CANADA ECONOMICS

IMF

IMF. 05/31/2017. Canada: Staff Concluding Statement of the 2017 Article IV Mission

May 31, 2017

A Concluding Statement describes the preliminary findings of IMF staff at the end of an official staff visit (or ‘mission’), in most cases to a member country. Missions are undertaken as part of regular (usually annual) consultations under Article IV of the IMF's Articles of Agreement, in the context of a request to use IMF resources (borrow from the IMF), as part of discussions of staff monitored programs, or as part of other staff monitoring of economic developments.

The authorities have consented to the publication of this statement. The views expressed in this statement are those of the IMF staff and do not necessarily represent the views of the IMF’s Executive Board. Based on the preliminary findings of this mission, staff will prepare a report that, subject to management approval, will be presented to the IMF Executive Board for discussion and decision.

Context

1. The economy has regained momentum, supported by expansionary fiscal and monetary policies, but complex adjustments are still at play . While personal consumption has been strong, business investment remains weak, non-energy exports have underperformed, and housing market imbalances have risen. Collectively, they raise uncertainty about the durability of the Canadian recovery.

2. Against this background, the 2017 Article IV consultation focused on policies to secure stronger, inclusive, and self-sustaining growth, while preventing the further build-up of housing market imbalances :

- Potential growth forecasts have been gradually marked down since the oil shock. Canada’s traditional engines of growth have slowed, hobbled by longstanding structural problems of low labor productivity growth and population aging that have affected the ability of Canadian firms to compete globally and create jobs. Without bold action to tackle these challenges, Canada’s medium-term growth will struggle to rise above 2 percent.

3. These two challenges will dominate the government’s policy agenda at a time of greater uncertainty about policy outcomes in the U.S. and across the Atlantic . While the global economy has improved with stronger manufacturing activity, the renegotiation of NAFTA, U.S. policies on tax reform and climate change, and the timing and form of the U.K.’s withdrawal from the EU could tilt policies toward protectionism and economic fragmentation. This would have significant consequences for Canada, an economy that is highly reliant on trade and cross border flows.

Outlook and Risks

4. GDP growth strengthened to 1.4 percent in 2016, up from 0.9 percent in 2015, in a volatile year marked by the devastation of the Fort McMurray wildfires. Personal consumption was robust as employment growth accelerated to 1.3 percent, the fastest annual job growth since mid-2013. Energy exports rebounded and the service sector performed well. However, low interest rates have yet to energize business investment, while the depreciation of the Canadian dollar has not provided the expected boost to non-energy exports.

5. The recovery is expected to gain momentum in the near term, supported by a fast-growing U.S. economy, expansionary fiscal and monetary policies, and stable oil prices. GDP growth is projected to rise to 2.5 percent in 2017 and 1.9 percent in 2018, allowing the negative output gap of 1 percent of GDP to close in the first half of 2018.

4. GDP growth strengthened to 1.4 percent in 2016, up from 0.9 percent in 2015, in a volatile year marked by the devastation of the Fort McMurray wildfires. Personal consumption was robust as employment growth accelerated to 1.3 percent, the fastest annual job growth since mid-2013. Energy exports rebounded and the service sector performed well. However, low interest rates have yet to energize business investment, while the depreciation of the Canadian dollar has not provided the expected boost to non-energy exports.

5. The recovery is expected to gain momentum in the near term, supported by a fast-growing U.S. economy, expansionary fiscal and monetary policies, and stable oil prices. GDP growth is projected to rise to 2.5 percent in 2017 and 1.9 percent in 2018, allowing the negative output gap of 1 percent of GDP to close in the first half of 2018.

6. The medium-term outlook is less upbeat, however, because of structural impediments

. As the fiscal stimulus fades and the U.S. economy returns to trend, low labor productivity growth and population aging will limit potential growth to about 1.8 percent, lower than the historical average of 2.6 percent (2000-2008).

7. Risks to the outlook are significant :

- On the domestic side, a sharp correction in the domestic housing market could impair bank balance sheets, trigger negative feedback loops in the economy, and lead to contingent claims on the government. Financial stability risks could emerge if the housing market correction is accompanied by a severe recession.

- On the external side, key risks pertain to higher uncertainty about U.S. policies and its impact on global growth. Stronger-than-expected growth in the U.S., because of planned tax cuts, would provide a fillip to Canadian exports and boost investment in the near term. But if this leads to a faster-than-expected-pace of interest rate hikes in the U.S. and a tightening of global financial conditions ensues, potential abrupt shifts in global market sentiment and a re-pricing of risk could raise the cost of funding for Canadian businesses and households, dampening domestic demand. Beyond this, a move by the U.S. towards greater protectionism, including by imposing non-tariff barriers in a revised NAFTA or raising tariffs, would undercut growth prospects in Canada, leading to a permanent reduction in investment and consumption. Similarly, a sharp reduction in the U.S. corporate tax rate may make Canada less attractive as an investment destination, including for intellectual property, and discourage much needed FDI inflows. Other risks include structurally weaker growth in key advanced and emerging economies and a further decline in oil prices.These risks are interconnected and can be mutually reinforcing. Policy choices will therefore be crucial in shaping the outlook and reducing risks.

Key Messages and Policy Takeaways

Addressing the complex adjustments that are taking place will require policy coordination on several fronts: accommodative fiscal and monetary policy, tight macroprudential policy, and bold action on trade and structural reform. The authorities are rightly factoring in the challenges Canada faces in their policy decision-making.

8. Fiscal policy should be geared toward ensuring that the cyclical recovery is secure, while fostering long-term growth and promoting inclusion.

To this end, the government has introduced tax cuts for the middle class and increased child benefits. In addition, the government has pursued subsidized child care spaces, flexible leave benefits to encourage more women to enter the workforce, and infrastructure spending. The government’s medium-term fiscal trajectory is appropriate given the current economic environment. As the output gap is expected to close in 2018, no further increase in the deficit resulting from discretionary spending or tax cuts will be required. Provincial governments need to be more cautious in their approach as they have a higher debt burden and growing health-care costs; in provinces that are highly indebted, fiscal consolation should continue but at a gradual pace so as not to offset the federal government’s efforts to support the economy.

9. Maintaining fiscal discipline will be important to keep funding costs low and to rebuild buffers.

The government’s commitment to set debt-to-GDP on a declining path is welcome. Once the economy stabilizes around its potential, reinstating a fiscal rule to anchor the medium-term fiscal framework would help ensure the sustainability of public finances.

10. Infrastructure investment is a cornerstone of the government’s growth strategy and the proposed Canada Infrastructure Bank (CIB) will be an effective instrument in achieving this goal.

The CIB is expected to invest in large, complex, and revenue-generating projects, which would not otherwise be feasible, given the risks involved are too large, and returns too small, to attract private investors while the cost is prohibitive for the federal government to go it alone. By taking a subordinate equity stake and leveraging private capital, the CIB would limit government borrowing and reduce pressure on budget financing, and free up fiscal resources for other high priorities. In addition to capital, private investors will be expected to bring their technical competence, discipline, and creativity, that could help reduce risk and lower the overall project cost. The success of the CIB will depend on ensuring that the project selection process is transparent and balances public and private interests. Given the potential of the CIB to advance long-term growth, the government and the CIB must address public resistance to user fees as well as skepticism over involving private investors in public infrastructure projects, with education and a clear statement of the CIB’s benefit.

11. Monetary policy should stay accommodative and gradually tightened as signs of durable growth and inflation pressures emerge.

The Bank of Canada’s cautious approach is justifiable given the considerable uncertainty around the economic outlook. The Bank could aim to achieve a small and temporary overshoot of the inflation target to better manage the downside risks to the inflation outlook and reinforce the symmetry of the inflation target.

12. If downside risks were to materialize, additional fiscal stimulus should be the first line of defense, as Canada has some fiscal space.

Fiscal policy is more potent when there is slack in the economy and monetary policy is constrained by the effective lower bound. To this end, the government should have on stand-by fiscal measures that could be easily brought forward. While further easing of monetary policy could be a useful complement, there is a risk that such action could exacerbate household balance sheet vulnerabilities and housing imbalances. A further cut in the policy rate or recourse to unconventional measures may, however, become necessary if there is a significant contraction in economic activity.

13. Macroprudential policy needs to protect the resilience of the household and banking sector.

Tackling housing market imbalances should be a joint responsibility of both the federal and provincial authorities given the regional divide in housing imbalances. A further tightening of macroprudential and tax-based measures to mitigate speculative and investment activity should be considered. In this regard, greater coordination between federal and provincial regulators, as well as government efforts to collect more comprehensive data on real estate transactions and improve the availability of beneficial ownership information, would improve surveillance and the calibration of these measures. The macroprudential measures would complement safety nets that are already in place to safeguard the financial system, including strengthened supervision, a resilient banking system, full recourse loans, and government-backed mortgage insurance.

14. The property transfer tax introduced by the governments of British Columbia and Ontario targets capital flows and discriminates against non-resident buyers.

However, non-resident activity is not the sole driver of housing prices, as residents also contributed to the spike in prices. The authorities are encouraged to replace the tax with alternative measures that are effective to address systemic financial risk. This could include a combination of prudential and tax-based measures that discourage speculative activity without discriminating between residents and non-residents.

15. The government recognizes that revitalizing productivity is key to placing Canada on a higher and sustainable growth path over the medium term.

Canada has taken a historic step forward in reducing barriers to internal trade, investment, and labor mobility with the new Canadian Free Trade Agreement that will come into effect in July 2017. The government has also unveiled an ambitious “Innovation and Skills Plan” to enhance innovation in “superclusters” that have the greatest potential to accelerate economic growth, and upgrade labor skills through education and training, smart immigration policies, and empowering women in the workplace. These priorities are consistent with Fund and OECD advice. Nevertheless, several caveats are in order:- Policies to promote innovation should be transparent and well targeted, with the aim of creating an “innovation- and competition-friendly” business environment. They should not be used to choose winners and losers.

- A holistic review of the overall tax system would help assess whether there is scope for reducing distortions, minimizing administration and compliance costs, and enhancing equity, while generating sufficient revenues to cover government spending. A more simple and efficient tax system is important to encourage greater participation in the labor market, and promote investment and innovation, so that Canada’s tax competitiveness will be preserved with the rest of the world.

- Shared responsibility for structural reform policies will require coordination across all jurisdictions to reduce overlaps, competing objectives, and inefficiencies that arise from operating too many programs at too small a scale. The federal authorities in partnership with provincial governments, should coordinate policies, establish uniform metrics of success, and institute a transparent and regular reporting mechanism to monitor progress.

- Progress has been slow in improving the regulatory environment and reducing FDI restrictions in the telecommunications, broadcasting, and transportation. Lowering these restrictions is crucial to reduce costs and improve business efficiency, hasten the adoption of new technology, and expand exports of services and high-value, information-intensive products.

16. Diversifying Canada’s export markets will facilitate its integration into global supply chains and reduce its dependence on the U.S. market. The CETA agreement with the EU is a major step forward in establishing new trade relationships. Canada should also tap new sources of growth in Asia, with bilateral trade agreements with China, India and Japan.

STATISTICS AND FINANCE

StatCan. 2017-05-31. Gross domestic product, income and expenditure, first quarter 2017

Real GDP by expenditure

First quarter 2017, 3.7% increase

(quarterly change, annualized)

National saving rate

4.1%, First quarter 2017

Household disposable income

First quarter 2017, 0.4% increase

(quarterly change)

Terms of trade

95.5 (2007=100), First quarter 2017

Debt service ratio

14.17, First quarter 2017

Source(s): CANSIM table 380-0071

Real gross domestic product (GDP) rose 0.9% in the first quarter, following a 0.7% gain in the fourth quarter. Growth was led by final domestic demand (+1.2%) while exports edged down.

Chart 1 Chart 1: Gross domestic product and final domestic demand

Gross domestic product and final domestic demand

Household final consumption expenditure rose 1.1% following a 0.7% gain the previous quarter. Outlays on goods grew 1.5% as purchase of vehicles increased 2.3%. Outlays on services (+0.7%) also rose.

Business gross fixed capital formation rose 2.9% following declines in eight of the previous nine quarters. Growth was driven by housing investment (+3.7%) and investment in machinery and equipment (+5.8%).

Exports edged down 0.1% as services decreased 0.5%. Exports of goods were unchanged.

Imports of goods and services increased 3.3%, in tandem with strength in final domestic demand. This followed a 3.0% decline in imports the previous quarter.

Expressed at an annualized rate, real GDP rose 3.7% in the first quarter. In comparison, real GDP in the United States grew 1.2%.

Chart 2 Chart 2: Contributions to percent change in real gross domestic product, first quarter

Contributions to percent change in real gross domestic product, first quarter

Household consumption increases

Household final consumption expenditures increased 1.1% in the first quarter, following a 0.7% gain in the fourth quarter. Outlays on goods rose 1.5%, with increases in durable (+2.4%), semi-durable (+2.1%) and non-durable (+0.8%) goods. Spending on services rose 0.7%.

Transport (+1.5%) was the largest contributor to increased household spending. Purchase of vehicles rose 2.3%, contributing to higher imports of passenger cars and light trucks (+6.1%). Housing, water, electricity, gas and other fuels (+0.9%), recreation and culture (+1.3%) and clothing and footwear (+2.5%) also increased.

Housing growth accelerates

Business investment in residential structures grew 3.7%, following a 1.5% gain in the fourth quarter. New contruction investment increased 3.9% while ownership transfer costs grew 5.8%, largely due to strong resale activity in the Ontario market. Renovation activity increased 2.1%, a slightly faster pace than in the previous quarter (+1.9%).

Business non-residential investment rebounds

Business investment in machinery and equipment (+5.8%) rebounded following declines in four of the previous five quarters. The increase was concentrated in investment in industrial machinery and equipment (+4.7%), computers and computer peripheral equipment (+7.5%) and medium and heavy trucks, buses and other motor vehicles (+5.8%), which were reflected in rising imports for all of these goods.

Investment in intellectual property products increased 1.5% following two consecutive quarterly declines. Mineral exploration and evaluation (+13.7%) rose sharply following eight consecutive quarters of decline, primarily due to increased activity in oil and gas.

Business investment in non-residential structures increased 0.2% following a 9.3% decline the previous quarter. Engineering structures increased 0.7% after declining 11.6% in the fourth quarter. A large one-time investment in the Hebron offshore oil project in the third quarter of 2016 led to a 9.8% increase in investment in engineering structures in that quarter, followed by a decline in the fourth quarter. Non-residential building investment (-1.5%) continued to decline.

Overall, business gross fixed capital formation increased 2.9% in the first quarter. This was the second quarterly increase in 10 quarters and the largest since the first quarter of 2010.

Chart 3 Chart 3: Business gross fixed capital formation

Business gross fixed capital formation

Inventories build up

Businesses accumulated $12.2 billion in inventories in the first quarter, following a draw-down of $2.8 billion in the previous quarter.

Manufacturing added $6.1 billion to inventories, with stocks of durable goods increasing $5.3 billion and those of non-durable goods rising $811 million. Wholesalers accumulated $3.8 billion. Inventories of motor vehicles increased $2.1 billion. Retailers added $2.3 billion overall to inventories.

Farm inventories fell a further $524 million after a similar draw-down in the previous quarter.

The economy-wide stock-to-sales ratio edged up from 0.749 in the fourth quarter to 0.751 in the first quarter.

Exports edge down

Exports of goods and services edged down 0.1% in the first quarter following a 0.2% gain in the fourth quarter.

Exports of goods were unchanged overall, with increases in motor vehicles and parts (+3.8%) and farm, fishing and intermediate food products (+7.0%) offsetting declines in aircraft and other transportation equipment and parts (-11.7%) and metal ores and non-metallic minerals (-8.5%).

Exports of services were down 0.5%, mostly due to a 1.1% decline in commercial services. Higher exports of travel services (+0.9%) partially offset the decline.

Imports of goods and services rebounded with a 3.3% increase in the first quarter, offsetting a 3.0% decline in the fourth quarter. Increased imports of goods (+3.7%) offset a 3.7% decline in the fourth quarter. The import of the Hebron oil platform in the third quarter led to 1.2% growth in that quarter and the subsequent decline in the fourth. Imports of services rose 1.3% in the first quarter.

Household saving decreases

Compensation of employees grew 0.9% in the first quarter (nominal terms), after increasing 1.2% the previous quarter. Wages and salaries rose 1.0%, with increases in both goods (+1.4%) and services (+0.9%) producing industries.

Household final consumption expenditure (nominal terms) rose 1.4%, outpacing household disposable income (+0.4%). The household saving rate decreased to 4.3% in the first quarter.

The household debt service ratio (defined as household mortgage and non-mortgage payments divided by disposable income) increased from 14.13% in the fourth quarter to 14.17% in the first quarter as debt payments increased at a faster pace than disposable income.

Corporate earnings increase

The gross operating surplus of non-financial corporations grew 5.6% in the first quarter, following a 4.1% increase the previous quarter. Strong domestic demand contributed to gains in non-financial corporate earnings. The gross operating surplus of financial corporations grew 1.4%.

Real gross national income increased 1.3% as the terms of trade improved for a fourth consecutive quarter. Export prices increased 1.5% as energy prices rose, while import prices fell 0.6%.

Government fiscal positions improve

The net borrowing position of the overall government sector was reduced to $34.3 billion, following increases over the previous two quarters, as government revenues (+1.1%) grew at a faster pace than expenditures (+0.5%). Improvements in government fiscal positions were evidenced at both the federal and provincial levels.

FULL DOCUMENT: http://www.statcan.gc.ca/daily-quotidien/170531/dq170531a-eng.pdf

StatCan. 2017-05-31. Gross domestic product by industry, March 2017

Real GDP by industry

March 2017, 0.5% increase

(monthly change)

Source(s): CANSIM table 379-0031

Real gross domestic product (GDP) increased 0.5% in March, following no change in February. Growth was widespread across goods-producing and service-producing industries.

Chart 1 Chart 1: Real gross domestic product increases in March

Real gross domestic product increases in March

Goods-producing industries grew for the fourth time in five months, increasing 0.9% in March, while service-producing industries rose 0.3% in March and have grown continuously since September 2015.

Manufacturing leads the growth

The manufacturing sector was the largest contributor to the growth in GDP in March, growing 1.6% and more than offsetting a 1.0% contraction in February.

Non-durable manufacturing (+1.7%) rose for the fourth time in the last five months based on widespread growth. With the exception of paper manufacturing, all subsectors posted gains, led by chemical products (+2.4%), petroleum and coal products (+2.6%) and plastic and rubber products (+2.4%). Food manufacturing rose 0.9% as seven of nine industry groups registered growth.

Durable manufacturing rose 1.5% in March as the majority of subsectors were up. Leading the growth in durable manufacturing were machinery manufacturing (+3.9%) and computer and electronic products (+4.8%). Transportation equipment increased 0.9%, reflecting growth in motor vehicle, motor vehicle body and trailer, motor vehicle parts and aerospace product and parts manufacturing. Miscellaneous transportation equipment manufacturing contracted 4.5%. Other subsectors posting declines were manufacturers of furniture (-2.8%) and non-metallic minerals (-2.4%).

Chart 2 Chart 2: Manufacturing output grows in March

Manufacturing output grows in March

Retail trade and wholesale trade continue to grow

Retail trade grew for the eighth time in nine months, rising 1.0% in March. Eight of twelve subsectors registered higher activity. Leading the growth were motor vehicle and parts dealers (+4.2%), primarily on the strength of more activity at new car dealers, and general merchandise stores (+2.6%).

Wholesale trade increased for the sixth month in a row, up 0.7% in March from widespread growth across subsectors. With the exception of machinery, equipment and supplies wholesalers, which contracted 1.9%, all other subsectors rose or were unchanged in March. Leading the growth was a 2.9% increase at building material and supplies wholesalers, reflecting the growth in lumber, millwork, hardware and other building supplies wholesaling as well as metal service centres.

Construction up for a fifth consecutive month

Construction increased for a fifth consecutive month, gaining 0.8% in March. Residential construction was up 1.2% in part due to increases in single, double and row housing construction, as well as in alterations and improvements. Engineering and other construction activities (+1.0%) and repair construction (+0.2%) also rose.

Non-residential construction contracted for the sixth month in a row, edging down 0.1% as institutional and governmental construction and industrial construction both declined.

Finance and insurance sector continues to grow

Finance and insurance rose 0.8% in March, growing for the sixth time in seven months. Depository credit intermediation and monetary authorities were up 1.3%. Financial investment services, funds and other financial vehicles grew 0.4% on the strength of increased market activity while insurance services and related activities remained unchanged.

Real estate and rental and leasing sector up

The output of the real estate and rental and leasing sector increased 0.3% in March. Activity by real estate agents and brokers grew 2.5% on the strength of continued higher home resale activity in Ontario and British Columbia.

Mining, quarrying, and oil and gas extraction grows

Mining, quarrying, and oil and gas extraction rose 0.3% in March following a 0.3% decline in February.

Support activities for mining and oil and gas extraction grew for the eighth month in a row, up 9.9% in March, after declining for most of 2015 and the first half of 2016. There were increases in drilling and rigging services, as well as in support activities for mining and quarrying.

Oil and gas extraction declined 0.4% in March. Growth in conventional oil and gas extraction (+2.0%) was more than offset by a decline in non-conventional oil extraction (-3.1%), as a fire and explosion at an oil upgrader facility in the Fort McMurray area disrupted production.

After decreasing 3.5% in February, mining and quarrying excluding oil and gas extraction further declined 2.1% in March. The largest contributor to the decline was a 7.2% contraction in non-metallic mineral mining, as potash mining declined for a third consecutive month due in part to lower exports. Metal ore mining edged down 0.1% in March as an increase in iron ore extraction was offset by declines in other types of metal ore mining. Coal mining grew 4.5% in March after three months of declines in part due to higher exports to Asia.

Utilities up from higher demand for heating

Utilities rose 1.6% in March after edging down 0.1% in February. Electric power generation, transmission and distribution rose 1.4% in March, while natural gas distribution was up 4.1% as unusually low temperatures across the country increased the demand for heating.

Transportation and warehousing grows

Transportation and warehousing services rose 0.3% in March, led by growth in air transportation (+1.4%) as movement of both passengers and goods increased. Pipeline transportation was up 1.1% as the transportation of natural gas (+2.0%) and crude oil (+0.3%) grew in part because of higher exports. Growth was partly offset by a 1.4% decline in postal and courier services, as postal as well as courier and messenger services declined.

Other industries

The public sector (education, health care and public administration) edged up 0.1% in March as education and healthcare rose, while public administration remained essentially unchanged.

Arts, entertainment and recreation services were up 0.6% in March. The 2.2% growth in performing arts, spectator sports and heritage institutions was partly offset by a 0.6% decline in amusement, gambling and recreation industries.

Accommodation and food services edged down 0.1% in March as growth in accommodation services was more than offset by a decline at food services and drinking places.

Agriculture, forestry, fishing and hunting was down for the fifth time in six months, declining 0.4% in March.

Chart 3 Chart 3: Main industrial sectors' contribution to the percent change in gross domestic product in March

Main industrial sectors' contribution to the percent change in gross domestic product in March

First quarter of 2017

The value added of goods-producing industries rose 1.7% in the first quarter of 2017, marking three consecutive quarters of growth. The value added of service-producing industries increased 0.9%. Growth in both goods-producing and service-producing industries was widespread, as all sectors recorded gains, with the exception of agriculture, forestry, fishing and hunting and management of companies and enterprises.

The main contributor to growth in goods-producing industries was a 2.6% rise in mining, quarrying, and oil and gas extraction. This increase is attributable in large part to support activities for mining and oil and gas extraction, which grew 30%, following a 23% increase in the previous quarter, reversing a downward trend that started in mid-2014.

Manufacturing was up 1.8%. Gains were shared across durable (+1.9%) and non-durable (+1.7%) manufacturing, as most subsectors showed growth.

Construction grew 1.7% in the first quarter, led by an increase in residential construction (+3.0%), the largest gain since the first quarter of 2012. Non-residential construction was down for the sixth consecutive quarter.

The largest contributor to growth in service-producing industries in the first quarter was wholesale trade, which grew 3.0%, its highest level of growth since the fourth quarter of 2010. This was partly a result of increased activity by machinery, equipment, and supplies wholesalers (+5.4%) and motor vehicle and parts wholesalers (+7.3%).

Real estate and rental and leasing rose 0.8% as activity by real estate agents and brokers was up 2.2%. Retail trade (+1.9%) grew for a third consecutive quarter, with increases in 10 of 12 subsectors. Finance and insurance (+1.4%) increased for the seventh quarter in a row. The public sector (education, health and public administration) grew 0.3%.

FULL DOCUMENT: http://www.statcan.gc.ca/daily-quotidien/170531/dq170531b-eng.pdf

Department of Finance Canada. May 31, 2017. International Monetary Fund Report Praises Canada's Approach of Investing in the Middle Class and the Economy

Ottawa, Ontario – The Government of Canada has an ambitious plan to make smart investments that will create jobs, build modern, resilient neighbourhoods and communities, grow our economy, and provide more opportunities for the middle class and those working hard to join it.

Finance Minister Bill Morneau today welcomed the Concluding Statement of the International Monetary Fund's (IMF) annual Article IV Mission to Canada, which supports the Government's inclusive growth policies.

The IMF supports the Government's approach of making smart, responsible investments in people, communities and the economy to create long-term growth that is shared by the middle class and those working hard to join it.

Today's IMF report notes that the Canadian economy's renewed momentum is supported by these investments, and that the proposed Canada Infrastructure Bank has the potential to be an important and effective instrument to support infrastructure investment and stronger, long-term growth.

Quote

"The Government of Canada is committed to building a strong middle class and growing the economy over the long term. It is clear that our approach is working. In the past year, more than a quarter million people have been hired and the unemployment rate has fallen 0.6 percentage points to its lowest point since the 2008 global financial crisis. This morning, data shows that economic growth in the first quarter was robust, which is boosting middle class confidence. I am proud of the international recognition that our approach is receiving, and would like to thank the IMF for their analysis today. I look forward to continuing our good work together in promoting inclusive growth, both in Canada and around the world."

- Bill Morneau, Minister of Finance

The Globe and Mail. Reuters. May 31, 2017. Canada’s economy accelerates; nudges BoC closer to hiking rates

LEAH SCHNURROTTAWA — Canada’s economy accelerated in the first quarter on the back of strong consumer spending and a business investment rebound, bolstering the case for the central bank to begin considering raising interest rates.

Gross domestic product grew at an annualized 3.7 per cent pace, Statistics Canada said on Wednesday, slightly below expectations for 3.9 per cent growth and following upwardly revised annualized growth of 2.7 per cent in the fourth quarter.

The economy was also on solid footing as it ended the first quarter, with growth rising by a better-than-expected 0.5 per cent in March.

While the first-quarter expansion was shy of the Bank of Canada’s 3.8 per cent forecast, it made Canada a growth leader among its industrialized peers at the start of the year.

“At the end of the day, we have to call it strong no matter what,” said Derek Holt, an economist at Scotiabank. “A lot of other countries would like to be in this position.”

Economists said the strong data put the Bank of Canada one step closer to raising rates. The central bank is largely expected to be on hold until 2018.

“If we continue to get growth numbers like this, absent trade policy risks, it’s going to be tougher for the Bank of Canada to avoid rate hikes at some point in the distance,” Holt said.

After initially strengthening following the data, the Canadian dollar was weaker against the greenback as oil prices fell.

Business investment picked up after declining in four of the past five quarters, with companies spending more on industrial machinery and equipment, and computers.

While the Bank of Canada will be encouraged by the long-awaited improvement in investment, the protectionist tone out of the United States will act as a counterbalance, said Paul Ferley, the assistant chief economist at Royal Bank of Canada.

Growth was also supported by a rebuilding of business inventories, which economists said could be reversed in the coming quarters. A rebound in imports weighed on growth, while exports fell modestly due to a decrease in services sent abroad.

Consumers continued to spend, particularly on vehicles. While wages rose 1 per cent compared to the previous quarter, the savings rate fell to 4.3 per cent.

Investment in residential structures also lifted the economy, bolstered by increased new home construction and a rise in the costs of selling a home amid strong resale activity in Ontario, the country’s most populous province.

REUTERS. May 31, 2017. Canadian dollar dips as slumping oil prices offset strong GDP data

By Fergal Smith

TORONTO (Reuters) - The Canadian dollar weakened against its U.S. counterpart on Wednesday as a drop in oil prices offset data showing strength in the domestic economy.

Canada's gross domestic product grew at an annualized 3.7 percent pace, slightly below economists' expectations for 3.9 percent, though growth in both the third and fourth quarters of 2016 was revised upward.

The economy also appeared to have solid momentum heading into the second quarter with growth rising by a better-than-expected 0.5 percent in March.

"If we continue to get growth numbers like this ... it's going to be tougher for the Bank of Canada to avoid rate hikes at some point in the distance," said Derek Holt, head of capital markets economics at Scotiabank.

The central bank last week struck a more upbeat tone than investors had expected as it kept interest rates on hold at 0.5 percent.

Chances of a Bank of Canada rate hike this year have increased to 30 percent from roughly one-in-ten before the interest rate decision, data from the overnight index swaps market showed.

Prices of oil, one of Canada's major exports, fell on Wednesday to a three-week low on news that Libyan output was recovering from an oilfield technical issue, fuelling concerns that Organization of the Petroleum Exporting Countries-led output cuts were being undermined by producers outside the deal.

U.S. crude CLc1 prices were down 2.52 percent at $48.41 a barrel.

At 9:21 a.m. ET (1321 GMT), the Canadian dollar CAD=D4 was trading at C$1.3477 to the greenback, or 74.20 U.S. cents, down 0.1 percent.

The currency traded in a range of C$1.3438 to C$1.3479 after having hit on Tuesday its weakest in nearly one week at C$1.3506.

Canadian government bond prices were mixed across a slightly steeper yield curve. The two-year CA2YT=RR was flat to yield 0.70 percent and the 10-year CA10YT=RR declined 6 Canadian cents to yield 1.421 percent.

On Monday, the 10-year yield hit its lowest intraday level in six months at 1.399 percent.

Canada's trade data for April is due on Friday.

(Additional reporting by Alastair Sharp; Editing by Meredith Mazzilli)

________________

HOUSING BUBBLE

The Globe and Mail. May 31, 2017. IMF warns of ‘significant’ risks from Canada’s housing market

BILL CURRY

OTTAWA — The International Monetary Fund is urging Canada to take further action in order to address rising household debt levels and the risks of a sharp correction in the housing market.

In a staff statement that followed an annual visit to Canada, the IMF warns of “significant” risks to future growth due to the potential for a housing market decline that impairs bank balance sheets and spreads to the broader economy.

“Credit ratings of Canada’s six largest banks were lowered recently, reflecting concern that high household debt and the rapid appreciation of house prices could weaken asset quality in the future,” the IMF stated.

As a result, Cheng Hoon Lim, an assistant director of the IMF, told a news conference in Ottawa that several specific actions are needed. She called for policies that will further tighten restrictions on speculative investments in the housing sector, greater co-ordination between federal and provincial regulators and better data on real estate transactions, which she noted has been promised by Ottawa.

Ms. Lim’s staff statement also took issue with the foreign buyers tax approach introduced in British Columbia and Ontario that “discriminates against non-resident buyers.” The IMF states that non-resident activity is not the sole driver of housing prices and the provinces should replace the foreign-buyers taxes with more effective tax changes aimed at discouraging speculative activity.

Federal Conservative and Liberal governments have announced several rounds of policy changes since 2008 that are aimed at discouraging home buyers from taking on more debt than they can handle. The most recent round of federal changes were announced in October. British Columbia and Ontario have also announced tightening measures that fall under provincial jurisdiction.

The IMF noted that high debt levels and housing affordability challenges are primarily a concern in Toronto and Vancouver, where many first-time buyers have been priced out of the market. Ms. Lim said the IMF has been studying the effectiveness of all of these policy measures.

“Overall, they have been effective in dampening mortgage credit growth, but less so with respect to house prices. There is an effect, but not as strong,” she said. “What we have found, it’s still a bit too early to tell because these measures were introduced in late 2016, but the measure to make it harder to qualify to qualify for mortgages by having a more stringent stress test on interest rates I think is beginning to work.”

The IMF statement touched on a wide-range of issues, including fiscal and monetary policy, infrastructure spending and projections for economic growth.

The IMF projects the Canadian economy will grow by 2.5 per cent in 2017 and 1.9 per cent in 2018. However the medium-term outlook is described as “less upbeat,” as low labour productivity and population aging is expected to limit potential growth to about 1.8 per cent. That’s lower than the historical average of 2.6 per cent growth between 2000 and 2008.

On monetary policy, the IMF said the Bank of Canada’s cautious approach is “justifiable” given the considerable uncertainty in the economic outlook. On the fiscal side, the IMF also approved of Ottawa’s deficit spending and welcomed the pledge to set federal debt-to-GDP on a declining path.

On the issue of the Infrastructure Bank, which is currently a matter of heated debate in the House of Commons as the government moves to pass enacting legislation, the IMF praised the overall concept as an “effective” instrument.

“The success of the CIB will depend on ensuring that the project selection process is transparent and balances public and private interests. Given the potential of the CIB to advance long-term growth, the government and the CIB must address public resistance to user fees as well as skepticism over involving private investors in public infrastructure projects, with education and a clear statement of the CIB’s benefit,” the IMF states.

REUTERS. May 31, 2017. Housing, U.S. protectionism key risks to Canada outlook - IMF

OTTAWA (Reuters) - The Bank of Canada should keep interest rates low and Canada's federal government should be ready with more fiscal stimulus in the event of an economic downturn, the International Monetary Fund said on Wednesday in a report that reiterated warnings about Canada's hot housing market and high household debt.

In an annual assessment of Canada's economy, the IMF said while it expects the recovery to gain momentum in the near term, risks to the outlook are significant - including a sharp correction in housing and U.S. protectionism.

The IMF staff said the Bank of Canada's cautious approach is justifiable given the "considerable uncertainty" around the economic outlook, and said monetary policy should stay accommodative and gradually tighten as signs of durable growth and inflationary pressures emerge.

"The Bank could aim to achieve a small and temporary overshoot of the inflation target to better manage the downside risks to the inflation outlook and reinforce the symmetry of the inflation target," the report said.

The central bank has held rates steady at 0.5 percent since 2015 in a bid to boost growth in the wake of an oil price slump.

The IMF warned a sharp correction in housing could hurt the nation's banks, which have already been downgraded, trigger negative feedback loops in the economy, and lead to contingent claims on the government.

"Financial stability risks could emerge if the housing market correction is accompanied by a severe recession," the report warned.

House prices in Toronto and Vancouver, the nation's largest markets, have more than doubled since 2009 but signs of a slowdown have emerged in the wake of repeated government moves to tighten mortgage lending and the introduction of a foreign buyers tax in those two cities.

Still, the IMF said a further tightening of macroprudential and tax-based measures should be considered to mitigate speculative and investment activity.

It said the foreign buyers tax is discriminatory and urged authorities to replace it with rules or taxes aimed at discouraging speculation without targeting non-residents.

While growth is seen rising to 2.5 percent this year as oil prices stabilize and U.S. growth boosts Canada's economy, GDP growth is expected to slip to 1.9 percent next year as stimulus fades and U.S. growth moderates.

The IMF said fiscal stimulus should be the first line of defense if downside risks materialize, because there is a risk further easing of monetary policy could worsen household debt and housing imbalances.

(Reporting by Andrea Hopkins; Editing by Andrea Ricci)

The Globe and Mail. May 30, 2017. Efforts to cool housing market sparked drop in CMHC insurance

JANET MCFARLAND

New mortgage insurance rules introduced by the federal government last fall to cool the housing market have led to a sharp drop in insurance volumes for Canada Mortgage and Housing Corp. as fewer home buyers qualify for mortgage insurance.

CMHC said total insured volumes fell 41 per cent in the first quarter of 2017, including a 23-per-cent drop in homeowner insurance volumes and an 87-per-cent decline in the volume of portfolio insurance, which is bulk insurance purchased by financial institutions for their portfolios of uninsured mortgages.

The numbers unveiled on Tuesday offer a window into the impact of the government’s new rules, suggesting they have led to a significant decline in the number of people qualifying for insured mortgages under the tougher standards. Among the changes announced in October, the federal government increased “stress testing” standards for people taking out fixed-rate loans of five years or more to ensure they could still afford their mortgages at higher interest rates than they are currently paying.

CMHC said it insured 48,746 housing units in the first quarter, down 41 per cent from 82,834 units in the same period last year. Homeowners insured 18,624 units with CMHC in the quarter, a 23-per-cent drop from 24,162 units last year, while institutions bought portfolio insurance for just 4,662 units, down 87 per cent from 36,690 units last year, after CMHC hiked premiums on that insurance category.

The declines were somewhat offset by increases in insurance volumes for multiunit residential buildings, such as apartment buildings, where the number of units insured rose by 16 per cent to 25,460 from 21,982 last year.

The total value of new loans insured in the first quarter dropped 42 per cent to $8.3-billion from $14.3-billion last year, CMHC said. The Crown corporation’s total portfolio of insurance-in-force stood at $502-billion as of March 31, down 2 per cent from $512-billion at the end of December, 2016.

Portfolio insurance for financial institutions, which took the biggest hit in the first quarter, was affected by new federal rules last fall that restricted the types of mortgages eligible to be insured. Lenders can no longer insure mortgages on homes with a purchase price of more than $1-million, for example, and cannot insure mortgages on homes that are purchased for rental or as investments.

Steven Mennill, CMHC’s senior vice-president of insurance, said most of the drop in demand for portfolio insurance in the first quarter was the result of a premium hike CMHC introduced on Jan. 1 because of new capital requirements for mortgage insurers that were introduced by Canada’s financial regulator.

Mr. Mennill said CMHC doesn’t know yet whether the drop in portfolio insurance signals a permanent shift in its business model or whether demand for the insurance product will swing back again.

“It’s not clear at this point whether either of these changes will be sustained over the long term,” he said. “Portfolio insurance [demand] is largely a function of the overall sources of capital and liquidity and funding available to lenders in the system, which is affected by a wide range of factors. The cost of portfolio insurance is just one of them.”

The declining insurance volumes led to an 8.1-per-cent drop in premiums and fees earned by CMHC on new mortgage insurance written in the first quarter, but the agency posted a 2.4-per-cent increase in premiums and fees earned on its entire insurance portfolio.

CMHC reported that its total revenue soared in the first quarter to $2.25-billion from $1.2-billion last year, while profit climbed to $370-million from $313-million.

Most of the increase in revenue is a result of the federal government’s rapid expansion to assisted housing programs under the National Housing Strategy, which is aimed at expanding affordable and assisted housing programs in communities across the country. The Trudeau government announced new federal investments of $11.2-billion over 11 years in its 2017 budget on top of other spending under the strategy.

CMHC is delivering much of the spending under the program, but the money is passing through the agency and is not revenue it is earning from business activity. CMHC chief financial officer Wojo Zielonka said the organization still anticipates that mortgage insurance will account for a majority of its business going forward.

CMHC has historically kept all the income it has earned as capital for its operations, but will start paying a dividend this year, reporting Tuesday that it will transfer $145-million to the federal government. Mr. Zielonka said CMHC also expects to declare a further one-time special dividend this year of excess capital.

________________

BOMBARDIER

The Globe and Mail. REUTERS. May 31, 2017. The Canadian PressOttawa says Boeing an ally but Bombardier petition disappointing

MIKE BLANCHFIELD

OTTAWA — Canada’s defense minister, Harjit Sajjan, said on Wednesday that Boeing Co will be a trusted military ally in decades to come, but that its anti-dumping petition against Bombardier Inc is not behaviour expected of a partner.

Sajjan called on Boeing to abandon the anti-dumping challenge it has launched against Canadian plane maker Bombardier, saying Ottawa was disappointed by the U.S. company’s behaviour. Canada has threatened to scrap plans to buy Boeing fighter jets over the dispute.

“We have a longstanding relationship with Boeing, and as I stated, we’re hoping that this can be resolved in a ... manner that respects everyone,” Sajjan told reporters on the sidelines of a defense industry event in Ottawa.

Earlier this month, in response to Boeing’s challenge at the U.S. International Trade Commission, Canada said it was reviewing the planned purchase of 18 Boeing Super Hornet jets.

Boeing accuses Bombardier of selling airliners in the U.S. market at artificially low prices.

When asked whether Ottawa would scrap the order if Boeing failed to drop its complaint, Sajjan said “we need to let the process take its course.” The Super Hornets are needed as an interim measure until Ottawa can run a competition to replace its aging fleet of CF-18 fighters.

“The interim fleet procurement requires a trusted industry partner. For decades, Boeing has been an outstanding partner with the Canadian Armed Forces ... I expect that to be the case in the decades to come,” he said during a speech.

“However, our government is of the view that their action against Bombardier is unfounded. It is not the behaviour we expect of a trusted partner, and we call on Boeing to withdraw it.”

________________

ENERGY

The Globe and Mail. Reuters. May 31, 2017. Oil at three-week low on potential undermining of OPEC-led deal

KAROLIN SCHAPS

LONDON — Oil prices fell to a three-week low on Wednesday on news that Libyan output was recovering from an oilfield technical issue, fueling concerns that OPEC-led output cuts to reduce global inventories were being undermined by producers outside the deal.

Benchmark Brent oil was down $1.63, or 3.1 per cent, at $50.21 a barrel by 1341 GMT, after earlier touching $50.12 a barrel, the weakest since May 10. U.S. light crude traded at $48.31, down $1.35, or 2.7 per cent.

Both contracts were on track for their third straight monthly loss.

“Unless some bullish news stops this, prices will fall further in particular now with Brent trading below the post-OPEC low and approaching $50 a barrel,” said Carsten Fritsch, commodity analyst at Commerzbank.

The Organization of the Petroleum Exporting Countries and other producers, including Russia, agreed last week to extend a deal to cut production by about 1.8 million barrels per day (bpd) until the end of March 2018.

“Traders covered short positions ahead of OPEC and some of these have now been re-established,” said Ole Hansen, head of commodities strategy at Saxo Bank.

OPEC members Libya and Nigeria are exempt from the cuts, while U.S. shale oil producers are not part of the agreement and have been ramping up production.

Libya’s oil production has risen to 827,000 bpd, climbing above a three-year peak of 800,000 bpd reached earlier in May, the National Oil Corporation said, after a technical issue that hit Sharara oilfield was resolved.

Shipping data on Thomson Reuters Eikon shows that, excluding pipeline exports, Libya shipped an average of 500,000 bpd of oil so far this year, compared with 300,000 bpd average for 2016.

Official government data showing weekly U.S. crude inventories will be published on Thursday. Analysts polled by Reuters expected U.S. stocks to have fallen by 2.8 million barrels last week, their eighth straight weekly decline.

“Attention will be on U.S. inventory stocks tomorrow, with expectations of a further draw this week, following initial indications of strong demand for gasoline after the AAA said that driving mileage over the holiday weekend was the highest since 2005,” said analysts at Cenkos Securities.

Compliance by those signed up to the OPEC-led deal remained high among OPEC members and industry sources said Russian figures for May showed output in line with its pledge.

Saudi Arabia and Russia said on Wednesday that cooperation between OPEC and non-OPEC producers was seen lasting beyond March. “We want to institutionalize cooperation between OPEC and non-OPEC producers,” Saudi Energy Minister Khalid al-Falih said.

BLOOMBERG. 2017 M05 31. Canada Bids Farewell to Oil Shock With Its Economy on a Tear

by Theophilos Argitis and Erik Hertzberg

- Quarterly gain is one of the most broad-based since recession

- Trade disappointment means growth comes in below forecast

If it wasn’t clear after the six-month run of strong economic data, the latest GDP numbers out of Canada confirm the country has bid adieu to its oil crisis.

The economy accelerated to a 3.7 percent annualized pace in the first quarter, following gross-domestic-product gains of 2.7 percent and 4.2 percent in the prior two periods, Statistics Canada reported Wednesday from Ottawa. That’s the strongest three-quarter gain since 2010.

It had been a tough ride, as the nation suffered through a once-in-a-generation collapse in commodity prices and one of its worst-ever economic performances short of a recession. Even now, the markets’ lackluster response to the news Wednesday -- the Canadian dollar fell -- underscore worries the country will struggle to find a new catalyst, especially once interest rates begin to rise from historical lows.

“Canada’s economy is humming along at a solid pace, and that has to be the lead for any story on the Q1 GDP numbers,” Avery Shenfeld, chief economist at Canadian Imperial Bank of Commerce, said in a note to investors. “Growth has left the earlier oil-price shock in the rear view mirror.”

Canada’s dollar, the worst performing major currency this year, fell 0.3 percent at 12:41 p.m. Toronto time Wednesday. Economists expected even stronger growth, with the median forecast in a Bloomberg survey coming in at 4.2 percent.

A report from the International Monetary Fund Wednesday highlighted the challenges, which have also kept the Bank of Canada on the sidelines even as the Federal Reserve has been raising interest rates.

The IMF estimates growth is on track to average 1.8 percent over the medium term. The Bank of Canada has also warned about Canada’s long-term potential growth, even as stronger growth this year cuts into excess capacity and diminishes the need for lower rates.

Economists forecast the Bank of Canada will start raising rates sometime next year.

Key Points

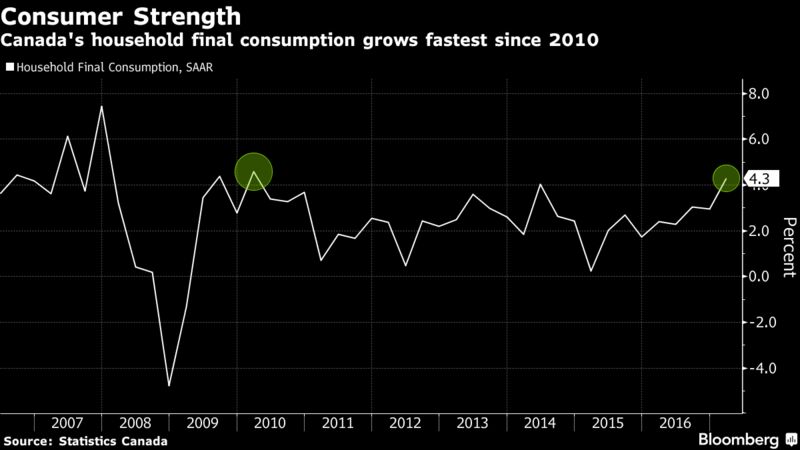

- Canada’s indefatigable consumers, benefiting from a buoyant jobs market and rising home values, continue to be key drivers. Household final consumption expenditure rose at an annualized 4.3 percent annualized pace in the first quarter. That’s the fastest since 2010.

- The housing booms in Toronto and Vancouver are fueling residential investment, which was up 15.7 percent on an annualized basis in the first quarter. That’s the biggest gain since the first quarter of 2012.

- Business investment made a comeback in the first quarter. Investment in non-residential structures, along with machinery and equipment, posted only its second quarterly gain since 2014, growing an annualized 10.3 percent. The increase was the largest since 2012.

- All major components of domestic demand increased in the first quarter -- the first time that’s happened since 2010.

- During the month of March, Canada’s economy grew at a more-than-expected 0.5 percent pace on the back of higher manufacturing, more than double the 0.2 percent pace estimated by economists.

Questions Remain

- There was a big jump in inventories, which turned out to be the biggest contributor to growth -- worth 3.6 percentage points. That may not bode well for the future if businesses decide to pare down those inventories

- The pick-up in consumption is being financed by a reduction in the household savings rate, which fell to 4.3 percent in the first quarter, a two-year low.

- Residential investment may have hit its high water mark as tougher regulations and new taxes kick in. At 7.1 percent of GDP, residential investment is the highest since 2006 and nearing its late 1980s record of about 8 percent.

- Exports disappointed, with a negative annualized reading of 0.3 percent in the first quarter. Combined with a surge of 13.7 percent in imports, the trade sector was a major drag on growth. That means the expansion is totally reliant on domestic demand -- business, consumer and government spending -- which was up an annualized 4.7 percent in the first quarter.

________________

LGCJ.: