wife predeceased him. In the case of a principal residence, you can shelter the tax on any gains using your principal-residence exemption (PRE). This will ensure that, in Jack’s case, there won’t be any tax on the $1-million gain upon his death. When William files his father’s final tax return, he’ll have to report the deemed disposition of the principal residence on Schedule 3, which is a new requirement as of 2016, notwithstanding that there won’t be any tax to pay on the residence.

Aside from the PRE, there may be another opportunity to save tax on Jack’s final tax return. This idea is possible because William plans to sell his father’s residence very soon. It’s quite possible that a capital loss will be realized by the estate when the property is sold, which can save taxes.

Here’s how: If you pass away, your estate will become the owner of your home after your death (assuming the home does not pass to a joint owner with right of survivorship). In Jack’s case, the adjusted cost base of the home to his estate is $1.2-million – the fair market value at the time of his death.

Let’s assume that William, as executor, will then sell the home for its current value of $1.2-million, less the costs of selling the home. So, the net proceeds to the estate will be less than $1.2-million. The result is that Jack’s estate will realize a capital loss. There’s a pretty good chance of that happening after your death, too. Don’t forget, even if your executor sells your home for its fair market value at the date of your death, the selling costs alone (say, 6 per cent, or $72,000 in Jack’s case) would create a capital loss.

The savings

Now, for the tax savings. If a capital loss is realized by the estate in the first taxation year of the estate, the loss can be carried back to the final tax return of the deceased, to offset any capital gains – or other income (yes, capital losses can be applied against any type of income in the year of death), that might have been taxable on that return. Subsection 164(6) of our tax law allows this loss to be carried back. That’s right, Jack’s heirs will be able to recover some tax that might have been paid on his final tax return if there’s a loss in his estate when selling the home.

One last point: A principal residence is normally considered to be “personal-use property,” and the taxman won’t allow you, or your estate, to claim a capital loss on personal-use property. Not to worry. The residence will not be considered personal-use property provided none of the beneficiaries of the estate (or someone related to a beneficiary) lives in the home after the owner’s death.

Tim Cestnick, FCPA, FCA, CPA(IL), CFP, TEP, is an author and founder of WaterStreet Family Offices.

The Globe and Mail. 16 Jun 2017. Home Capital: Settlement a step forward for beleaguered firm. The remaining key hurdle (and the most significant) is getting sufficient funding. Geoffrey Kwan Analyst with Royal Bank of Canada Dominion Securities

Home Capital Group Inc. relieved a major headache by agreeing to settle a dispute with securities regulators, but the mortgage lender’s funding woes are still a central concern as investors crave more tangible signs of a turnaround.

Toronto-based Home Capital watched its share price surge 12.7 per cent on Thursday after news that the troubled mortgage lender has struck a pair of deals to settle allegations of misleading disclosures about fraudulent mortgage underwriting practices dating back to 2014.

If the settlements are approved by regulators and the courts, Home Capital and three former senior executives will pay $12million in penalties to the Ontario Securities Commission. Most of those funds will go toward a $29.5-million payment to resolve a class-action lawsuit filed earlier this year against the lender.

In mid-April, Home Capital insisted the OSC’s allegations were “without merit” and planned to “vigorously” defend itself. But days later, its stock price plunged about 65 per cent and the company soon suffered a near-death experience as its depositors fled for the exits, with the OSC’s detailed allegations appearing to be one factor that helped trigger the run. In short order, the company overhauled its board, adding five new members as six others departed.

Under new governance, Home Capital abandoned its defiant tone, taking “full responsibility for failing to meet its disclosure obligations to the marketplace,” according to a statement from board chair Brenda Eprile released late Wednesday. The company also agreed to say the OSC “is not to blame for the events of recent months.”

Analysts hailed the settlements as a step forward for Home Capital, avoiding the prospect that the OSC’s enforcement case might continue to dog the company for months to come. Yet, the most crucial questions about its future have yet to be answered: Investors want to see proof that the Home Capital can renew its executive ranks after dismissing CEO Martin Reid in March and sustain its funding base over the long-term.

“The remaining key hurdle (and the most significant) is getting sufficient funding,” said Geoffrey Kwan, an analyst at Royal Bank of Canada Dominion Securities Inc., in a research note. If the lender is to bolster its mortgage book, what matters “is getting depositors to buy [Home Capital’s guaranteed investment certificates] again at levels that don’t just fund renewals, but also fund new originations.”

Mr. Kwan estimates Home Capital needs to sell an average of $23-million in new GICs each business day to replace $5.6-billion in fixed-term deposits maturing over the next year. Although Home Capital’s deposit base, which funds its mortgages, has steadied in recent weeks, it still bleeds small sums on a daily basis. As of June 14, its high-interest and Oaken Financial savings accounts held a combined $244-million, while its GIC balance inched upward to nearly $12.1-billion.

In the meantime, Home Capital’s investors are keen to see the company replace a costly backstop loan at more reasonable terms. An onerous $2-billion credit line from the Healthcare of Ontario Pension Plan that carries a 10-per-cent annual interest rate, has kept Home Capital afloat for now. But finding a better deal could be “the next meaningful positive catalyst” for the company, said Brenna Phelan, an analyst at Raymond James Ltd.

Talks continue with a number of potential lenders, including Canada’s largest banks, according to sources familiar with the process, and Home Capital is seeking a longer term as well as a lower interest rate.

In a statement released Thursday at the urging of the Investment Industry Regulatory Organization of Canada , Home Capital said it is “aware” of media reports about a possible refinancing, but “does not comment on speculation and rumours.”

A separate process to consider selling at least some of Home Capital’s assets is continuing, as private equity groups, such as Onex Corp. and Brookfield Business Partners LP, a unit of Brookfield Asset Management, circle the company.

And Home Capital is still hunting for a CEO with a plan to lead it out of the current crisis, with executive search firm Caldwell Partners in charge of the process.

Under the terms of the OSC settlement, company founder Gerald Soloway will be banned from acting as a director or officer of a public company for four years, and pay a $1-million administrative penalty. Mr. Reid, the former CEO, and ex-chief financial officer Robert Morton each face two-year bans and $500,000 penalties.

Of the three, Mr. Morton is the only one still employed at Home Capital. A spokesperson declined to comment on his status. Home Capital (HCG) Close: $13.67, up $1.54

The Globe and Mail. 16 Jun 2017. Canadian home sales fall 6.2% in May

JANET McFARLAND

Home sales fell across a broad swath of communities around the Greater Toronto Area in May after Ontario’s new housing measures reduced real estate speculation in the region, the Canadian Real Estate Association said.

CREA said national home sales in Canada fell 6.2 per cent in May compared with April on a seasonally adjusted basis, due largely to a 25-per-cent drop in sales in the GTA and significant declines in other communities in the socalled Greater Golden Horseshoe region including Oakville, Hamilton and Barrie.

In the Oakville-Milton area, for example, the number of homes sold in May fell 36 per cent compared with April on a seasonally adjusted basis, while sales in Barrie fell 29 per cent and HamiltonBurlington sales fell 13 per cent. Sales in Kitchener-Waterloo dropped 8.6 per cent in May, although the Peterborough and the Kawarthas area east of the GTA bucked the regional trend and recorded a 9-per-cent increase in sales in May.

The rapid sales decline came after the Ontario government announced a 15-per-cent tax on foreign buyers in April as part of a package of reforms aimed at cooling Toronto’s overheated real estate market.

CREA chief economist Gregory Klump said the May sales reflect the first full month of data since the new rules took effect, and provide clear evidence that the changes have made housing markets “more balanced.”

“This suggests the changes have squelched speculative home purchases,” he said in a statement.

Royal Bank of Canada economist Robert Hogue also credits the province’s changes for the market shift, but says the measures themselves are not having a major direct impact. Instead, he credits a growing market sentiment that the province is determined to cool the market, which is causing buyers to step back “en masse” to reassess.

“I’ve got to admit the reaction has been a bit more swift and strong than I expected at the announcement time, but I think it’s probably a welcome rebalancing of the market,” he said.

Mr. Hogue said some cities around Toronto have not seen as large a drop in sales, but he believes the impact will spread outward if Toronto continues to weaken.

“If we see this cooling in the Toronto area being sustained, I’d be hard pressed to see the other parts of Southern Ontario resisting it,” he said.

However, Hamilton realtor Joe Ferrante said the Hamilton market has remained more buoyant than Toronto’s because buyers still get more value for their money in the city, where prices never rose to Toronto’s heights.

“There’s a lot of value – I don’t think we’ve reached our peak,” he said.

Mr. Ferrante, who is president of Royal LePage State Realty with more than 300 realtors in three offices in Hamilton, said homes are still selling quickly and there has not been an average drop in sales prices.

“It is hot – we’re still seeing multiple offers, we’re still seeing stuff sell within two or three days of listing,” he said.

While the average sale price of homes in the GTA fell 7.3 per cent in May over April on a seasonally adjusted basis, CREA said the MLS Home Price Index (HPI) benchmark price rose 1.24 per cent. While the numbers appear to signal opposite pricing trends, the HPI benchmark reflects prices for similar types of homes each period, while the average sale price depends on the mix of homes sold in the period. That means, for example, that the average price could drop because fewer luxury homes were sold in May.

Across Canada, the index benchmark sale price of homes rose 1.29 per cent in May compared to April with $613,800 nationally. Prices in the Greater Vancouver Region climbed 2.8 per cent to $967,500, continuing Vancouver’s status as Canada’s most expensive housing market.

Bank of Montreal economist Sal Guatieri said cooling in the Toronto region may not last long if Vancouver is any guide; there slumping home sales heated up this spring to hit record highs in May.

Mr. Guatieri said the Toronto region has merely returned “to some semblance of normalcy after a manic winter,” but the supply of houses available for sale is still tight.

“Given the strong economic, demographic and financial backdrop, don’t expect the GTA market to stay down for the count,” he said in a research note. “Policy tinkering will do little to cool demand on a sustained basis.”

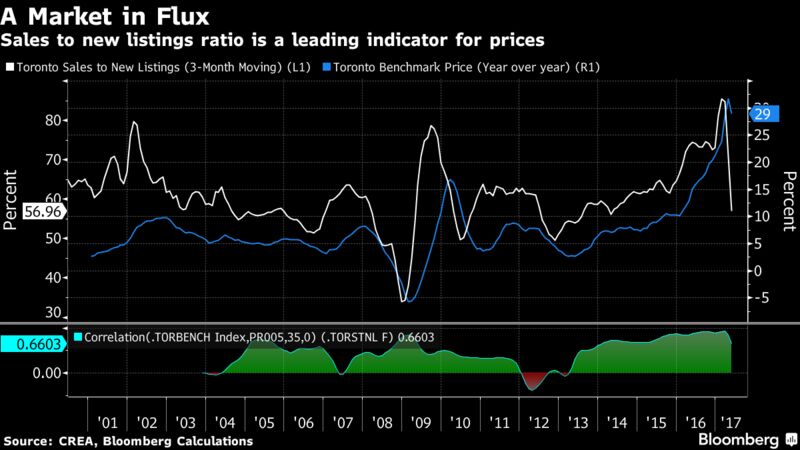

BLOOMBERG. 2017 M06 16. With Sales Gauge at Decade Low, Toronto Home Prices Set to Drop

by Erik Hertzberg

- Ratio of sales to new listings is collapsing at record rate

- New supply, recently announced foreign-buyer tax boost risk

The latest data on Toronto housing show a sharp decline in sales in Canada’s biggest city has yet to trigger a drop in prices. A major indicator of market conditions suggests it will soon enough.

The ratio of Toronto sales to new listings slumped to 41 percent in May, according to Canadian Real Estate Association data Thursday. That’s the lowest since 2008 and near the bottom of the range for what economists generally consider a balanced market.

The gauge is a pretty good predictor of home prices and what it’s showing -- based on the typical historical relationship between the two variables -- is that a modest price decline is probably in the cards.

According to Bloomberg calculations, the 3-month moving average of the sales to new listings ratio explains almost 60 percent of the variation in Toronto benchmark home prices five months later. A sustained ratio of 40 percent implies small, single-digit annual price declines in about half a year.

Just such a soft landing is the prevailing view of most economists, as well as the Bank of Canada. Home prices in the country’s financial capital after all have been climbing steadily for years, and the recent run of annual gains in excess of 30 percent was bound to end. Even amid the sales decline in May, Toronto benchmark prices were up 1.2 percent last month.

The soft landing predicted by the model however assumes a smooth and orderly correction, whereas Toronto housing dynamics seem out of control. Predictions based on historical relationships are less robust in more extreme situations.

So, will the landing be soft or hard?

Soft Landing Case

In its semi-annual financial system review last week, the central bank said a sharp price correction in Toronto and Vancouver is unlikely because strong underlying fundamentals “support the idea that a downturn in prices would be limited.”

That view was given additional credence this week when Governor Stephen Poloz and his Senior Deputy Governor Carolyn Wilkins jolted markets by suggesting the economy may have firmed enough to withstand a gradual withdrawal of stimulus. In effect, the policy makers are saying they’re comfortable enough with the situation in Toronto and Vancouver real estate to risk the potential fallout from higher borrowing costs.

Here are some further arguments for a soft landing:

- As the central bank pointed out, about 40 percent of the 300,000 immigrants who settled in Canada last year moved to Ontario. That bolsters demand. And land-use regulations are often cited as a constraint that will prevent excessive supply from coming on the market.

- The “world-class city” argument stipulates Toronto should be compared with London and Tokyo rather than Ottawa when it comes to real estate valuations, given its status as a major metropolis and North America’s third-largest financial center.

- Vancouver’s recent experience is easing some concern that the market is vulnerable. The imposition of a tax on foreign buyers in the Pacific Coast city last summer spurred declines in sales and prices, but the latest data indicate those are rebounding.

Hard Landing

In January, sales as a share of new listings rose above 90 percent, smashing a record. The decline in that metric since then has been over 50 percentage points, which is the largest and the sharpest in data back to 1988. The only comparable decline in the metric was in the late 1980s, when it fell from 71 percent to 30 percent. And that move, which was followed by a record price drop, took two years to play out.

Much will depend on whether the sales to listings ratio continues falling.

Market psychology is key. There’s been plenty of speculative demand in the market, and any fear of a correction could send investors running for the exits. And a wave of new construction is about to hit the market. Data this month from Canada Mortgage and Housing Corp. showed year-to-date single family completions in Toronto rose to 4,937 units in May -- the most since 2008 and up 19 percent from 2016.

Even the conventional model suggests that in the event the sales to listings ratio starts hovering at about 30 percent, price declines could start hitting double digits.

ENERGY

The Globe and Mail. Jun. 15, 2017. Oil sands firms face stringent emissions caps

KELLY CRYDERMAN AND JEFF LEWIS

CALGARY — Alberta is set to unveil the blueprint for its 100-megatonne cap on greenhouse gas emissions from the province’s oil sands, including a plan for specific project emission permits and penalties if producers do not meet their allocations.

The recommendations from the Oil Sands Advisory Group, not yet adopted by the government, are set to be released by the province in Calgary on Friday – with consultation with communities, industry and other groups to take place in the months ahead.

Right now, the oil sands industry – the fastest-growing source of Canadian GHG emissions – collectively emits about 70 megatonnes a year. Under the advisory group’s plan, the Alberta Energy Regulator would issue annual emission-allocation permits to companies for oil sands projects or facilities, according to sources familiar with the advice to government.

To slow the growth of emissions as new projects or expansions are proposed, the permitting system will become more competitive once the industry as a whole gets closer to the 100-megatonne-a-year cap. Permits would be issued based on past performance on lowering emissions.

The advisory group – made up of industry, environmental and Indigenous members – has made recommendations for financial penalties if producers surpass emission targets. The group has also called for a change to a regulation known as Directive 82, so that the highest-cost, highest-emission bitumen would be left in the ground.

The 100-megatonne cap was the central plank in a climate strategy introduced by the province in 2015 to blunt criticism of fast-growing carbon emissions in the oil sands.

The system laid out by the advisory group is designed to make sure emissions limits are never exceeded but to maintain investor confidence in the province – and to make sure the cap encourages technological innovations to limit emissions.

Alberta is the world’s first major oil-producing jurisdiction to cap emissions, but the plan still allows emissions to grow in the decades ahead. While companies have made strides in lowering the amount of energy it takes to produce a single barrel of oil, overall emissions are poised to soar as production levels rise.

Alberta Premier Rachel Notley’s government is taking flak from many sides as the climate strategy has raised hackles from an energy industry that is already struggling with depressed oil and natural gas prices, and predictions of limited capital spending or growth beyond the near-term completion of large-scale projects. On the other side, environmentalists believe the province’s actions won’t be enough for Canada to meet its international climate-change commitments, including the Paris agreement.

The industry’s carbon footprint has been a major flashpoint as companies seek public support for new pipelines, including Kinder Morgan Inc.’s $7.4-billion Trans Mountain expansion through British Columbia to the Pacific coast.

The plan to nearly triple capacity on the existing line to 890,000 barrels a day was approved by Prime Minister Justin Trudeau last year. But BC NDP Leader John Horgan and Green Party Leader Andrew Weaver, who are poised to assume power in the province, have pledged to block it.

The 18-member Oil Sands Advisory Group was created last year to provide advice on how best to implement the 100-megatonne cap.

The disparate group includes co-chairs David Collyer, former head of the Canadian Association of Petroleum Producers, Tzeporah Berman, an environmental campaigner formerly with Greenpeace and ForestEthics, and Melody Lepine, director of government and industry relations for the Mikisew Cree First Nation.

Companies represented included Royal Dutch Shell, Canadian Natural Resources Ltd., Cenovus Energy Inc. and Suncor Energy Inc. – whose top executives unveiled the emissions cap alongside Ms. Notley at a news conference in late 2015.

The province sought recommendations on a range of potential mechanisms for implementing the policy, including whether changes were required on existing regulations or the permitting process for new developments, according to a mandate letter posted on the government’s website.

Ms. Notley has maintained the differences in opinion have helped in the consensus-building process, and will lead to stronger oil sands policy. Earlier this week, the Alberta Premier told reporters that the idea of leaving some bitumen in the ground was something that could only happen far in the future.

“At a certain point becomes an issue of pace – potentially it could,” she said of oil sands development this week.

The Globe and Mail. Reuters. Jun. 16, 2017. Oil prices bounce but stuck near 2017 lows on supply overhang

LIBBY GEORGE

LONDON — Oil prices edged up from 2017 lows on Friday but remained on track for a fourth consecutive week of losses because of excess supplies, despite OPEC-led production cuts.

Brent crude futures were up 57 cents at $47.49 per barrel by 1224 GMT. U.S. West Texas Intermediate (WTI) crude futures were at $44.85 per barrel, up 39 cents.

“The market took a breather yesterday and is trying to recover somewhat this morning. It is by no means bullish,” said Tamas Varga, analyst at brokerage PVM Oil Associates.

Oil prices are more than 12 per cent below where they were in late May, when producers led by the Organization of the Petroleum Exporting Countries (OPEC) extended for nine months a pledge to cut output by 1.8 million barrels per day (bpd). The cuts had been due to end this month and will now run till March.

Rising U.S. oil output has undermined the impact of OPEC-led cuts. Data from the U.S. Energy Information Administration (EIA) this week showing growing gasoline stocks and shaky demand, despite the peak summer driving season, sent prices tumbling.

“It’s going to be difficult to have a rally unless there’s a disruption or some news from OPEC,” said Olivier Jakob, managing director with PetroMatrix.

Recovering production from Libya and Nigeria, both of which were exempt from OPEC cuts, and high exports and production from Russia were also contributing to the glut. An excess is already building on ships in Asia.

Top producer Russia, not an OPEC member but which signed up to the cuts, is expected to export 61.2 million tonnes of oil via pipelines in the third quarter, equivalent to about 5 million bpd, against 60.5 million tonnes in the second quarter, according to industry sources and Reuters calculations.

In the United States, which is not participating in the deal to reduce production, oil output has risen more than 10 per cent in the past year to 9.3 million bpd. The EIA expects that to rise above 10 million bpd in 2018.

U.S. drilling rig counts due later in the day on Friday could add further pressure, if it shows more were added.

“Oil is unlikely to find solace into the weekend either, with tonight’s Baker Hughes Rig Count expected to deliver its now weekly increase of operational rigs,” said Jeffrey Halley, senior market analyst at futures brokerage OANDA in Singapore.

The Globe and Mail. 16 Jun 2017. Qatar standoff is all about gas, not politics

PATRICIA DeGENNARO, Adjunct professor of International Security at New York University and a U.S. Army contractor with Threat Tec, LLC

Saudi Arabia’s move to blockade Qatar seems a desperate move for the frail kingdom. While competition between the Gulf monarchies is nothing new, the most current move from the Saudi monarchy to punish Qatar for “funding terrorism” may produce an outcome that it fears – not the one it desires.

To be clear, the real reason the Saudi monarchs are isolating Qatar is liquefied natural gas (LNG), not terrorism. That would be the pot calling the kettle black. Qatar sits on one of the largest natural gas reserves in the region, making it the richest country in the Gulf, if not the world. This has given the tiny country diplomatic and economic power to challenge Saudi influence in the region, unlike Bahrain, Egypt and the United Arab Emirates.

The real reason for the Syrian proxy war is the battle for gas lines through tools of government alliances, insurgency and terrorism. Unfortunately, Syria is a necessary conduit for those lines and is suffering the impact of the LNG pipeline fight.

In the mix lies the United States, Turkey, Iran, Israel – an unlikely Saudi bedfellow – and, of course, Russia: All of whom have something to gain, and all who just happen to be extremely active in the fight to keep or oust Syrian leader Bashar al-Assad.

The Saudi move, however, to isolate Qatar may have an unfortunate impact none of these players desire, that is, to further destabilize an already volatile situation.

The instability in the Middle East, North Africa and across the Arabian Peninsula is already rampant with countries funding and arming groups of insurgents, depending on which way the wind blows. All parties – in one way or another – have been funding rebels in the region only to further destabilize it. In addition, you have the United States, Russia, Iran, Turkey and other countries with large military presence further fuelling the destabilization fire.

Enter the blockade on Qatar. This is not easy to implement as countries are much more intertwined. You have Bahrainis living in Qatar, Qataris in the Emirates, Saudis in Qatar and so on. Families are being separated, jobs are being lost, students pulled from their studies and large economic ties frozen hitting business funds and livelihoods alike.

Turkey, Oman, and Iran have set up a sea bridge to bring food and other things to Qatar – other things being military aid to Qatar from Turkey. Qatar houses a large U.S. military base and it will be interesting to see if Turkish support will be welcomed by the United States.

In the middle of all of this is the continued bombardment of Yemen. This, along with the instability in Syria and Iraq, has contributed to one of the largest humanitarian crises in history. The problem is it does not end there. Fallout from this regional crisis reaches into large swaths of Africa and is fuelling global terrorism.

Saudi Arabia, the UAE and Israel are flush with U.S. military weapons. Saudi Arabia is currently using them in Yemen. Now, there are reports that the Trump administration approved a $12billion (U.S.) fighter jet deal with Qatar – even after U.S. President Donald Trump supported Saudi Arabia’s condemnation of the country.

Meanwhile, in Yemen, drones continue to target alleged terrorists; insurgent groups are sending shock waves through Egypt, Iraq, Syria and, most recently, Iran; and the Israel-Palestinian conflict marches on. The humanitarian crisis is on an exponential path to wiping out generations of people who will suffer starvation in lieu of education and will have post-traumatic stress for an unforeseen future ensuring longer conflict and scares.

Unfortunately, the foreign-policy elite is rushing to fuel the Saudi Kingdom’s “terrorist” narrative about Qatar and further claiming Iran is to blame for destabilizing the region. Truthfully, though Iran and Qatar are certainly doing their part, there is a much more dangerous game here focused on LNG.

Making terrorism, and by proxy Qatar and Iran, the culprit is missing the point. These Saudi actions may just cause the destabilization of the Arabian Peninsula – which is on the brink of all-out violence – and the consequences are guaranteed to sting the entire international community.

The international community must step up and hastily find a way to stop the momentum of violence. Calmer minds must prevail. If world leaders don’t take heed now, the conflict will worsen like a wildfire that will not be tamed, which is really not the Saudi Kingdom’s desirable outcome.

CANADA - US

The Globe and Mail. 16 Jun 2017. U.S. ambassador pick moves in many circles. Craft would be taking the role at a crucial time between Canada and the United States as they embark on a renegotiation of NAFTA. She’ll be a phenomenal ambassador. She’s somebody who moves in circles where people have global businesses and understand the need for these types of cross-border relationships. She gets it. She understands it. It’s a world she lives in, said Matt Bevin Kentucky Governor

BILL CURRY

Taking a break from March Madness, America’s annual obsession with college basketball, Kelly and Joe Craft flew into Dallas to see the NBA’s Toronto Raptors play a Monday night game against the Mavericks.

Ms. Craft has known Raptors coach Dwane Casey since they were both students at the University of Kentucky in the 1970s and Mr. Craft’s grandson was eager to meet the Raptors’ star shooting guard, DeMar DeRozan. The special trip was organized to mark his 13th birthday.

“Their grandson is a huge DeMar DeRozan fan,” Mr. Casey said in an interview with The Globe and Mail. “I took him in the locker room and introduced [Mr. Craft and his grandson] to the players and said that his grandmother was going to be the ambassador – she has to go through confirmation and all that – but she was going to be the ambassador for the U.S. in Canada.”

A Republican fundraising power couple whose lives revolve around hoops, education and Republican politics is preparing to represent the United States in Canada’s capital. The Globe and Mail first reported in February that Ms. Craft was under serious consideration by U.S. President Donald Trump. But it was not until Wednesday evening that the White House made it official.

The appointment must still be approved by Congress through a confirmation process, meaning it is not entirely clear how much longer the U.S. embassy in Ottawa will continue to operate without a permanent ambassador. Former ambassador Bruce Heyman, a Democratic fundraiser, stepped down in January.

The ambassador position will be an important link between the two governments as they embark on a renegotiation of the North American free-trade agreement, which is expected to begin this summer. Prime Minister Justin Trudeau’s senior staff and Canada’s ambassador to Washington, David MacNaughton, have already established direct links with Mr. Trump’s senior advisers in the White House. Cabinet ministers and provincial officials have also been making frequent trips south in the hope of preventing radical policy changes that would hurt the Canadian economy.

Ms. Craft has close and longstanding relationships with VicePresident Mike Pence and senior Republican members of Congress, people who will also play a key role in any policy changes that affect cross-border trade.

The Crafts are known as wellconnected fundraisers who have raised millions for Republican politicians and the University of Kentucky. Ms. Craft also has a long history of organizing and fundraising for numerous charities.

In 2015, they donated $4-million (U.S.) to Kentucky’s Moorhead University to launch the Craft Academy for Excellence in Science and Mathematics, a two-year program that offers free tuition and housing for gifted students in their final two years of high school to study at the university.

They are passionate fans of the Kentucky men’s basketball program, a perennially star-studded team that practises in a state-ofthe art athletic facility named after Joe Craft.

“Both of them are very beautiful people, giving people, down to earth. There’s no pretense about

either one of them,” said the Raptors’ Mr. Casey, who supports the appointment even though he has been a vocal critic of Mr. Trump and his policies.

Ms. Craft grew up in the small town of Glasgow, Ky. – population 14,339 – and ran a marketing and consulting company in Lexington, Ky., where she raised two children from a previous marriage. She was appointed in 2007 by then-president George W. Bush as an alternate delegate to the United Nations general assembly, a short-term assignment that included speaking at the assembly about U.S. support for Africa.

In a 2007 interview with the Glasgow Daily Times, she said she hoped to focus on children’s issues and “social, humanitarian and cultural issues” while at the UN.

Zalmay Khalilzad, who was the U.S. ambassador to the UN when Ms. Craft was there, describes her as smart, politically connected and a quick study. Mr. Khalilzad notes that in an era in which communication is easy and travel is cheap, officials can be in regular contact with their counterparts in other countries. As a result, ambassadors are not the key link between countries that they once were.

“The role of the ambassador is important, but different. Not as decisive as in the past,” he said. “This is an issue that all ambassadors, especially in Western countries, representing the United States have. … She will have an important role nevertheless, but there will be this complexity.”

Ms. Craft has made few public comments over the years but she took on a higher profile in politics after entering into a relationship with Joe Craft, to whom she is now married. Mr. Craft is the billionaire president of Alliance Resource Partners, the secondlargest coal producer in the eastern United States.

Mr. Trump campaigned on a pledge to bring back jobs in the American coal sector. That puts the United States at odds with the priorities of Canada’s Liberal government, which is encouraging provinces to phase out the use of coal as part of a national climate-change plan.

The couple served as the Kentucky state finance chairs for Republican Mitt Romney’s unsuccessful presidential campaign in 2012. They have supported other prominent Republicans over the years, including Mr. Pence, Senate Majority Leader Mitch McConnell – who is from Kentucky – and House Speaker Paul Ryan. During last year’s presidential campaign, the couple announced they would be supporting the Trump campaign after receiving assurances that he would not aim to replace Mr. McConnell or Mr. Ryan.

The couple is also close with Kentucky Governor Matt Bevin, a Republican who won in 2015 by campaigning as an establishment outsider in a way that has drawn comparisons to Mr. Trump. They co-chaired the inauguration committee in 2015 following Mr. Bevin’s election victory.

In an interview, Mr. Bevin said the Crafts understand the importance of global trade and are good at bringing people together, two factors that will benefit both countries.

“She’ll be a phenomenal ambassador,” Mr. Bevin said in an interview. “She’s somebody who moves in circles where people have global businesses and understand the need for these types of cross-border relationships. She gets it. She understands it. It’s a world she lives in. She understands the significance of making sure that that is still possible. So I think she’ll be an ally for both of us, because frankly all our interests are aligned.”

Mr. Bevin said strong relationships have developed in recent months between state governors and provincial officials and he does not expect problems between the two countries over trade even as changes are proposed to NAFTA.

“I don’t think it’s going to be that big of a deal. You’re our biggest trading partner by far,” he said. “I’m not even a little bit worried that this will end up in some kind of a dispute.”

The ability to take on large projects such as an inauguration or fundraising and complete them well is frequently cited as one of Ms. Craft’s strengths, according to those who know her.

“Kelly’s got a reputation for taking on big assignments and getting them done,” said Jim Gray, the mayor of Lexington, a Democrat who grew up in the same town as Ms. Craft and went to the same church. “I would say that everything she decides to do, she does it with precision and skill and passion and commitment and she’s a very quick study.”

Mr. Gray said the Crafts are Republicans who will work across party lines.

University of Kentucky men’s basketball coach John Calipari, who has an office in the Joe Craft Centre on campus and has accompanied the couple as they interacted with politicians in Washington, said the new ambassador has strong connections with decision-makers.

“The relationship with the United States and Canada – we know the importance of it. That person has to have the ear of the leadership in our government, and she does,” he said in an interview. “If she calls, they’re going to pick up that phone call. I also think that the people of Canada will enjoy who she is, what’s she’s about. You want somebody that has some presence, and she does.”

AVIATION

The Globe and Mail. 16 Jun 2017. Bombardier, defiant, presses on with C Series sales pitch

NICOLAS VAN PRAET

Fred Cromer Bombardier’s president of commercial aircraft We sort of view this complaint as a way to stifle innovation and direct people to existing products that don’t deliver the same economics and the same superior performance in this size aircraft that we’re delivering.

Bombardier Inc. is pressing ahead with sales campaigns around the world for its C Series airliner in the face of trade challenges from the United States and Brazil, saying that the industry wants the innovation the airplane brings and that it should not be stuck with older, inferior aircraft.

Just days ahead of the most important airshow of the year, at Paris’s Le Bourget airfield, Fred Cromer, Bombardier’s president of commercial aircraft, struck a confident tone when asked about trade challenges against the plane maker’s flagship C Series that have dominated news headlines in recent months.

Mr. Cromer said the complaints by U.S.-based Boeing Co. and Brazil’s Embraer SA are having no negative effect on Bombardier’s efforts to sell the C Series plane, and that the company welcomes the attention. He said his rivals are trying to smother the natural technological progress the sector needs for narrow-body aircraft.

“I don’t think it’s slowing us down at all,” Mr. Cromer told reporters in a conference call on Thursday when asked about Boeing’s latest challenge.

“This complaint, it’s a little bit of a detractor. But at the same time, the industry wants innovation. We’re delivering innovation. We sort of view this complaint as

a way to stifle innovation and direct people to existing products that don’t deliver the same economics and the same superior performance in this size aircraft that we’re delivering.”

The C Series, Montreal-based Bombardier’s new 100- to 150-seat plane, is the first clean-sheet design of a single-aisle airliner in nearly 30 years. It is the company’s big bet to drive aerospace revenue over the next generation.

Boeing in April petitioned the U.S. Department of Commerce and the U.S. International Trade Commission to investigate the C Series, alleging Bombardier used government aid for the aircraft to offer it at less than fair value to U.S.-based customers. Boeing is asking the United States to impose tariffs on the plane when it is sold into the country. A preliminary decision on the matter earlier this month went against Bombardier when a U.S. trade court ruled Boeing might have been harmed by the C Series.

The allegations opened a new battle in a growing trade war between the United States and Canada. Many industry observers say Boeing is taking advantage of a new mantra in the Trump-led White House to get tough on trade.

Brazil in February filed a separate complaint to the World Trade Organization against Canada’s aid for Bombardier. The country acted on allegations by homegrown plane maker Embraer that the federal government’s $372.5-million cash pledge for Bombardier earlier this year amounts to illegal subsidies that distort the global market for airplanes.

Mr. Cromer said potential customers are more focused on how the C Series might fit into their fleet plans and operations than about the trade disputes. He said the specific sales campaigns that are at issue in the Boeing complaint involve 100-seat aircraft, a product Boeing does not even offer. “I think the facts are going to be on our side,” he said.

Others are not so sure. Ottawabased trade consultant Peter Clark says Washington has changed the U.S. trade remedy system in recent years to favour complainants, not respondents. “The chances of a [final] injury finding are much higher than the chances of Bombardier being let off,” he said.

Bombardier has orders for 360 C Series aircraft as of the end of 2016, meaning its output is essentially sold out through 2020. The smaller, 110-seat CS100 model has a list price of $79.5-million (U.S.) while the larger, 130-seat CS300 goes for $89.5-million.

Order activity in the industry for planes of all sizes is slow at the moment. Bombardier has not announced a major new order for the C Series in 14 months. Two airlines are currently flying the aircraft as launch customers: Deutsche Lufthansa AG’s Swiss, and Air Baltic.

Despite the soft market, interest in the C Series is growing, Mr. Cromer said. If his team can build on that enthusiasm and get closer to clinching deals, the Paris air show will be positive for the company, Mr. Cromer said.

“You go there and you show your product line, you continue to generate interest and you advance your conversations,” Mr. Cromer said. “To me, that’s success.” Bombardier (BBD.B) Close: $2.43, up 1¢.

TRADE PROMOTION

Global Affairs Canada. June 16, 2017. Delegation of woman business owners to attend Business Development Conference and Business Fair in Nevada

Ottawa, Ontario - Canada is committed to advancing a progressive trade agenda that addresses issues such as gender equality to ensure that all segments of society can take advantage of the opportunities that flow from trade and investment.

In keeping with this commitment, Global Affairs Canada’s Business Women in International Trade (BWIT) program is leading a delegation of more than 50 woman business owners to attend the annual Women’s Business Enterprise National Council’s (WBENC) National Conference and Business Fair, held in Las Vegas, Nevada, from June 18 to 22, 2017.

The business development conference and business fair is the largest event of its kind for woman business owners. It is an important venue for businesswomen who want to access supplier diversity opportunities with Fortune 500 companies, and offers invaluable opportunities to network with potential partners from around the world and with other Canadian businesswomen.

Quotes

“Empowering women through entrepreneurship and leadership is at the core of Canada’s progressive trade agenda. Trade missions offer important opportunities to help advance the success of businesswomen, which, in turn, contributes to our overall economic growth and competitiveness.”

- François-Philippe Champagne, Minister of International Trade

Quick facts

- According to BMO, businesses that are majority woman-owned contribute almost $150 billion to the Canadian economy annually and employ more than 1.5 million people.

- BWIT is celebrating its 20th anniversary in 2017. The BWIT program has helped hundreds of Canadian women achieve their international business goals by providing services and tools to help woman entrepreneurs access new market opportunities overseas.

________________

LGCJ.: