CANADA ECONOMICS

INVESTIMENT

StatCan. 2017-06-13. Canada's international investment position, first quarter 2017

Canada's net international investment position

$247.9 billion, First quarter 2017

Source(s): CANSIM table 376-0142.

Canada's net foreign asset position rose by $75.6 billion in the first quarter to $247.9 billion. The increase in the net asset position reflected the stronger performance of foreign stock markets relative to the Canadian stock market, which pushed the value of Canada's international assets up by more than liabilities. Over the quarter, the US stock market (as measured by the Standard and Poor's 500) rose 5.6% while the Canadian stock market (as measured by the Standard and Poor's / Toronto Stock Exchange composite index) increased 1.7%.

Chart 1 Chart 1: Canada's net international investment position

Canada's net international investment position

On a geographical basis, Canada continued to post a net foreign asset position with non-US countries as a whole and a net foreign debt position with the United States. The net foreign debt position with the United States was reduced from $116.4 billion to $89.0 billion at the end of the first quarter. Canada's financial assets held in the United States rose by $85.4 billion, while Canada's international liabilities with the United States increased by $58.0 billion in the first quarter. Historically, Canada's net international investment position with the United States has been negative, with the exception of the fourth quarter of 2015.

Chart 2 Chart 2: Net international investment position by geographic region

Net international investment position by geographic region

Large cross-border transactions and higher foreign stock prices push Canada's international assets up

Total international assets were up by $141.1 billion to $4,438.2 billion at the end of the first quarter. The increase was mainly attributable to the strong performance of foreign stock markets and significant cross-border investments in equity instruments.

Canadian investors increased their holdings of foreign equity instruments by $165.4 billion to $3,092.2 billion in the first quarter, led by record cross-border acquisitions and higher equity prices. Meanwhile, Canadian holdings of foreign debt instruments were down by $24.3 billion to $1,346.0 billion. This mainly reflected a $32.7 billion decline in currency and deposits held by Canadians abroad, moderated by an increase in loan assets.

The growth in international assets was moderated by the overall downward revaluation effect related to the fluctuations of the Canadian dollar against foreign currencies. Over the quarter, the Canadian dollar gained 1.0% against the US dollar but lost 0.1% against the euro, 0.6% against the British pound and 3.8% against the Japanese yen. Since most of Canada's international assets are denominated in US dollars, the downward effect of the appreciating Canadian dollar against the US dollar more than offset the upward effect resulting from its depreciation against other foreign currencies.

Chart 3 Chart 3: International assets and liabilities

International assets and liabilities

Canada's international liabilities up on strong foreign investment in Canadian securities

Canada's international liabilities rose by $65.5 billion to $4,190.3 billion in the first quarter. Strong foreign portfolio investment in Canadian securities largely contributed to this increase.

Foreign holdings of Canadian equity instruments rose by $53.2 billion to $1,820.3 billion in the first quarter. Large foreign acquisitions of portfolio equity securities and, to a lesser extent, the revaluation effect of higher Canadian equity prices contributed to the increase in the quarter.

Canadian debt instruments held by foreign investors, also referred to as Canada's gross external debt, grew by $12.3 billion to $2,370.0 billion at the end of the quarter. The increase was mainly driven by higher foreign holdings of Canadian bonds, but moderated by declines in money market instruments and deposits held by non-residents in Canada. On a sector basis, Canadian government debt held by foreign investors totalled $443.1 billion and represented 19% of Canada's total gross external debt at the end of the first quarter. This share has declined progressively from a high of 28% reached in 2012.

FULL DOCUMENT: http://www.statcan.gc.ca/daily-quotidien/170613/dq170613a-eng.pdf

ECONOMY

Bank of Canada. 12 June 2017. Canadian economy showing encouraging signs, says Senior Deputy Governor Wilkins

Winnipeg, Manitoba - With the adjustment to lower oil prices largely behind us, there are encouraging signs that growth is broadening across regions and sectors, Senior Deputy Governor Carolyn A. Wilkins told the Associates of the Asper School of Business in a speech today.

Senior Deputy Governor Wilkins discussed how having more broad-based economic growth makes it more likely that it will be sustainable over the medium term. This is the horizon Bank of Canada policy-makers consider as they set policy to achieve the Bank’s 2 per cent inflation target.

“While broad-based growth is desirable, it’s not under the direct control of monetary policy, and it’s not our objective. We target a 2 per cent inflation rate,” she said.

Senior Deputy Governor Wilkins focused on diversity in sources of growth from three perspectives: progress made in adjusting to lower oil prices, the range of industries that are growing and the evolution of the labour market.

One sign of progress in adjusting to lower oil prices is the bounce-back in capital expenditures in the oil and gas sector, which is helping to underpin renewed growth in business investment. Another comes from rising consumer demand in energy-intensive provinces. And Bank of Canada models also point to a broadening in provincial activity this year, reinforcing recent results in the Bank’s Business Outlook Survey.

“What’s encouraging is that this growth is not being driven by just a few key industries,” Senior Deputy Governor Wilkins said. The data show that more than 70 per cent of industries have been expanding and the labour market continues to improve.

However, slack in the economy is still translating into below-target inflation, Senior Deputy Governor Wilkins said, and risks to the outlook remain.

To meet its inflation objective, the Bank must consider not only current economic conditions, but also how they will evolve, she said.

“If you saw a stop light ahead, you would begin letting up on the gas to slow down smoothly,” said Senior Deputy Governor Wilkins. “You don’t want to have to slam on the brakes at the last second. Monetary policy must also anticipate the road ahead.”

Bank of Canada. 12 June 2017. Canadian Economic Update: Strength in Diversity. Remarks. Carolyn A. Wilkins - Senior Deputy Governor. The Associates of the Asper School of Business. Winnipeg, Manitoba

Introduction

I am very pleased to join you here in Winnipeg. Thank you to the Associates of the Asper School of Business for the invitation.

I was able to get out for a run this morning at The Forks. It is a beautiful area, and I was struck by the impressive architecture of the Canadian Museum for Human Rights.

I am looking forward to visiting it this week. The museum reminds us that all people are worthy of respect and dignity, regardless of their differences. The 150th anniversary of Confederation of Canada is the perfect opportunity to reflect on the strength that comes from diversity. Just a couple of weeks ago, the Bank of Canada issued a commemorative bank note that celebrates the diversity of our nation builders and of our landscape.

Diversity comes in many forms, and today I will speak about economic diversity and the strength that comes from having multiple sources of growth. As you will remember, the Canadian economy was hit hard by the collapse in oil prices in 2014. The adjustment to lower oil prices is now largely behind us, and we are looking for signs that the sources of growth are broadening across sectors and regions. As I will explain, the signs are encouraging.

My colleagues and I spend a lot of time poring over data to see how the economy is evolving. Data rarely tell the whole story, though, which is why we also spend a lot of time talking to people, firms, financial market participants, industry associations, labour groups and others. We do this through formal surveys on important economic issues and through outreach discussions. And, for years now, the Bank has held one of its Board of Directors’ meetings outside Ottawa every year.

In fact, there is a Board meeting in Winnipeg this week, and we will have an opportunity to exchange views with local business people and other community members. We are looking forward to these discussions because this province is a vibrant microcosm of the Canadian economy.

While Manitoba has a number of unique dimensions—ranging from world-class ballet to world-class winters—it shares almost the same structure as the overall Canadian economy when it comes to sources of gross domestic product (GDP) (Chart 1).

Manitoba’s diverse economy has been a source of strength over the past decade. Its economy has expanded by slightly more than 2 per cent a year on average since 2006. That is about half a percentage point higher than the Canadian economy overall for the same period.

As I talk about economic diversity today, I will first explain why it matters to a central bank whose main goal is to achieve low, stable and predictable inflation. I will then walk you through what key sets of information are telling us. Finally, I will outline some of the issues that we are considering as we prepare for our next economic update. This will be published in our Monetary Policy Report on 12 July, along with our interest rate decision.

Why Diversity Matters

Diversity comes in many forms. Let me mention two that relate to the Canadian economy. The first is diversity with respect to our nation’s industrial structure, in other words, the range of goods and services produced in Canada. This is important because sectoral diversity makes the economy more resilient—although not immune—to shocks. It is the economic equivalent to not putting all of our eggs in one basket. Anyone who has attended business school or managed an investment portfolio will be familiar with the benefits of diversification.

Let us remember, Canada has benefited over history from its wealth in natural resources.1 But when oil prices fell from their highs in mid-2014, the regions of Canada that rely on the oil and gas sector were hit hard. As these regions underwent a difficult adjustment process, sectors in other parts of the country were able to help absorb the slack that was created. The service sector was a primary force. That demonstrates the benefit of diversity in the Canadian economy.

Monetary policy stimulus and a lower dollar together provided critical support to aggregate demand and facilitated the adjustment of labour and capital. You will remember that the Bank of Canada reduced the policy rate by 50 basis points in 2015, to near-historical lows.

The second form of diversity—which I will focus on today—relates to the sources of economic growth. Generally speaking, while growth might bounce around from quarter to quarter, it is more likely to be sustainable over the medium term if its sources are broad-based. For example, growth in exports helps generate the income required to sustain growth in household spending without the need to borrow from abroad. Similarly, demand growth is more likely to be sustainable if matched by growth in capacity-enhancing business investment. There are also important sectoral and geographic aspects to sustainability.

While broad-based growth is desirable, it is not under the direct control of monetary policy, and it is not our objective. We target a 2 per cent inflation rate. That means that it is the outlook for overall inflationary pressure and related risks that matters most when we consider the appropriate stance for monetary policy. So even if only a few sectors were expanding enough to absorb the excess capacity in the aggregate economy, we would need to take the appropriate monetary policy action to meet our inflation target.

So let us look at how the economy has been performing recently.

Signs that Growth Is Broadening

When we assess the extent to which the sources of growth are broadening, we look at the economy from a number of perspectives. These include the progress made in adjusting to lower oil prices, the range of industries that are growing and the evolution of the labour market. As I discuss each in turn, I will point to some signs that growth is broadening across regions and sectors, although not to the same extent.

Adjustment to lower oil prices

Let us start with the adjustment to lower oil prices. In 2015 and 2016, the starkest effects of the drop in oil prices on GDP were in business investment. Firms in the oil and gas sector cut capital spending in half, shutting down oil rigs and cancelling investment plans. Investment in the rest of the economy was also subdued, in part as a result of the weakness in non-commodity exports, especially last year. The economy kept growing, thanks to household spending, and activity was concentrated in regions where the energy sector was not as important.

Today, as we move past the adjustment to lower oil prices, we are seeing the economy pick up. A couple of weeks ago we got the national accounts data from Statistics Canada for the first quarter of this year. It was pretty impressive, with growth at 3.7 per cent. And the figures show business investment growing again. This is in large part because capital expenditures in the oil and gas sector have bounced back. That is good news. That said, investment growth in this sector is likely to moderate if oil prices stay around where they are today. More generally, ongoing uncertainty about the policies of the US administration is weighing on investment plans. And, given how business investment has declined in the past two years, we flagged it as one of the downside risks to the outlook in our April Monetary Policy Report.

Growth in the first quarter was also fuelled by the usual suspects—consumer spending and residential investment. However, growth in the housing sector is expected to slow from exceptionally high rates, and we are already seeing this in the most recent data on housing starts and resales. It is too early to tell how the recent housing measures introduced in Ontario will ultimately affect activity and prices in and around Toronto. In Vancouver, when similar measures were introduced last year, we saw the market cool for a period of time. But it is picking up again.

So, given we expect household spending to slow somewhat, it could surprise us and provide an unexpected boost to growth in the near term, which is another risk we mentioned in April. Higher-than-expected spending, if funded by credit, could add to the vulnerabilities in the household sector. We have been monitoring these for some time and highlighted them in last week’s Financial System Review. In this regard, the recent policy measures taken by federal and provincial governments are welcome.

If there was one disappointment in the first-quarter figures, it was exports. We actually saw a decline of exports of services, which had been performing very well. At the same time, goods exports were flat. We have been working hard to understand the forces behind the data.

Stepping back from the quarterly data, there are other signs of adjustment. We see indications that demand in energy-intensive provinces is strengthening, after having fallen in 2015 and the first half of 2016. You just need to look at motor vehicle sales and housing resales (Chart 2).

One challenge we have when assessing the geographic diversity of growth is that it takes longer for provincial data to be published—this year’s data on growth by province will not be available until well into 2018. That is why Bank of Canada staff recently developed models to get a timelier read on provincial GDP.2 These models point to a broadening in provincial activity this year, in contrast to the lopsided growth we have seen over the past couple of years (Chart 3).

We also see a regional broadening of demand in the results of our most recent Business Outlook Survey. This survey asks 100 businesses every quarter about things like sales, employment and investment intentions. Executives across the country responded more optimistically about their future sales and their investment plans than they were just a few quarters ago.

Range of growing industries

We also see a broadening when it comes to growth across industries (Chart 4).3 We can see the adverse effect the oil price shock had on goods production in 2015 and the first half of 2016. The fact that growth was positive overall was due to a resilient service sector. As the oil and gas and related sectors stabilized, the goods sector as a whole started contributing again.

What is encouraging is that this growth is not being driven by just a few key industries. The data show that more than 70 per cent of industries have been expanding—a rate we have not seen since the oil price shock. That is the kind of diversity that helps support strong and sustained overall growth.4

When we think about the main drivers of economic growth, many of us picture industries like mining, motor vehicles or aerospace. While these sectors still matter a great deal to the economy, many service industries are increasing in importance. Computer systems design and related services have been growing nearly 10 per cent in the past year. This sector is now as big in Canada as motor vehicles and aerospace combined. It is not all about computers—more areas of the service sector, such as financial services and air transportation, are engines of growth. This is helping to support the household spending we have seen.

Labour market developments

Let me turn now to labour markets. Developments here are largely consistent with the evolution of economic activity I just discussed. It is not surprising that job growth in the past couple of years had been concentrated in services, offsetting significant losses in goods employment. Jobs in goods-producing industries are now on the rise, and the share of sectors adding workers is growing.

Some sectors stand out. The technology sector has been creating a lot of jobs, many of which are very well paid. Other sectors that have seen strong job growth include finance and insurance, health care and education.

As sources of growth become more diverse, gains in employment are spreading across the country (Chart 5). Now, we know that the adjustment in the labour market is still under way in some regions, and this is difficult for many people and their families. Alberta and Newfoundland and Labrador, in particular, have not recovered all the jobs lost in the aftermath of the oil price shock.

Taking Care of Business

Being able to judge the sustainability and evolution of growth is critical for a forward-looking central bank that targets inflation over the medium term. To meet this objective, we use our policy interest rate to stimulate or slow economic activity, depending on how we judge the evolution of inflationary pressures. Once inflation reaches our target, maintaining it there requires growth to be sustained at the economy’s speed limit—what we refer to as “potential output growth.” Low, stable and predictable inflation, in turn, allows people to make financial decisions with more confidence.

Monetary policy actions influence financial conditions and economic decisions right away but can take as long as two years to have their full effect on inflation. To ensure that inflation gets back to target on a sustainable basis, we must consider not only current economic conditions but also how they will evolve. If you saw a stop light ahead, you would begin letting up on the gas to slow down smoothly. You do not want to have to slam on the brakes at the last second. Monetary policy must also anticipate the road ahead.

Right now, slack in the economy is still translating into inflation that is below our target. Headline inflation stood at 1.6 per cent in April, in part because of the transitory effects of competition among food retailers. We look at several measures of core inflation to see past the transient volatility in headline inflation.5 These measures have drifted down in recent quarters and range from 1.3 to 1.6 per cent. This is consistent with the lagged effects of excess supply in past quarters.

Other indicators also point to ongoing spare capacity. We have seen moderate growth in wages, and the number of hours that people work has only recently picked up, although employment growth has been strong. Our base-case projection in the April Monetary Policy Report was for the output gap to close sometime in the first half of 2018 and inflation to return sustainably to target around the same time.

We are in the process of doing our next projection, which will be released in July. We will digest all the new data since the April Report and update our assessment of inflationary pressures. We will also look at how the main risks we highlighted in that report have evolved. I have already mentioned the risk of slower investment growth and the risk of stronger growth in household spending. We also underscored the risk that even stronger growth in the United States could lead to a big jump in business confidence, igniting “animal spirits” as John Maynard Keynes would have put it. And, given that we do not know how much capacity might be rebuilt as the economy expands, we pointed to the possibility that potential growth may be stronger than assumed in our base-case projection.

We are all acutely aware of the uncertainty around the policies of the US administration—whether it is about trade, tax or the regulatory environment. We already factored in some of the effects of that uncertainty in our April outlook. Until we get more information, it will be difficult to gauge the impact of any proposed policy changes more precisely. This will likely remain an important uncertainty in our projection, but life goes on and decisions must be made in the meantime.

Our judgment on the appropriate stance of monetary policy will continue to be based on the outlook for inflation and on the full range of risks—both upside and downside—to that outlook. An important aspect of our inflation assessment is that the economic drag from lower oil prices is now largely behind us. And the 50 basis point reduction in our policy rate in 2015 has facilitated this adjustment. As growth continues and, ideally, broadens further, Governing Council will be assessing whether all of the considerable monetary policy stimulus presently in place is still required.

Conclusion

Time to wrap up.

There are still risks to the Canadian economic outlook. That said, when you look at the economy from different perspectives, there is reason to be encouraged. Growth has been robust in recent quarters. As we celebrate Canada’s 150th birthday and the strength that comes from the diversity of its people, we are seeing the benefits of its economic diversity as well.

The strengthening economic activity in regions and sectors that rely on energy is working to diversify the sources of growth across the country. And, while there is still room for improvement in the labour market, stronger growth is translating into job gains across a wider range of regions and sectors.

At present, there is significant monetary policy stimulus in the system. As we work toward our interest rate decision on 12 July, we will be focusing on the data and talking to many people like you to get a better sense of what is happening on the ground.

One thing that remains clear is the Bank’s commitment to achieving its inflation target so that Canadians can make their financial decisions with more confidence.

I would like to thank Eric Santor and Stephen Murchison for their help in preparing this speech.

Foot Notes

- S. S. Poloz, “Riding the Commodity Cycle: Resources and the Canadian Economy” (speech to Calgary Economic Development, Calgary, Alberta, 21 September 2015).

- T. Chernis, C. Cheung and G. Velasco. “A Three-Frequency Dynamic Factor Model for Nowcasting Canadian Provincial GDP Growth.” Bank of Canada Staff Discussion Paper No. 2017-8 (June 2017).

- The goods sector includes oil and gas, mining and manufacturing, while the service sector includes trade, transportation, digital and professional services, health care, education and public administration.

- To examine the breadth of activity over a given period of time, we constructed a diffusion index that includes the 22 subcomponents of GDP at basic prices and measures the proportion that are growing. This index has been increasing since the third quarter of 2016.

- The measures are CPI-median, which is based on the price change located at the 50th percentile (in terms of the CPI basket weights) of the distribution of price changes; CPI-trim, which excludes CPI components whose rates of change in a given month are located in the tails of the distribution of price changes; and CPI-common, which tracks common price changes across categories in the CPI basket.

FULL DOCUMENT: http://www.bankofcanada.ca/wp-content/uploads/2017/06/remarks-120617.pdf

The Globe and Mail. Jun. 13, 2017. Canadian dollar extends surge on BoC economic outlook

BARRIE MCKENNA

A top Bank of Canada official says economic growth has spread to most regions and industries in Canada – the latest clue that the central bank is pondering when to start raising interest rates.

The central bank is seeing “some signs that growth is broadening across regions and sectors,” senior deputy governor Carolyn Wilkins told a business audience on Monday in Winnipeg. Her remarks sent the Canadian dollar flying: The loonie jumped more than half a cent immediately after they were posted on the bank’s website. By Monday evening, it rose above 75 cents (U.S.) for the first time since April.

The loonie continued its climb into Tuesday. It was just below 75.5 cents in the early hours.

“We are seeing the economy pick up,” insisted Ms. Wilkins, Governor Stephen Poloz’s No. 2 executive at the bank.

The improving outlook has prompted the Bank of Canada to start looking ahead to its first rate hike in nearly seven years.

Ms. Wilkins said the central bank will be “assessing” whether to keep pumping low-interest fuel into the economy as “growth continues and, ideally, broadens further.”

The economy surged ahead at an annual pace of 3.7 per cent in the first quarter.

Bank officials seem relatively unconcerned that inflation has drifted lower in recent months and now sits well below the bank’s 2-per-cent target. Ms. Wilkins played down recent weak inflation numbers, saying much of it is “transitory” and caused by intense competition in the grocery business.

Ms. Wilkins hinted that the bank may have to act pre-emptively as it anticipates how economic conditions will evolve.

“If you saw a stop light ahead, you would begin letting up on the gas to slow down smoothly,” she said. “You do not want to have to slam on the brakes at the last second. Monetary policy must also anticipate the road ahead.”

It is the clearest sign yet of a bias towards tightening monetary policy. The bank’s key overnight-interest rate has been fixed at 0.5 per cent since July, 2015, when it made the second of two quarter-point cuts to deal with the aftershocks of the oil price collapse. The Bank of Canada has not raised rates in nearly seven years.

Nonetheless, most economists who follow the central bank don’t expect an interest-rate hike until some time next year.

Toronto-Dominion Bank economist Brian DePratto said Ms. Wilkins appears to be “preparing markets” for eventual higher rates.

“This speech may be sending a clear signal, but don’t expect the Bank of Canada to hit the hike button just yet,” added Mr. DePratto, who doesn’t expect a rate increase until early 2018. “A significant haze of uncertainty continues to hang over the economy.”

As evidence of the economy’s “broadening” strength, Ms. Wilkins pointed to the resumption in business investment, largely driven by a bounce-back in spending in the oil patch. She also said that consumer demand has picked up in the energy-producing provinces, leading to a broadening of economic strength and job creation across the country. A chart accompanying Ms. Wilkins’s speech shows that employment is up in eight out of 10 provinces since last October. New Brunswick and Newfoundland and Labrador have continued to lose jobs.

Growth is also spreading across sectors and industries, Ms. Wilkins said. More than 70 per cent of industries are now expanding output. She highlighted computer systems and design, which has grown at a rate of 10 per cent in the past year – a sector that is now as large as vehicle production and aerospace combined.

But the economic news is not all good. Ms. Wilkins pointed to a number of risks that could cause the economy to stall, including another fall in the price of oil, sluggish exports and the continuing uncertainty over what U.S. President Trump will do on taxes and trade.

“We are all acutely aware of the uncertainty around the policies of the U.S. administration – whether it is about trade, tax or the regulatory environment,” she said. “Until we get more information, it will be difficult to gauge the impact of any proposed policy changes more precisely. This will remain an important uncertainty in our projection, but life goes on and decisions must be made in the meantime.”

REUTERS. Jun 13, 2017. Bank of Canada's Poloz: Rate cuts have largely done their work

OTTAWA (Reuters) - Interest rate cuts instituted in 2015 have largely done their job as the Canadian economy gathers momentum, the Bank of Canada's head said on Tuesday, the second top official in as many days to set the stage for eventual rate hikes.

Bank of Canada Governor Stephen Poloz said in an interview with CBC Radio that the economic recovery from weak oil prices appeared to be widening.

"What that suggests to us is that the interest rate cuts we put in place in 2015 have largely done their work," Poloz said. "So that's very reassuring, we're encouraged by the data."

The change in tone from policymakers this week has prompted traders to raise their bets on rate hikes this year, with markets pricing in a 72.9 percent chance of an increase by December.

Nonetheless, Poloz noted a stronger export picture remained a big missing element and suggests there are competitiveness challenges for Canadian companies.

A second missing element is business investment, which has been slow, though there are signs it is now picking up, he said.

"It isn't time to throw a party," Poloz added.

Poloz's comments echoed a more hawkish tone from Senior Deputy Governor Carolyn Wilkins on Monday, though he stopped short of suggesting a near-term rate move, economists said.

"The uncertainties that threaten the export and investment outlook likely preclude an imminent hike but recent communication from the Bank of Canada are commensurate with the 50 basis points of tightening we have penciled in for the first half of 2018 - or slightly earlier," said Nick Exarhos, economist at CIBC.

The Canadian dollar added to its strength against the greenback on Poloz's comments. [CAD/]

Wilkins said on Monday the central bank would assess whether it needs to keep interest rates at near-record lows as the economy continues to grow.

The Bank of Canada cut rates twice in 2015 in response to tumbling oil prices that put the economy in a brief recession. The bank has held rates at 0.50 percent since then.

(Reporting by Leah Schnurr; Editing by Chizu Nomiyama and Bernadette Baum)

REUTERS. Jun 12, 2017. Bank of Canada hints at possible rate hikes, C$ jumps

By Rod Nickel

WINNIPEG (Reuters) - The Bank of Canada will assess whether it needs to keep interest rates at near-record lows as the economy continues to grow, a senior official said on Monday, raising the prospect that a rate hike could come sooner than anticipated and lifting the Canadian dollar.

The change in tone for the central bank, which said earlier this year rate cuts remained on the table, sent the Canadian dollar CAD= to its strongest level against the greenback since April 18.

In the bank's most upbeat comments on the economy, Senior Deputy Governor Carolyn Wilkins said first-quarter growth was "pretty impressive," while there were encouraging signs growth was broadening.

"As growth continues and, ideally, broadens further, Governing Council will be assessing whether all of the considerable monetary policy stimulus presently in place is still required," Wilkins told a business audience.

Wilkins said Canada had largely adjusted to a drop in oil prices LCOc1 CLc1 that prompted the bank to cut rates twice in 2015, to 0.50 percent, to bolster the economy, which slipped into a brief recession.

The speech's hawkish tone is the first acknowledgement from the bank that the next move is likely to be a hike, said Royce Mendes, senior economist at CIBC Capital Markets.

The bank makes its next rate decision on July 12. While many economists had expected the bank to start raising in 2018, markets were pricing in a 52 percent chance of a hike by the end of 2017 following Wilkins' speech.

"It looks as though the bank is looking to shift gears," said Benjamin Reitzes, senior economist at BMO Capital Markets.

"There's a decent chance that if things go right over the next few months, rate hikes could be coming sooner than everybody thought."

Wilkins acknowledged tax and trade policies in the United States will likely remain an important uncertainty in the bank's outlook and it will be difficult to gauge the impact without more information.

She added, "life goes on and decisions must be made in the meantime."

Even if only a few sectors were expanding enough to absorb excess capacity, the bank would need to take the appropriate monetary policy action to meet its 2 percent inflation target, she said.

Inflation is currently at 1.6 percent, thanks in part to slack in the economy, Wilkins said. She noted other indicators also point to ongoing spare capacity, including only moderate growth in wages.

(Reporting by Rod Nickel; Writing by Leah Schnurr and David Ljunggren in Ottawa; Editing by Dan Grebler and James Dalgleish)

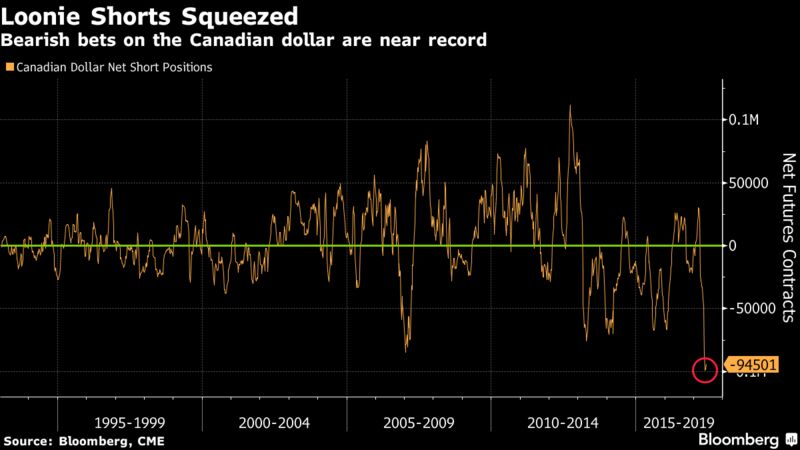

BLOOMBERG. 2017 M06 13. Short Sellers Get Notice as Bank of Canada Signals Rate Hike

by Theophilos Argitis and Maciej Onoszko

- Wilkins say central bank to assess whether stimulus cut needed

- Country’s currency is second-worst performing major in 2017

- Bank of Canada Encouraged About Economic Recovery

Count the Bank of Canada out as an enabler.

Investors betting against the Canadian economy lost a key support Monday when the country’s central bank indicated it’s turned bullish enough to consider raising interest rates -- a surprise policy change the Bank of Montreal called a “potential watershed.’’ Governor Stephen Poloz added to the bullish tone in a CBC interview Tuesday by saying rates have been “extraordinarily low,” and that rate cuts “have done their job.”

The comments Monday by Carolyn Wilkins, the central bank’s second-highest-ranking official, are a rebuke to pessimists who say unprecedented household debt and record home prices will trigger a disorderly unwind of Canada’s housing markets, some of which may have entered into bubble territory. The Bank of Canada may have contributed to the negativity. Until now, it’s been slow to acknowledge a sharp economic rebound, suggesting instead the economy wasn’t healthy enough to warrant higher interest rates.

“It was a painful day for those investors holding short positions in the Canadian dollar in the hope of a short-term gain,” said Matthew Strauss, a Toronto-based portfolio manager at Signature Global Asset Management.

The loonie surged after Wilkins’s comments, ending Monday up 1.1 percent to C$1.3350 per U.S. dollar in Toronto, the steepest increase since March and the biggest advance among Group-of-10 peers. The loonie added to gains Tuesday, rising 0.33 percent. Odds of a 2017 rate increase almost doubled to 59 percent, from 30 percent on Friday, based on trading in the swaps market. Yields on benchmark 2-year government bonds surged 11 basis points to 0.84 percent, and added another three basis points Tuesday to the highest since January 2015.

‘Real Problems’

Short sellers betting against Canada’s housing market have been emboldened by several factors: price gains that far exceed incomes; the recent run on deposits and share collapse at mortgage lender Home Capital Group Inc.; and a downgrade of the nation’s banks by Moody’s Investors Service. Even while the economy has been on a roll -- with annualized growth of 3.7 percent in the first quarter -- the boom times in Vancouver and Toronto look to some investors like the debt-fueled housing bubbles that wrought havoc in so many Western countries last decade.

“I’m starting to believe that there could be some real problems with Canada,” Carson Block, an investor and founder of Muddy Waters LLC, said in a May 31 interview. Canada may be “the hottest market in the world for short sellers; if not, it could be.” The investor is shorting Canadian miner Asanko Gold Inc.

Famed short seller Marc Cohodes has been betting against Home Capital since November 2014 -- when the stock was near its peak. The California investor is also targeting mortgage lender Equitable Group Inc. Net short positions in the Canadian dollar meanwhile hit an all-time high going back more than two decades.

In a speech Monday, Wilkins highlighted how the nation has largely emerged from the oil price decline that prompted policy makers to cut interest rates twice in 2015, citing “pretty impressive” first-quarter GDP growth that was the well above any other G-7 economy. The recovery is also broadening across regions and sectors, giving policy makers “reason to be encouraged” about its sustainability.

She downplayed worries about Toronto’s housing market and, while acknowledging slack still remains in the economy, said policy makers need to keep their eye on the future evolution of growth, not only current economic conditions. The analogy she used was of a car needing time to brake ahead of a traffic light.

“As growth continues and, ideally, broadens further, Governing Council will be assessing whether all of the considerable monetary policy stimulus presently in place is still required,” Wilkins said. “At present, there is significant monetary policy stimulus in the system.”

Market sentiment had already turned more bullish on Canada before her speech. Short-interest positions of Canada’s six-biggest lender are down, with Toronto-Dominion Bank and Royal Bank of Canada -- the two largest -- now at about 1.6 percent of the free float, according to Markit data. That compares with about 5.9 percent at Royal Bank on April 25, and 5.5 percent in early April for Toronto-Dominion Bank, the data show.

Short sellers have also been easing pressure on Home Capital. Short positions on the shares dropped to 20 percent earlier Monday, the least since July 2015, according to Markit data. The alternative lender’s stock tumbled in April after Ontario’s securities regulator accused the company of misleading investors about mortgage fraud.

The sense that Canada’s economy is strong enough to overcome any vulnerabilities in the financial system was also the key theme last week at a press conference by Governor Stephen Poloz. The optimism is an about face from earlier this year, when he spoke about the possibility of another reduction in the bank’s benchmark lending rate, after cutting it twice in 2015 to 0.5 percent.

“This is a pretty glaring hint that policy is now biased to tighten, with the next move likely a lot sooner than many had expected,” Bank of Montreal Chief Economist Doug Porter said in a note to investors.

The Toronto-based bank moved up its call for a rate increase to January, from its previous call for an April move. The bank said an October hike is a “real possibility.”

SOFTWOOD LUMBER

The Globe and Mail. Jun. 12, 2017. Canada, U.S. still ‘far apart’ in softwood dispute: Freeland

NICOLAS VAN PRAET

MONTREAL — Canada and the United States are still "far apart" in the softwood lumber dispute, federal foreign affairs minister Chrystia Freeland said ahead of a planned meeting with Quebec lumber producers Monday.

The minister said she is in regular contact with U.S. Commerce Department officials and with its secretary, Wilbur Ross, on the softwood issue. She thanked Mr. Ross for his level of engagement on the file but said there is no settlement in view.

"Our positions are still quite far apart," Ms. Freeland told reporters after a speech to the International Economic Forum of the Americas in Montreal. "But I think that talking is always a good thing and that is something that we are doing very actively and energetically."

The United States slapped countervailing duties of nearly 20 per cent on most Canadian softwood shipments to the United States earlier this year after a complaint from the American lumber lobby. The issue is one of several in what appears to be an escalating trade battle between Canada and the United States.

"The fact is that the U.S. economy needs our lumber," Ms. Freeland said, evoking middle class Americans who want to buy a house or make home improvements like building a backyard deck. "The U.S. industry on its own does not produce enough lumber for the U.S. economy."

Ottawa has introduced an $867-million aid package for the Canadian softwood industry to help the pain of punitive U.S. duties. The effort has been decried by the U.S. Lumber Coalition as "a new government subsidy" for Canadian producers that only tilts the trade scale further in Canada's favour while threatening U.S. jobs.

U.S. producers have been arguing for decades that Canadian provinces unfairly subsidize lumber exports by undercharging domestic forestry companies for cutting on crown land. Timber auctions and other mechanisms have been introduced to address such concerns but the United States argues they are not enough.

Canadian producers affected by the duties include Canfor, Resolute Forest Products, Tolko and West Fraser. The industry accounts for 60,000 jobs and 180 businesses in Quebec alone.

In appeals at the both the World Trade Organization and North American Free Trade Agreement level, Canada has always successfully defended its position in previous softwood lumber subsidy disputes. Ottawa is confident that won't change, Ms. Freeland said.

The minister's comments come just days after she made a major speech in the House of Commons in which she said Canada will forge its own path in international relations because it can no longer rely on the United States for global leadership. In the speech, she championed the benefits of free trade, now under challenge with the rise of U.S. protectionism under President Donald Trump.

Taking advantage of that new political climate, Boeing Co. in April launched a trade complaint against Montreal-based plane maker Bombardier Inc. and its flagship C Series airliner. Boeing alleges that Bombardier benefits from unfair subsidies in selling the jet into the U.S. market, hurting American jobs.

Ms. Freeland reiterated Monday her government's belief that the complaint has no merit and that it would stand by the company. The U.S. Department of Commerce is expected to render a decision by July 21 on whether to apply tariffs on Bombardier planes to counter the alleged subsidization.

BLOOMBERG. 2017 M06 13. U.S.-Canada Trade Spat Set to Sharpen as Lumber Decision Nears

by Jen Skerritt

- Anti-dumping duties may be as high as 15%: RBC analyst

- Lumber futures in Chicago have jumped on supply concerns

The U.S. is setting the stage to heighten one of its most-contested trade battles with Canada this month as a decision over lumber duties nears.

The U.S. Department of Commerce is scheduled to announce whether it will impose preliminary anti-dumping duties on Canadian softwood lumber by the end of June. The U.S. already escalated the row in April by slapping tariffs of up to 24.1 percent on Canadian shipments. This month’s decision may bring the combined duties to more than 30 percent according to RBC Capital Markets. The fees would be levied against companies such as West Fraser Timber Co. and Canfor Corp.

While the spat between the world’s two largest trading partners goes back decades, tensions have intensified amid U.S. President Donald Trump’s tough talk on the North American Free Trade Agreement. The dispute over softwood lumber was reignited in November when the U.S. lumber industry filed a petition asking for duties. The group alleges Canadian wood is heavily subsidized and imports are harming U.S. mills and workers. Lumber futures in Chicago have surged amid concerns that the trade battle will disrupt supplies.

“I think it’s the consistent U.S. position, and probably pumped up with Trump, to hit the Canadians hard off the bat, force them to the negotiation table by hurting them financially,” said Paul Quinn, an analyst at RBC Capital Markets in Vancouver. “You’re going to see less shipments out of Canada as a result of a 30 percent tax.”

Why the U.S. and Canada Are Fighting About Lumber: QuickTake Q&A

Canada has pledged to fight the duties and announced it will assist lumber producers with a C$867 million ($642 million) aid package. While talks with the U.S. are continuing, the two sides “are still quite far apart,” Foreign Affairs Minister Chrystia Freeland said in Montreal on Monday.

Canada is the world’s largest softwood lumber exporter and the U.S. is its biggest market. The dispute has contributed to a more than 18 percent surge in wood prices from the end of January to mid-May as companies raised prices to compensate for potential duties, according to a Bloomberg Intelligence report. The most-recent deal between the countries expired in October 2015, and Canada was given one year to ship lumber tariff-free while both parties were negotiating a new accord.

“If we have no deal it will be years, years of litigation,” Quebec Premier Philippe Couillard said Monday. “We were ready to defend our workers and the softwood lumber industry before Mr. Trump was elected, and this is what we are doing as we speak.”

Higher Tariffs

Anti-dumping duties on Canadian softwood lumber may reach 10 percent to 15 percent as the U.S. tries to hurt producers financially, RBC’s Quinn said.

That rate would put combined duties in line with the 32 percent duties imposed during a previous softwood trade battle in 2001, CIBC analyst Hamir Patel said in an April 24 report. After a previous trade pact expired, anti-dumping duties reached as high as 12.6 percent from 2001 to 2006, according to the report.

The additional tariff will probably further lift lumber prices as Canadian companies raise quotes to offset the cost, said Kevin Mason, managing director of Vancouver-based ERA Forest Products Research.

________________

LGCJ.: