CANADA ECONOMICS

FOREIGN POLICY

EDC. JUNE 8, 2017. Weekly Commentary. Diversification: In Vogue Again

By Peter G Hall, Vice President and Chief Economist

We never learn, do we? When that big basket of ours seems like the best thing going, what do we do? We put all of our eggs into it – or most of them, anyway. Seems like it happens over and over again: when things are going well with our top client, we put our full weight into serving them. When it’s the big thing we do in our economy – like energy, other resources, a key manufacturer – we really love the good times, and they distract us from the other things we do, or could be doing. And there’s always that critical international client, which in the case of the Canadian economy is the US market. Then when something goes wrong, invariably we say, “We should have diversified!”

Well, the ‘D’ word is back in vogue. US anti-trade talk has turned into action, and has a lot of Canadian exporters worried. The Trans-Pacific Partnership was one of the Administration’s earliest casualties, and NAFTA renegotiation is now on the August 2017 docket. Individual industries have alternately been in the crosshairs: the new President took early aim at the auto sector. Expiry of the Softwood Lumber Agreement fell into the Administration’s lap, and it hasn’t missed an opportunity to talk tough. Canada’s dairy industry has also been singled out as a target. Attacks on trade may become a tax on trade that is perhaps the most damaging overall proposal to date. Without concrete policies to react to, business on both sides of the border is in a quandary, not quite sure how to strategize.

Ideas are flying fast, and one of them is the old stand-by, diversification. Canada remains highly exposed to the US market, which under normal conditions would be a great thing. Growth stateside is setting the pace for the developed world, and new and exciting developments suggest an upswing that can be sustained for a number of years. Current Canadian export activity reflects this – growth in international shipments of our merchandise has risen at an annual rate of over 18 per cent since June of 2016, and the US market is a key driver of the activity. With that now at risk, exporters are looking at other markets as a form of sales insurance. What are the prospects?

Just in time, Canada is inking the CETA agreement with Western Europe. Sure, Brexit has raised a key existential question for the EU, but it seems that nobody over there is actually giving up on trade mechanisms. First, the dependency is so high. Second, anti-trade parties seem more recently to be losing elections. And third, Britain is doing all it can to secure the trade relationships it already has, and to ink even more agreements. Key Canadian exporters, like the agri-food and auto industries and others besides, stand to gain from the deal, which seems bound to diversify Canada’s trade among developed economies.

What about fast-growing emerging markets? Here, Canada is already on the move. In 2000, we shipped just 5 per cent of our goods to emerging markets. By 2008, it was 12 per cent, an extraordinary increase over such a short span. Emerging market woes in recent years haven’t rolled this back: the share hit 13 per cent in 2013, and has held steady since. The bulk of this – 86 per cent – is in three markets, China, Mexico and India, respectively, but others are also rising at a torrid pace.

The diversification runs deep. All of Canada’s provinces are participating. Saskatchewan is a standout, head and shoulders above the rest. British Columbia is also impressive, with 25 per cent of its goods headed for the emerging world. It has also seen the most progress since 2000, rising from an initial share of just 8 per cent. Ontario was the least active in emerging markets in 2000, and has only moved up one spot since. In contrast, Quebec went from being below the national average to slightly above by 2016.

All industries are also more into the emerging world than they were back in 2000. Top of the heap is the agri-food sector, while the auto industry is a notable laggard. The most improved? It’s actually hard to pin down. Resource exports show well, but higher-valued exports are generally keeping up.

The bottom line? Diversification is not just a good idea; it’s alive and well in Canada. Increased emphasis on this in the coming months and years may well see the rate climb. Given superior emerging market growth, it’s also likely to happen organically. It should boost the bottom line, and the predictability of sales.

HOUSING BUBBLE

StatCan. 2017-06-08. New Housing Price Index, April 2017

New Housing Price Index — Canada

April 2017

0.8% increase (monthly change)

Source(s): CANSIM table 327-0056.

Buyers of new homes in Canada saw prices rise 0.8% in April, the largest monthly increase since May 2016. Higher prices in Toronto and Vancouver led the gain.

Chart 1 Chart 1: New Housing Price Index

New Housing Price Index

New Housing Price Index, monthly change

Toronto (+2.1%) and several surrounding census metropolitan areas (CMAs) in Ontario posted the largest gains of the 13 CMAs with price increases in April. Builders in Toronto tied the rise to favourable market conditions and a shortage of developed land.

Builders in London cited improved market conditions, higher construction costs and a shortage of developed land as reasons for the 2.0% increase in new house prices.

In St. Catharines–Niagara (+1.8%) and Oshawa (+1.4%), builders linked higher prices to market conditions. Builders in Kitchener–Cambridge–Waterloo (+1.5%) reported price increases due to higher construction costs.

New house prices in Vancouver (+1.2%) rose for a second consecutive month. The increase reflected market conditions, higher construction costs and new phases of development.

Prices were down in two metropolitan areas—Halifax and Edmonton both posted 0.2% declines—and were unchanged in 12.

New Housing Price Index, 12-month change

New house prices in Canada increased 3.9% over the 12-month period ending in April. The national rise was the largest since May 2008 and was led by the increase in Toronto (+9.9%).

Chart 2 Chart 2: The metropolitan region of Toronto posts the highest year-over-year price increase

The metropolitan region of Toronto posts the highest year-over-year price increase

St. Catharines–Niagara (+7.2%), Windsor (+6.5%) and Kitchener–Cambridge–Waterloo (+6.4%) also posted notable year-over-year increases.

Declines were recorded for six metropolitan areas, with St. John's (-0.7%) and Edmonton (-0.6%) posting the largest decreases. Year over year, prices for all surveyed metropolitan areas in Alberta and Saskatchewan were down for an eighth consecutive month.

Chart 3 Chart 3: Housing completions 1967 - 2016

Housing completions 1967 - 2016

FULL DOCUMENT: http://www.statcan.gc.ca/daily-quotidien/170608/dq170608a-eng.pdf

REUTERS. Jun 8, 2017. Canada April new house prices jump 0.8 percent as Toronto surges

OTTAWA (Reuters) - New housing prices in Canada jumped by 0.8 percent in April from March, the biggest gain in almost a year, amid keen buyer interest in the hot markets of Toronto and Vancouver, Statistics Canada said on Thursday.

The monthly increase was the biggest since the 0.8 percent advance recorded in May 2016. Compared to April 2016, new house prices leapt by 3.9 percent, the highest year-on-year since the 4.1 percent seen in May 2008.

The data will undoubtedly fuel worries about a potential housing bubble in Vancouver and Toronto, where prices grew by the most in 28 years. Bank of Canada Governor Stephen Poloz last month said hefty Toronto home prices increases were not sustainable.

Prices in Toronto, which accounts for 25.49 percent of the Canadian market, surged by 2.1 percent, the highest month-on-month advance since the 2.8 percent recorded in March 1989. Builders cited a shortage of developed land as one reason.

Vancouver prices climbed by 1.2 percent, their second consecutive advance. Vancouver is the largest city in the Pacific province of British Columbia, where the government imposed a 15 percent property transfer tax on foreign real estate buyers last August.

The price index excludes apartments and condominiums, which the government says are a particular cause for concern and which account for one-third of new housing.

(Reporting by David Ljunggren; Editing by Chizu Nomiyama)

REUTERS. Jun 8, 2017. Canada housing starts slip more than expected in May

OTTAWA (Reuters) - Canadian housing starts dipped in May as construction intentions fell in the major cities of Toronto and Vancouver, data from the Canada Mortgage and Housing Corporation showed on Thursday.

The seasonally adjusted annual rate of starts declined to 194,663 in May from April's upwardly revised 213,498. May's figure was a bigger decline than economists' expectations for a decrease to 205,000.

(Reporting by Leah Schnurr)

BANK OF CANADA. 8 June 2017. Household vulnerabilities have moved higher, but the financial system remains resilient

Ottawa, Ontario - Household indebtedness and housing market imbalances—the most important vulnerabilities for the Canadian financial system—have moved higher over the past six months, the Bank of Canada said today in its Financial System Review (FSR). However, “the financial system remains resilient, and macroeconomic conditions continue to improve,” said Governor Stephen S. Poloz.

Household indebtedness has continued to rise in Canada, driven in large part by growth in mortgage lending in the Toronto and Vancouver areas. Recent federal government measures are improving credit quality in the insured mortgage market. At the same time, the share of uninsured mortgages is increasing, especially in markets with high house prices, with some mortgages showing riskier characteristics.

Imbalances in the Canadian housing market have also grown since December, mainly due to an acceleration in prices in Toronto and surrounding areas. While strong fundamentals are supporting price growth in both the Toronto and Vancouver areas, extrapolative expectations are also playing an important role. Macroprudential and housing policy measures are, however, expected to help mitigate this vulnerability over time.

In this FSR, the Bank assesses two separate risk scenarios related to these vulnerabilities.

The first risk scenario focuses on the financial stability implications of an externally generated severe recession, where a nationwide correction in house prices is only one of the channels through which the economy and the financial system are affected. A rise in unemployment and a decline in household income would impair the ability of some households to service their debts, potentially generating broad financial system and economic stress. This risk has a low probability of materializing, but would have a severe impact should it occur. Improving macroeconomic conditions have reduced the probability of this risk occurring.

The second risk scenario looks more narrowly at a significant house price correction in Toronto, Vancouver and their surrounding areas. A decline in house prices in these areas would be unlikely to generate the kind of widespread rise in unemployment and fall in business profitability assumed in the first risk scenario. As a result, while the likelihood of this second risk scenario materializing is higher than that of the first, its impact would be less severe.

Other risks highlighted in the FSR are a sharp increase in long-term interest rates driven by higher global risk premiums and stress emanating from China or other emerging-market economies. The risk of prolonged weakness in commodity prices, which was rated as low in the December 2016 FSR, has now been removed. The economy’s adjustment to lower oil prices is largely complete, and the financial system has been able to manage the negative effects on households and businesses in commodity-producing regions.

The June issue also features three reports written by Bank of Canada staff:

- Using Market-Based Indicators to Assess Banking System Resilience

- Canada’s International Investment Position: Benefits and Potential Vulnerabilities

- Project Jasper: Are Distributed Wholesale Payment Systems Feasible Yet?*

* first published on 25 May 2017

FULL DOCUMENT: http://www.bankofcanada.ca/wp-content/uploads/2017/06/press_080617.pdf

REUTERS. Jun 8, 2017. Debt, housing drive up household vulnerabilities: Bank of Canada

OTTAWA, June 8 (Reuters) - - Rising consumer debt in Canada and an increasingly unbalanced housing market have boosted household vulnerabilities in the last six months but the nation's financial system remains resilient, the Bank of Canada said on Thursday.

Pointing to Canada's two largest housing markets, Toronto and Vancouver, where prices have more than doubled in recent years, the bank said there is an "increased likelihood of a price correction that could lead to financial stress."

In its semi-annual Financial System Review, the central bank said household indebtedness and housing market imbalances, the most important vulnerabilities for the Canadian financial system, have moved higher since December 2016.

While new housing policy measures should help mitigate the vulnerabilities over time, the share of uninsured mortgages is increasing and some mortgages are showing riskier characteristics, the bank said.

It warned that the overall level of mortgage debt relative to income continues to rise, and said the greater use of home equity lines of credit could be contributing to vulnerabilities because that borrowing makes it harder for lenders to spot emerging credit problems.

(Reporting by Andrea Hopkins and Leah Schnurr)

BLOOMBERG. 2017 M06 8. Bank of Canada Sees Risks Spilling Over Into Uninsured Mortgages

by Theophilos Argitis

The Bank of Canada said financial system vulnerabilities associated with household debt have increased in recent months, as a combination of surging home prices in Toronto and Vancouver and tighter qualification rules for insured home finance drive growth in uninsured mortgages.

In its semi-annual report on the financial system, Canada’s central bank paints a picture of a housing market where government mortgage tightening measures are being offset by the growing costs for buying homes in Toronto and Vancouver.

Measures by the federal government last year to tighten qualification rules has improved the credit quality of the insured mortgage sector, the central bank said. Those measures though may be pushing more higher-risk borrowers into the uninsured space, the Bank of Canada said.

“Some potential borrowers have likely chosen to purchase less expensive homes, some have chosen to delay their purchases, and others may have increased their down payments and taken out low-ratio mortgages,” it said.

The Bank of Canada also commented on the situation at Home Capital Group Inc., saying the “first steps” of a market-based solution have emerged, adding that the market expects the situation is largely isolated to the troubled lender.

Key Points

- There are growing worries about uninsured mortgages, which are increasing as a share of total mortgages. Not only is the uninsured sector growing, but the Bank of Canada is seeing some riskier mortgages within that area.

- Worries include the growing use of home equity lines of credit that have been growing at rates above income growth since early 2016.

- The quality of credit has improved significantly for high-ratio mortgages (those with down payments of less than 20 percent), amid a decline in share of highly indebted borrowers. The volume of insured mortgages has also decreased.

- Housing market imbalances have also risen over the past six months, increasing vulnerabilities to a housing correction. Still, macro-prudential and housing policy measures will help mitigate this vulnerability over time.

Other Details

- While fundamentals remain strong in Toronto and Vancouver housing markets, they can’t explain recent price gains. “Extrapolative expectations” and speculation have become more pervasive.

- Foreign buyer taxes typically have a temporary effect. That includes the tax introduce in Ontario in April.

- The Bank of Canada flags concern that “could arise if a significant proportion of the funding for down payments comes from other forms of borrowing, rather than from personal savings or friends and family.”

- Not enough data to assess how frequently co-lending arrangements occur when a mortgage is bundled with a second loan. Increased funding for low-ratio mortgages isn’t coming from portfolio insurance, which is declining. There may be some growth from private lenders who operate outside the regulated market

- There are changing characteristics of low-ratio mortgages that suggest increased risk. Highly indebted borrowers are choosing higher down payments to get around more stringent mortgage qualification rule. The share of low-ratio mortgages with amortization periods longer than 25 years now makes up more than half of all borrowers.

REUTERS. Jun 8, 2017. Home Capital shows risk of less-stable funding: Bank of Canada

OTTAWA, June 8 (Reuters) - - The recent funding and liquidity strain at Home Capital Group (HCG.TO: Quote) highlighted the vulnerability associated with overreliance on less-stable funding sources and the sensitivity of depositors to the business prospect of mortgage lenders, the Bank of Canada said on Thursday.

In its semi-annual Financial System Review, the central bank said the market largely viewed the alternative lender's situation as "idiosyncratic to" Home Capital, which accounts for about 1.5 percent of Canadian mortgage lending.

"Market participants have remained confident in the capital and liquidity position of other Canadian lenders," the bank said in the review.

The rapid withdrawal of deposits at Home Capital beginning in April coincided with allegations made by the Ontario Securities Commission that the company failed to adequately disclose a 2014-2015 review of mortgage origination business partners and underwriting processes, remediation actions and associated effects on business operations, the bank said.

It said depositors were sensitive to information about the lending industry amid rising household indebtedness and housing market imbalances - the two biggest vulnerabilities to Canada's financial system.

"This focus was particularly acute for HCG because its main business is mortgage lending to borrowers who do not meet all the lending criteria of traditional financial institutions," the bank said.

It added that federal financial sector authorities are "working collaboratively" to monitor the situation at HCG, which said in late May that it continues to work on developing longer-term liquidity solutions.

(Reporting by by Andrea Hopkins)

BANK OF CANADA. 8 June 2017. Financial System Review - June 2017

This issue of the Financial System Review reflects the Bank’s judgment that household indebtedness and housing market imbalances–the most important vulnerabilities for the Canadian financial system–have moved higher over the past six months. However, the financial system remains resilient, and macroeconomic conditions continue to improve. Other vulnerabilities discussed in this FSR are fragile fixed-income market liquidity and the capacity of an interconnected financial system to mitigate cyber threats.

FULL DOCUMENT: http://www.bankofcanada.ca/wp-content/uploads/2017/06/fsr-june2017.pdf

BANK OF CANADA. 8 June 2017. Using Market-Based Indicators to Assess Banking System Resilience (Financial System Review - June 2017)

Cameron MacDonald

Maarten van Oordt

This report reviews the use of quantitative tools to gauge market participants’ assessment of banking system resilience. These measures complement traditional balance-sheet metrics and suggest that markets consider large Canadian banks to be better placed to weather adverse shocks than banks in other advanced economies. Compared with regulatory capital ratios, however, the measures suggest less improvement in banking system resilience since the pre-crisis period.

FULL DOCUMENT: http://www.bankofcanada.ca/wp-content/uploads/2017/06/fsr-june17-macdonald.pdf

The Globe and Mail. Jun. 08, 2017. The one housing-market fix that Canada hasn't tried

DAVID PARKINSON

The Organization for Economic Co-operation and Development has come right out and said it: A lot of Canada’s housing-market fever could be treated with an injection of higher interest rates.

If the international economic-policy body’s new economic forecast is on target, it may get its remedy soon enough – even if the Bank of Canada isn’t sold on the OECD’s housing prescription.

In its semi-annual Global Economic Outlook, released Wednesday, the OECD increased its calls for Canadian policy makers to address the housing excesses in the key Toronto and Vancouver regions. After observing a spring in which the huge Toronto housing market soared to dizzying heights, propelling the economic and policy rhetoric along with it, it seems the OECD had seen enough.

It questioned the longer-term efficacy of the foreign-buyers taxes imposed in recent months in Vancouver and Toronto. It fretted about Ontario’s expansion of rent controls, saying they could choke off new rental supplies and hamper poor and young Canadians. It called for tougher debt-to-income requirements for mortgage borrowers specifically targeted at “regions where house prices are inflated relative to fundamentals.”

But the real attention-getter was what it had to say about the prospect for higher interest rates from the Bank of Canada.

“Raising interest rates will reduce overheating in housing markets, which poses economic and financial stability risks and has made housing increasingly unaffordable, especially in Toronto and Vancouver,” the report said.

This isn’t the first time the OECD has drawn a link between Canada’s low interest rates and its surging regional housing prices and high household debts. But never before had it so strongly and clearly championed higher rates as a big part of the solution to Canada’s housing excesses. In its previous economic outlooks and quarterly updates over the past year or so, it has largely agreed with the Bank of Canada’s current low-rate policy stance, citing (as the central bank has) the evidence of tame inflation and significant excess capacity in the economy.

The OECD’s position up until now has been an implicit agreement with the Bank of Canada’s consistent argument that higher interest rates are not the right tool to address regional housing problems. Higher rates apply the brakes to a wide swath of economic activity and in all sectors and parts of the country, reaching far beyond one specific industry in a couple of specific regions. The central bank has instead been reserving interest rates to deal with a broader, inflation-fuelling acceleration of the economy – something that it wasn’t seeing in Canada’s economic data.

Until now, neither was the OECD. But the organization’s economic outlook for Canada is suddenly much hotter than it used to be – hot enough, in fact, to have put a rate hike on the radar for economic reasons alone.

The OECD’s new forecast calls for Canada’s real gross domestic product to expand by 2.8 per cent this year. That’s up sharply from 2.4 per cent in the agency’s forecast update just three months ago, and from 2.1 per cent in its last full economic outlook in November.

It should be noted that the OECD is positioning itself at the bullish end of forecasters; even after last week’s strong Canadian first-quarter GDP report, which showed that the economy grew at an annualized pace of 3.7 per cent in the first three months of the year, most prominent private-sector economists were still looking at growth of about 2.5 per cent for all of 2017. The Bank of Canada’s own quarterly forecast, issued in April, called for 2.6-per-cent growth this year.

But if the OECD’s optimism is founded, then the economy will eat up its excess capacity faster than previously anticipated – which is precisely what would compel the Bank of Canada to raise interest rates sooner rather than later. The housing sector would feel the effects of such a move, but needn’t be the impetus for it.

Indeed, the OECD projected that the Bank of Canada will need to start raising rates “towards the end of 2017” – anywhere from three to six months ahead of where most other forecasters put the first rate hike. If it’s right, we’re only a few months away from a splash of cold water on the Toronto and Vancouver housing markets.

Is the Bank of Canada seeing the same thing? Frankly, we don’t really know; in a fast-evolving economy, quarterly projections can feel very far apart. But we might have a better idea in fairly short order.

On Thursday, the central bank releases its semi-annual Financial System Review. That report will not only detail the bank’s analysis of the housing market, but will be followed by a press conference in which Bank of Canada Governor Stephen Poloz will face questions from the media – some of which will surely touch on his current assessment of the economy. Next Monday, Mr. Poloz’s second-in-command, senior deputy governor Carolyn Wilkins, will give a speech in Winnipeg, the title of which is Canadian Economic Update: Strength in Diversity. Those two events should shed at least a little light on the bank’s next quarterly economic forecasts, which come out a little over a month from now, on July 12.

But if there’s a takeaway from the OECD’s report, it’s that the economy’s acceleration has now put a rate increase in sight. And that means that its timing may actually be close to becoming part of the housing discussion, even for officials at the Bank of Canada. It’s no longer inconsistent with the direction the economy is taking the interest-rate outlook anyway.

INVESTMENT

StatCan. 2017-06-08. Canadian portfolio investment abroad, 2016

Canadian holdings of foreign securities increased by 4.2% to $1,741.4 billion at the end of 2016. However, this growth was well below the strong gains recorded in each of the previous four years. Canadian portfolio investment abroad accounted for 40% of Canada's total international assets at the end of 2016, compared with a 25% share 20 years ago.

Higher foreign stock prices and, to a lesser extent, acquisitions of $13.8 billion of foreign securities by Canadian investors in 2016 contributed to the increase. The downward revaluation effect of an appreciating Canadian dollar against most major foreign currencies moderated the overall growth in the value of these assets.

The Canadian dollar appreciated by 3.1% against the US dollar, 6.1% against the euro, 23.2% against the British pound and 0.1% against the Japanese yen in 2016.

Chart 1 Chart 1: Canadian holdings of foreign securities

Canadian holdings of foreign securities

On an instrument basis, holdings of foreign equities were up $67.3 billion to $1,358.3 billion, accounting for 78% of total holdings of foreign securities at the end of 2016. This share has been relatively stable since 2009. At the same time, Canadian holdings of foreign debt instruments edged up by $2.5 billion to $383.1 billion in 2016, following a $90.2 billion increase in 2015.

The majority of portfolio investment assets were denominated in US dollars at the end of 2016. More precisely, 63% of Canadian investors' holdings were in securities denominated in US dollars, while 9% were in euros and 6% in British pounds. Canada's portfolio assets are therefore strongly influenced by changes in the value of the Canadian dollar against foreign currencies, mainly the US dollar.

Chart 2 Chart 2: Currency composition of Canadian portfolio investment assets, 2016

Currency composition of Canadian portfolio investment assets, 2016

Canadian portfolio investment abroad led by holdings of US securities

On a geographical basis, the United States remains the top investment destination for Canadian portfolio investors. Canadian holdings of US securities increased by 6.3% to $1,065.3 billion at the end 2016. Most of this gain was in the form of equities and mainly resulted from higher stock prices. US stock prices were up by 9.4% in the year. Canadian investors had 61% of their portfolio invested in US securities at the end of 2016, compared with a 50% share in 2007 just prior the financial crisis.

Holdings of European securities edged down to $362.7 billion at the end of 2016. The downward revaluation effect of an appreciating Canadian dollar against the British pound resulted in a 3.8% decline to $103.4 billion in holdings of UK securities in 2016. Portfolio assets in other major European countries rose in 2016, notably Germany (+8.8%).

At the same time, holdings of securities from Asia and Oceania edged up to $213.1 billion. Growth in the value of Canadian investors' holdings in most major countries in this region was moderated by a decline in holdings of Chinese securities in the year, mainly from lower equity prices.

Canadian portfolio investment abroad was spread over more than 100 countries at the end of 2016. However, the top three destinations (United States, United Kingdom and Japan) represented over 70% of total Canadian portfolio assets abroad.

Chart 3 Chart 3: Canadian holdings of foreign securities, by major geographic area

Canadian holdings of foreign securities, by major geographic area

FULL DOCUMENT: http://www.statcan.gc.ca/daily-quotidien/170608/dq170608c-eng.pdf

BANK OF CANADA. 8 June 2017. Canada’s International Investment Position: Benefits and Potential Vulnerabilities (Financial System Review - June 2017)

Gabriel Bruneau

Maxime Leboeuf

Guillaume Nolin

While greater global financial integration is beneficial, the authors discuss how foreign capital inflows can also facilitate the buildup of domestic vulnerabilities and potentially lead to destabilizing reversals. Canada’s current international investment position is typical of advanced economies and will likely continue to act as an economic stabilizer. However, the growth and composition of Canada’s international investment position warrant continued monitoring.

FULL DOCUMENT: http://www.bankofcanada.ca/wp-content/uploads/2017/06/fsr-june17-bruneau.pdf

BANK OF CANADA. 8 June 2017. Project Jasper: Are Distributed Wholesale Payment Systems Feasible Yet? (Financial System Review - June 2017)

James Chapman

Rod Garratt

Scott Hendry

Andrew McCormack

Wade McMahon

This report describes a joint endeavour between public and private sectors to explore a wholesale payment system based on distributed ledger technology (DLT). They find that a stand-alone DLT system is unlikely to be as beneficial as a centralized payment system in terms of core operating costs; however, it could increase financial system efficiency as a result of integration with the broader financial market infrastructure.

FULL DOCUMENT: http://www.bankofcanada.ca/wp-content/uploads/2017/05/fsr-june-2017-chapman.pdf

ENERGY - QUATAR

The Globe and Mail. Jun. 08, 2017. Qatar’s economic outlook uncertain as boycott continues

ERIC REGULY - EUROPEAN BUREAU CHIEF

ROME — The images apparently showed a country in near panic. Supermarket shelves were empty, the airports in chaos and the borders jammed with cars. Invasion or natural disaster?

The country is Qatar and it is the victim of neither. Instead, a diplomatic and economic boycott – a blockade, in effect – is under way. Saudi Arabia, the United Arab Emirates, Bahrain and Egypt severed ties with Qatar on Monday and Qataris rushed to the supermarkets to stock up on food and water. The borders were jammed because the countries behind the boycott ordered Qatari diplomats and citizens to leave.

It would seem easy to strangle Qatar. The country forms a peninsula that juts into the western Persian Gulf, its only land border shared with Saudi Arabia. But four days into the boycott, Qatar, an energy powerhouse, seemed far from economic catastrophe.

Still, the fear among the Qataris and the countries that trade with it is that the boycott, if it endures, could do lasting damage to Qatar. “It all depends on how long the standoff lasts,” said Syed Basher, a former research economist at the Qatar Central Bank, now a professor of economics at East West University in Bangladesh.

Damage to the global energy trade is also possible if the boycott is tightened, blocking shipments of oil and liquefied natural gas (LNG) to the export markets. Qatar, a British protectorate until 1971, is a member of the Organization of Petroleum Exporting Countries (OPEC) and the world’s biggest exporter of LNG.

If oil and LNG exports were choked off, Qatar’s lifeblood would drain away quickly and the global energy markets would take a blow. Qatar’s oil and gas exports are intact, though Japan is on edge. Japan depends heavily on imported gas and is the biggest buyer of Qatari LNG.

The Saudi-led boycott was triggered by accusations that the Qataris were supporting Islamist militants and the Muslim Brotherhood, which the Saudis declared a terrorist organization in 2014, and cozying up to Iran, the Saudis’ great regional rival. The boycott is a more serious replay of 2014, when Saudi Arabia, Bahrain and the UAE temporarily suspended relations with Qatar for its support of the Brotherhood.

So far, the energy markets’ reaction to the Qatari crisis has been calm as traders have trouble judging the boycott’s potential impact. A blockade of all tankers calling at Qatar’s ports certainly would rattle the oil and LNG markets, but that hasn’t happened. Nor has OPEC solidarity shattered. Qatar, one OPEC’s smallest oil producers, has given no sign that it wants to sabotage the cartel’s planned production cuts, which are aimed at propping up the price.

Brent crude, the international benchmark, has been gently drifting downward this week, reaching $48 (U.S.) a barrel. Olivier Jakob of the Swiss oil-market intelligence company PetroMatrix, said “the crisis has, for now, [had] a limited impact.”

Kuwait, the Persian Gulf country that is trying to broker a truce between Qatar and its Arab detractors, on Tuesday said that Qatar remains committed to the planned supply cuts of 1.8 million barrels a day by OPEC and non-OPEC countries. Analysts, meanwhile, do not believe that the Saudis will allow the Qatar crisis to escalate into a full-blown energy war.

REUTERS. Jun 8, 2017. Oil falls for second day as concern grows over supply

By Amanda Cooper

LONDON (Reuters) - Oil fell for a second day on Thursday to hit one-month lows after an unexpected surge in U.S. inventories and the return of more Nigerian crude aggravated investor concerns about an already oversupplied market.

The oil price has slipped below $50 a barrel despite a pledge by the world's largest exporters to extend an existing output cut of 1.8 million barrels per day (bpd) into next year in an effort to reduce bulging global inventories.

Adding to concern about supply outstripping demand, Royal Dutch Shell (RDSa.L: Quote) on Wednesday lifted force majeure on exports of Nigeria's Forcados crude, bringing all the country's oil grades fully online for the first time in 16 months.

Brent crude LCOc1 was down 26 cents at $47.80 a barrel by 1137 GMT (7:37 a.m. ET), having touched an earlier high of $48.60, while U.S. crude futures CLc1 fell 25 cents to $45.47 a barrel.

The market has also come under pressure from news of rising output from Libya, which together with Nigeria is exempt from the production cut made by the Organization of the Petroleum Exporting Countries and its 11 partners.

"I've been quite bullish for the second half of this year, based on supply and demand balances and I would still not give up on that idea, that rebalancing is going to start in the second half," PVM Oil Associates strategist Tamas Varga said.

"But if Nigerian and Libyan production is picking up as well as they are now, then slowly, I am probably going to have to start changing my mind."

The most actively traded Brent derivatives were bearish sell options that would give the holder the right to sell at $45 and $46 a barrel between August and December.

U.S. inventories of crude oil and gasoline surprisingly rose last week as refinery runs declined and exports fell, official data showed on Wednesday.

"Unless data are released that make the latest inventory build appear an anomaly, oil prices are hardly likely to make any lasting recovery," Commerzbank said in a note.

Sentiment across the broader financial markets also remained jittery.

Former FBI director James Comey's U.S. congressional appearance, a European Central Bank (ECB) policy meeting and the British general election take place on Thursday.

Many investors are wary ahead of Comey's Senate appearance as they look for any hints that U.S. President Donald Trump may have been engaged in obstruction of justice - an offence that could lead to impeachment hearings.

ECB policymakers are set to take a more benign view of the economy and will even discuss dropping some of their pledges to ramp up stimulus if needed, sources with direct knowledge of the discussions told Reuters.

(Additional reporting by Aaron Sheldrick in TOKYO; Editing by Dale Hudson and David Evans)

REUTERS. Jun 7, 2017. Oil dives 5 percent on surprise build in U.S. crude, gasoline stocks

By David Gaffen

NEW YORK (Reuters) - Oil prices slid 5 percent on Wednesday to a one-month low, after an unexpected increase in U.S. inventories of crude and gasoline fanned fears that output cuts by major world oil producers have not done much to drain a global glut.

Crude stocks in the United States grew 3.3 million barrels to 513 million barrels, according to the U.S. Energy Information Administration (EIA). That confounded forecasters who had predicted a drop of 3.5 million barrels, especially a day after data from the American Petroleum Institute indicated an even bigger fall.

Gasoline inventories also unexpectedly rose, imports increased, and exports dropped, the EIA data showed.

“These figures spell a setback to the joint effort by OPEC and some non-OPEC countries to curb their output," said Abhishek Kumar, senior energy analyst at Interfax Energy’s Global Gas Analytics in London.

"However, without persistent drawdowns in U.S. oil stockpiles, the process could be painfully slow.”

U.S. crude futures settled down 5 percent, or $2.47 a barrel, at $45.72 a barrel, the lowest settlement for U.S. crude since May 4. U.S. benchmark futures CLc1 have slid more than 11 percent in 10 days of trading.

Brent crude prices LCOc1 fell $2.06, or 4 percent to settle at $48.06 a barrel. Official settlement prices were delayed due to a technical issue, according to a Nymex spokesperson.

Gasoline futures 1RBc1 tumbled 4 percent to $1.4921 a gallon, lowest since May 10, as rising inventories fed worries about weak demand. Overall gasoline demand is down 0.7 percent for the past four weeks from a year ago, the EIA said.

"Flagging gasoline demand continues to bedevil the market. With gasoline currently the seasonal leader of the complex, its weakness is dragging everything down," said John Kilduff, partner at Again Capital in New York.

Some in the market remained concerned about the move by OPEC members Saudi Arabia and the United Arab Emirates to cut diplomatic and transport ties with Qatar, an OPEC member that had agreed to cut about 30,000 barrels a day as part of the Organization of the Petroleum Exporting Countries agreement to reduce output.

Some analysts saw a risk that rivalries between OPEC members could weaken the production cut agreement. Some were concerned about rising production from Libya and Nigeria, which are exempt from the agreement.

OPEC and other producers including Russia have pledged to cut output by about 1.8 million barrels per day (bpd).

Royal Dutch Shell (RDSa.L: Quote) lifted force majeure on exports of Nigeria's Forcados crude oil, bringing all the country's oil exports fully online for the first time in 16 months.

(To view a graphic on 'World fuel production vs. consumption' click reut.rs/2r3ZH8Y)

(Additional reporting by Scott DiSavino, Stephen Eisenhammer and Henning Gloystein; Editing by Louise Heavens and David Gregorio)

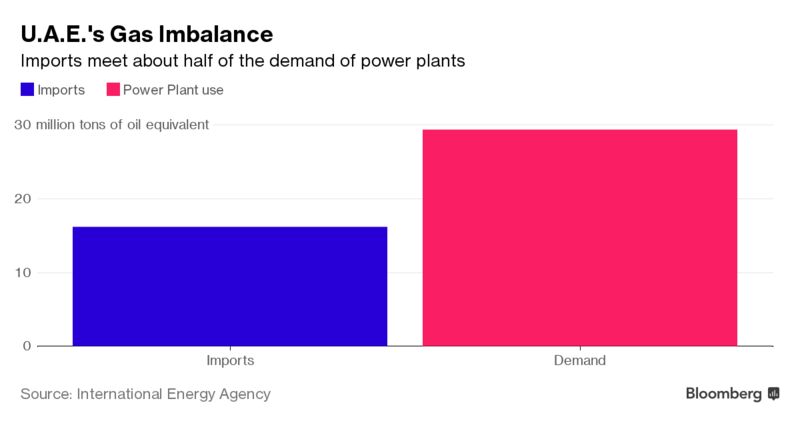

BLOOMBERG. 2017 M06 8. The U.A.E. Needs Qatar’s Gas to Keep Dubai’s Lights On

by Anthony Dipaola

- Pipeline spared as imports generate half of U.A.E.’s power

- Without Qatar gas, Dubai and Abu Dhabi might pay more for fuel

- Abu Dhabi Said to Ease Qatari Vessel Ban

When it comes to natural gas shipments, the United Arab Emirates needs Qatar more than Qatar needs the U.A.E.

The U.A.E. joined Saudi Arabia in cutting off air, sea and land links with Qatar on Monday, accusing the gas-rich sheikhdom of supporting extremist groups. But the U.A.E., which depends on imported gas to generate half its electricity, avoided shutting down the pipeline supplying it from Qatar. Without this energy artery, Dubai’s glittering skyscrapers would go dark for lack of power unless the emirate could replace Qatari fuel with more expensive liquefied natural gas.

What’s the situation for Qatari gas shipments to the U.A.E.?

Qatari natural gas continues to flow normally to both the U.A.E. and Oman through a pipeline, with no indication that supplies will be cut, according to a person with knowledge of the matter who asked not to be identified because the information isn’t public. Abu Dhabi-based Dolphin Energy Ltd., which operates the gas pipeline, declined to comment.

Who are the players behind Qatar’s gas link with the U.A.E.?

Qatar, which has the world’s third-largest gas deposits, sends about 2 billion cubic feet of the fuel a day through a 364-kilometer (226-mile) undersea pipeline. Dolphin Energy, the link’s operator, is a joint venture between Mubadala Investment Co., which holds a 51 percent stake, and Occidental Petroleum Corp. and Total SA, each with a 24.5 percent share. Since 2007, the venture has been processing gas from Qatar’s North Field and transporting it to the Taweelah terminal in Abu Dhabi, according to Mubadala’s website. Dolphin also distributes gas in Oman.

What’s the extent of the U.A.E. ban on shipping with Qatar?

The U.A.E.’s oil ports authority on Wednesday night again restricted international vessels from traveling to and from Qatar, along with Qatar-flagged ships, from entering its harbors. Earlier in the day, Abu Dhabi’s Petroleum Ports Authority had lifted restrictions on international tankers.

The tanker Apollo Dream, which carries about 2 million barrels of crude, loaded at an offshore terminal in Abu Dhabi on Wednesday after being at an offshore terminal in Qatar on Tuesday, according to tanker tracking data on Bloomberg. The vessel is currently outside Saudi Arabia’s Ras Tanura port.

Other U.A.E. ports, including Jebel Ali, the region’s biggest container terminal, and the oil-trading hub at Fujairah are prohibiting all vessels traveling to or coming from Qatar. Royal Dutch Shell Plc diverted a vessel carrying LNG to Dubai’s Jebel Ali port to supply fuel under contract amid the ban on Qatari vessels, FGE Energy said in research note. The tanker Maran Gas Amphipolis moored Thursday, and originally listed Kuwait’s Mina Al Ahmadi as the destination, according to ship data.

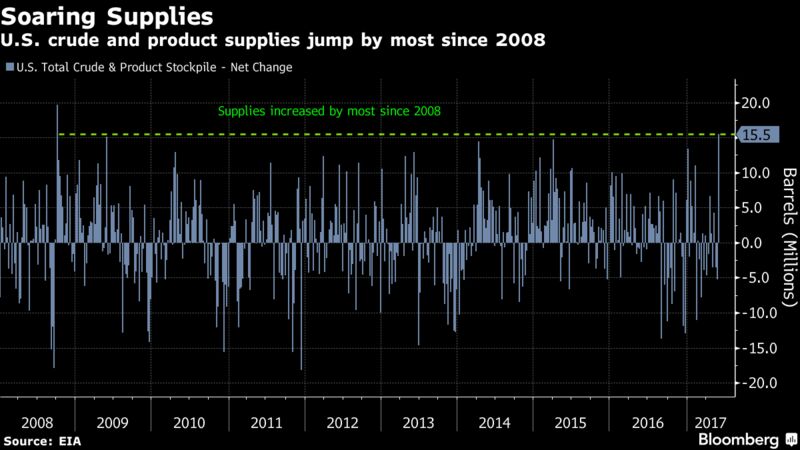

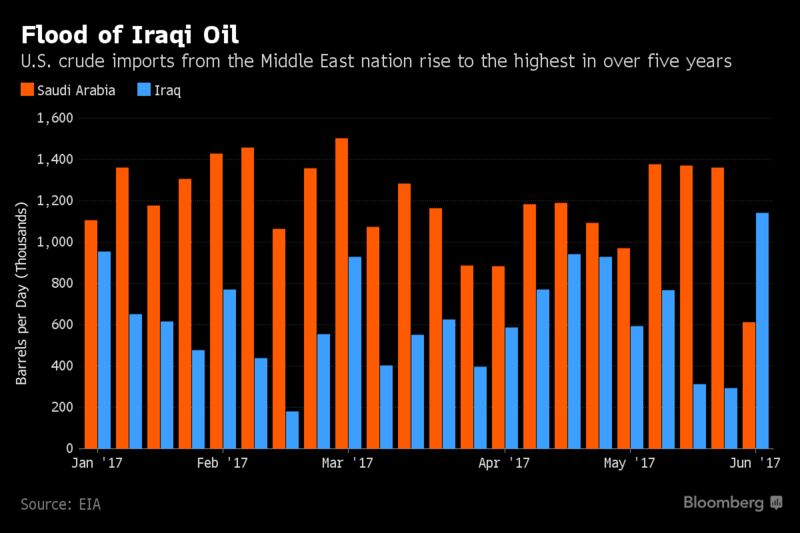

BLOOMBERG. 2017 M06 8. Crude Oil’s Biggest Tumble Since March Shown in Three Charts

by Jessica Summers

- U.S. total crude and products supplies jump by most since 2008

- WTI-Brent spread narrows, encouraging U.S. crude oil imports

- Oil Plunges on Unexpected Build in U.S. Inventories

Oil’s 5 percent tumble Wednesday, the biggest slide since March, followed government data that showed U.S. crude and fuel stockpiles unexpectedly soaring at a time of year when they normally decline. Here are three charts showing what made oil bulls run scared.

Stockpile Surge

Total U.S. inventories of crude oil and products such as gasoline and diesel fuel surged the most since 2008 last week, according to the Energy Information Administration. The 15.5 million-barrel jump took investors by surprise, sending the market off a cliff. What caused the increase? Higher imports of crude, as well as a sharp decline in exports. Add in a 505,000 barrel a day drop in gasoline demand and you end up with growing stockpiles.

“It’s about total stocks, crude and products, because that’s what the world wants to see, that’s what OPEC wants to see," Michael Wittner, head of commodities research at Societe Generale SA in New York, said by telephone. "A week ago, you could say three of the past four weeks, it has come down, you are starting to see a trend develop. And then today, boom, the whole thing falls apart.”

Dynamics Shift

What’s behind the import shift that helped cause the 3.3 million barrel build in nationwide crude supplies? The spread between the global crude benchmark Brent and its U.S. counterpart tightened during the second half of May, shrinking to a premium of $1.99 last week, the smallest since February. A narrower gap encourages imports and makes U.S. exports more expensive relative to oil from elsewhere. Imports rose by 356,000 barrels a day last week, while crude exports fell by 746,000 barrels a day, the biggest drop ever.

Iraqi Imports

Where did the flood of imports mostly come from? Imports from Iraq surged to 1.14 million barrels a day, the most since 2012, according to preliminary EIA data. That more than outweighed a drop in imports from Saudi Arabia, which sank 55 percent to the lowest level since January 2015.

“Today’s report was the straw that broke the camel’s back. We thought there would be no chance of a build in the oil market,” Phil Streible, senior market strategist at RJO Futures in Chicago, said by telephone. There’s a lot of chatter about oil heading back to the $20s again, he said.

AVIATION

REUTERS. Jun 8, 2017. Boeing barrels ahead on 787 and 777 cost reductions

By Alwyn Scott

SEATTLE (Reuters) - Boeing Co is streamlining its aircraft production systems at its largest factory, trying to cut costs to compete with rival Airbus and chip away at the near-$30 billion deficit created by its 787 Dreamliner.

Dozens of complex robots are replacing humans for such mundane tasks as drilling and riveting, and Boeing is reordering some of its assembly steps to speed up the process.

The savings, part of a long-term cost-cutting drive at the world's biggest plane maker that also includes substantial staff reductions, comes as Boeing has spent heavily to develop new aircraft models.

It poured $1 billion into erecting a 27-acre factory to make carbon composite wings for its forthcoming 777X widebody jet. It scaled the factory to produce 100 planes a year. But with only 306 firm orders for the 777X on its books, and the production rate falling, Boeing is challenging workers to find more efficient ways to do the work so it can avoid purchasing some of the planned machinery.

"Frankly, we would like to not to have to buy all of the equipment that we are currently sized for," said Eric Lindblad, vice president of the 777X program, during a recent factory tour. "It's just saving money on capital."

Behind him, only two of six bays built to hold carbon fiber placement machines had been outfitted with all equipment.

Boeing also has set up a temporary low-rate assembly line for initial production (LRIP) of the 777X so it can test processes before hitting the acceleration pedal.

REDUCING RISK OF LEMONS

The "LRIP" strategy comes in part from painful lessons on the 787 line, where early aircraft that came out of the factory needed heavy reworking.

This time, "we are actually testing the primary elements of that new production capability" on the 777, a plane Boeing already knows how to make, said Jason Clark, vice president of 777 and 777X operations.

Final assembly of the 777X begins next year, with testing in 2019 and first delivery in 2020. Lindblad said it might be delivered a quarter early, if customers want, but not in 2019.

On the 787 line, where wings, fuselage and other major pieces are shipped from suppliers and simply assembled at Boeing, the savings options are fewer.

But teams are still taking out costs. They have slashed production time by more than two-thirds in four years through such changes as organizing kits so mechanics have all parts on hand and putting interiors into planes earlier on the assembly line, said Bob Manelski, director of 787 business operations.

Boeing builds the 787 in Everett, Washington, and North Charleston, South Carolina. That allows it to try out new techniques on one line at a time. A year ago, it started noting a "champion time" for fastest production and analyzing how that was done.

The savings are crucial to paying back about $27 billion in deferred 787 production costs racked up by the first few hundred 787s.

Boeing's goal is to build the largest 787 version, the 787-10, in the same amount of time as the two smaller versions - and for the same cost as the 787-9.

It has no choice but to continue getting lean, Manelski said. "We have to price the airplane more and more aggressively every time we got to the market."

(Reporting by Alwyn Scott)

REUTERS. Jun 7, 2017. Boeing studies 'mild to wild' design for pivotal mid-market jet

By Tim Hepher

CANCUN, Mexico (Reuters) - Boeing (BA.N: Quote) has looked at options "from mild to wild" for the design of a proposed mid-market jet, a senior executive said, hinting at a breakthrough that industry sources say will create building blocks for future models.

Marketing Vice President Randy Tinseth said Boeing would leapfrog reported plans by Airbus (AIR.N: Quote) to update its hot-selling A321neo, as Boeing eyes a gap between narrow-body jets and long-haul aircraft for a potential new mid-market airplane.

"We have looked at the mild and we have looked at the wild and I can tell you we know that if you are going to address that market, you need a new airplane," Tinseth told Reuters after a two-day meeting of airline leaders in Mexico.

Industry sources have said the mid-market development is pivotal for Boeing since it will spawn the industrial jigsaw, systems and cockpits likely to be used for the next plane after that, a three-aircraft replacement of Boeing's 737 cash cow.

Getting the "production system" right now would partially allow Boeing to develop the next jet, which is expected to revolve around a model carrying 180 passengers, as an industrial spin-off of the mid-market one, albeit with major differences.

This would result in significant cost savings and avoid repeating a patchwork of different production architectures.

Two further derivatives could extend that post-737 jet family to 160-210 seats, based on current market forecasts.

Boeing has not yet talked about its plans beyond the mid-market plane, which is expected to enter service by 2025.

Boeing officials declined comment on the long-term options or specific details of the mid-market project, which one leasing company has dubbed "797".

GOODBYE STEAM ENGINE

For the mid-market jet, industry sources have said Boeing is settling on a family of two wide-body aircraft.

These would effectively combine a twin-aisle cabin sitting on top of the reduced belly space of a single-aisle jet.

The aim is to reduce wind resistance or drag and therefore operating costs.

However, it involves a risky gamble that airlines will not need to carry much paid cargo on the routes for which the airplane is designed, delegates at the airlines meeting in Cancun said.

The two mid-market models, designed to carry about 220-260 passengers over 3,500 to 5,000 nautical miles (6,400-9,260 km), will also have a wing resembling the distinctive stiletto design of the 787 Dreamliner but with significant internal differences.

Seen from the front, the outline of traditional metal airplane fuselages is usually closer to a true circle.

That allows pressurised air inside the cabin to push out uniformly in all directions, easing loads and removing the need for heavy strengthening materials.

That well-tested concept is as old as the steam engine.

Carbon composites allow manufacturers to make complex pieces in one shape and are well suited to the more elliptical design that Boeing has in mind for the new mid-market fuselage.

However, composites are more expensive to produce.

Reuters reported last month that the new aircraft could be built using cheaper and faster new production techniques without costly pressurised ovens, or autoclaves.

That technology was used to weave the carbon wings of Russia's new MS-21 jet, which first flew last month.

Airbus this week played down a project called A321neo-plus-plus in response to the Boeing mid-market jet, first reported by Reuters, and said it was always reviewing options.

(Additional reporting by Victoria Bryan; Editing by Susan Fenton)

BLOOMBERG. 2017 M06 8. Boeing’s Rookie Plane Boss Plots Assault on Airbus With New Jets

by Julie Johnsson

- McAllister oversees Max 10 and ‘797’ with billions at stake

- U.S. company looks to hit back at European rival in mid-market

Boeing Co. is about to go on the offensive after watching Airbus SE creep into a market segment the U.S. planemaker had dominated since the 1980s.

Responsibility for the success or failure of the new initiatives falls to a relative newcomer: Kevin McAllister, a 27-year General Electric Co. veteran. On the job a little more than six months, he’s the first outsider to run Boeing’s $65 billion commercial airplanes division.

The multibillion-dollar bets he’s guiding represent Boeing’s response to the sales boom Airbus has enjoyed by inexpensively updating older jet programs. One Boeing project is for an all-new aircraft family to cover the market between the biggest narrow-body planes and smallest wide-bodies. Another is for a larger 737 Max, expected to launch later this month, to take on Airbus’s hot-selling A321neo.

Both members of the global jetliner duopoly also have to contend with aircraft-development programs in Russia and China. That takes McAllister back to the painting in his office depicting the heyday of the steel works in Bethlehem, Pennsylvania, his hometown. The memory of the now-shuttered mills helps provide perspective, he said, that success isn’t guaranteed for the titans of U.S. industry -- not even for Boeing, the country’s largest exporter.

“It’s a reminder that as a company we have to reinvent ourselves every day,” McAllister, who now works out of a Seattle-area office park, said during his first meeting with reporters June 2.

Max 10

The first of the new planes likely to hit the market is the 737 Max 10, which would be the largest version of Boeing’s workhorse single-aisle plane. The company is in discussions with about a dozen potential buyers of the Max 10, which is aimed at curbing the A321’s appeal, said Ihssane Mounir, Boeing’s chief airplane salesman.

Development costs for Boeing will probably be less than $1 billion for the plane, said Richard Aboulafia, an aerospace analyst at Teal Group. The aircraft will be five feet longer than the Max 9, and feature a taller, semi-levered landing gear borrowed largely from Boeing’s 777 wide-body jetliner.

“It’s a relatively minor development program for us to do,” McAllister said. While the Boeing plane is comparable in terms of seating, it’s expected to burn about 5 percent less fuel than the heavier Airbus rival.

As McAllister learns Boeing’s culture and walks the floors of its factories, he and his team are also meeting weekly on a more ambitious project Boeing has long been studying: its first all-new jetliner family since the 787 Dreamliner a decade ago.

It won’t be cheap. Development could cost $10 billion to $15 billion based on past programs, Aboulafia said. And that’s if the process goes smoothly. The Dreamliner’s engineering changes, cost overruns and supplier stumbles saddled the company with nearly $30 billion in deferred production costs.

New Markets

The goal of the new airplane concept -- dubbed the 797 by aircraft-leasing pioneer Steven Udvar-Hazy -- is to generate new travel markets. The twin-aisle, oval-shaped jets would link cities that can’t be efficiently served by current aircraft models on medium-length flights, said Mike Delaney, a Boeing vice president and general manager for airplane development.

The planes would debut in the mid-2020s. They would seat between 220 and 270 passengers. They would fly 4,800 to 5,000 nautical miles, connecting Chinese cities to Southeast Asia, crossing the Atlantic or joining the U.S. to destinations deeper into Latin America.

“We’re going to do exactly in that market what we did with the 787,” Delaney said. “Put in an airplane that’s able to fly about 30 percent more city pairs.”

While the strategy mirrors the more than 140 new routes pioneered by the Dreamliner, Boeing has studied and changed its engineering and development process after the first carbon-fiber jetliner fell years behind schedule.

Boeing is using a processing capability, called the “digital twin,” to design parts and configure the production system around the new aircraft’s architecture, from automation to tooling. Following a process that has been honed with the 737 Max and 777X should lessen engineering error and disruption in the factory, Delaney said.

Airbus Plan

The proposed jets would also replace the Boeing 757 and 767 aircraft that dominated the market spanning the largest narrow-bodies and smallest twin-aisle planes. Airbus has been chipping away at that by adding new engines to the A321 narrow-body and smallest twin-aisle A330neo model.

The European planemaker is looking at expanding the A321neo, chief salesman John Leahy told reporters this week.

“It’s not just the threat itself,” he said in reference to Boeing’s new plane. “We listen to our customers.”

Delaney insists Boeing’s twin-aisle jet would be superior to an even longer Airbus single-aisle plane.

‘Row 65E’

“I certainly wouldn’t want to be in row 65E, waiting to get off,” he said.

Boeing is working with 57 potential customers as it hones designs, range and potential fuel savings, McAllister said. It’s not sufficient to identify a market opportunity. The real challenge lies in developing a business case that will win the approval of Boeing Chief Executive Officer Dennis Muilenburg and company directors.

“We have to bring Dennis and the board a dog that hunts,” he said.

BLOOMBERG. 2017 M06 8. Boeing Woos United and Lion in a Bid to Boost Max 10 Launch

by Julie Johnsson , Anurag Kotoky , and Fabiola Moura

- Chinese lessor CDB also said to study longest version of 737

- Planemaker looks to slow gains of Airbus’s A321neo narrow-body

Boeing Co. is in talks with United Airlines and at least five other companies as the U.S. planemaker tries to line up initial customers for its 737 Max 10 jetliner and gain ground on a fast-selling Airbus SE model, people familiar with the matter said.

The roster of potential buyers of the largest-ever 737, which is expected to launch this month, spans the globe. Initial sales prospects include Indonesia’s Lion Mentari Airlines PT, the aircraft-leasing arm of China’s development bank, Jet Airways India Ltd., SpiceJet Ltd. and Copa Holdings SA, said the people, who asked not to be named because they weren’t authorized to speak publicly about the negotiations.

The U.S. manufacturer is seeking a groundswell of orders to demonstrate the Max 10’s market appeal and strike back at the A321neo, Airbus’s largest narrow-body jet, which is capturing trans-continental routes once dominated by Boeing’s out-of-production 757. The Max 10 talks aren’t final and Airbus could still try to thwart the sales ahead of the Paris Air Show later this month.

A spokesman for Chicago-based Boeing declined to comment on the talks. Megan McCarthy, a spokeswoman for United, declined to comment on a potential order, as did CDB Aviation Lease Finance, the Chinese aircraft lessor, Jet Airways and SpiceJet. Lion and Panama City-based Copa didn’t immediately comment.

‘Better Airplane’

The newest 737 Max would seat about 220 passengers in a single-cabin layout popular with budget carriers while burning about 5 percent less fuel than its similarly sized Airbus rival, according to the U.S. company. The Boeing jet isn’t slated to enter the commercial market until 2020. Airbus delivered the first A321neo earlier this year and has garnered 1,416 total orders, according to the company’s website.

“We aren’t looking to simply build something on par with the A321neo,” said Randy Tinseth, a Boeing vice president for marketing. “We’re bringing a better airplane to the market -- and that’s our focus.”

Airbus sales chief John Leahy dismissed the competitive threat in comments to reporters this week, saying the U.S. planemaker was responding to the A321neo only because the Airbus plane outsold the Max 9 by a four-to-one ratio. The Max 10’s frame would be five feet longer than that of the Max 9. Boeing doesn’t break out its Max sales by variant.

Boeing is “flailing about, trying to come up with some answer to it that doesn’t cost them a fortune,” Leahy said. “Usually those things in aviation don’t work successfully.”

United Fleet

United Continental Holdings Inc. is studying whether to convert 61 orders for the 737 Max to the -10 version, while taking a handful of Boeing 777-300ERs, the largest twin-engine jetliner currently flying, some of the people said. The carrier gained the production slots last year after it converted an earlier order for the Boeing 737-700 to the Max. The Chicago-based airline is also considering an A321neo order, the people said.

Chief Executive Officer Oscar Munoz said United, the third-largest U.S. carrier, was “interested” in the Max 10, during a brief interview on the sidelines of the International Air Transport Association meeting in Cancun, Mexico, this week.

Jet Airways, India’s biggest full-service airline, is preparing to order 50 single-aisle jets, Bloomberg reported June 5. The airline, which operates an all-Boeing narrow-body fleet, is evaluating the Max 10, the high-density Max 200 as well as the Airbus A321neo.

________________

LGCJ.: