US ECONOMICS

CHINA

U.S. Department of State. 06/29/2020. On China’s Coercive Family Planning and Forced Sterilization Program in Xinjiang. Michael R. Pompeo, Secretary of State

The world received disturbing reports today that the Chinese Communist Party is using forced sterilization, forced abortion, and coercive family planning against Uyghurs and other minorities in Xinjiang, as part of a continuing campaign of repression. German researcher Adrian Zenz’s shocking revelations are sadly consistent with decades of CCP practices that demonstrate an utter disregard for the sanctity of human life and basic human dignity. We call on the Chinese Communist Party to immediately end these horrific practices and ask all nations to join the United States in demanding an end to these dehumanizing abuses.

U.S. Department of State. 06/29/2020. U.S. Government Ending Controlled Defense Exports to Hong Kong. Michael R. Pompeo, Secretary of State

The Chinese Communist Party’s decision to eviscerate Hong Kong’s freedoms has forced the Trump Administration to re-evaluate its policies toward the territory. As Beijing moves forward with passing the national security law, the United States will today end exports of U.S.-origin defense equipment and will take steps toward imposing the same restrictions on U.S. defense and dual-use technologies to Hong Kong as it does for China.

The United States is forced to take this action to protect U.S. national security. We can no longer distinguish between the export of controlled items to Hong Kong or to mainland China. We cannot risk these items falling into the hands of the People’s Liberation Army, whose primary purpose is to uphold the dictatorship of the CCP by any means necessary.

It gives us no pleasure to take this action, which is a direct consequence of Beijing’s decision to violate its own commitments under the U.N.-registered Sino-British Joint Declaration. Our actions target the regime, not the Chinese people. But given Beijing now treats Hong Kong as “One Country, One System,” so must we. The United States is reviewing other authorities and will take additional measures to reflect the reality on the ground in Hong Kong.

U.S. Department of State. 06/29/2020. On China’s Threats to Impose Visa Restrictions on U.S. Officials. Michael R. Pompeo, Secretary of State

The Chinese Communist Party’s crackdown on Hong Kong prompted the United States to retool its relationship with the territory. The Chinese Communist Party’s threats to retaliate by restricting visas for U.S. citizens exposes once again how Beijing refuses to take responsibility for its own choices. If China wants to regain the trust of Hong Kongers and the international community, it should honor the promises it made to the Hong Kong people and to the United Kingdom in the U.N.-registered 1984 Sino-British Joint Declaration.

CORONAVIRUS

FED. June 30, 2020. Testimony. Coronavirus and CARES Act. Chair Jerome H. Powell. Before the Committee on Financial Services, U.S. House of Representatives, Washington, D.C.

Chairwoman Waters, Ranking Member McHenry, and other members of the Committee, thank you for the opportunity to testify today to discuss the extraordinary challenges our nation is facing and the steps we are taking to address them.

We meet as the pandemic continues to cause tremendous hardship, taking lives and livelihoods both at home and around the world. This is a global public health crisis, and we remain grateful to our health-care professionals for delivering the most important response, and to our essential workers who help us meet our daily needs. These dedicated people put themselves at risk day after day in service to others and to our country.

Beginning in March, the virus and the forceful measures taken to control its spread induced a sharp decline in economic activity and a surge in job losses. Indicators of spending and production plummeted in April, and the decline in real gross domestic product, or GDP, in the second quarter is likely to be the largest on record. The arrival of the pandemic gave rise to tremendous strains in some essential financial markets, impairing the flow of credit in the economy and threatening an even greater weakening of economic activity and loss of jobs.

The crisis was met by swift and forceful policy action across the government, including the Coronavirus Aid, Relief, and Economic Security Act (CARES Act). This direct support is making a critical difference not just in helping families and businesses in a time of need, but also in limiting long-lasting damage to our economy.

As the economy reopens, incoming data are beginning to reflect a resumption of economic activity: Many businesses are opening their doors, hiring is picking up, and spending is increasing. Employment moved higher, and consumer spending rebounded strongly in May. We have entered an important new phase and have done so sooner than expected. While this bounceback in economic activity is welcome, it also presents new challenges—notably, the need to keep the virus in check.

While recent economic data offer some positive signs, we are keeping in mind that more than 20 million Americans have lost their jobs, and that the pain has not been evenly spread. The rise in joblessness has been especially severe for lower-wage workers, for women, and for African Americans and Hispanics. This reversal of economic fortune has caused a level of pain that is hard to capture in words as lives are upended amid great uncertainty about the future.

Output and employment remain far below their pre-pandemic levels. The path forward for the economy is extraordinarily uncertain and will depend in large part on our success in containing the virus. A full recovery is unlikely until people are confident that it is safe to reengage in a broad range of activities.

The path forward will also depend on the policy actions taken at all levels of government to provide relief and to support the recovery for as long as needed.

The Federal Reserve's response to these extraordinary developments has been guided by our mandate to promote maximum employment and stable prices for the American people as well as our role in fostering the stability of the financial system. Our actions and programs directly support the flow of credit to households, to businesses of all sizes, and to state and local governments. These programs benefit Main Street by providing financing where it is not otherwise available, helping employers to keep their workers, and allowing consumers to continue spending. In many cases, by serving as a backstop to key financial markets, the programs help increase the willingness of private lenders to extend credit and ease financial conditions for families and businesses across the country. The passage of the CARES Act by Congress was critical in enabling the Federal Reserve and the Treasury Department to establish many of these lending programs. We are strongly committed to using these programs, as well as our other tools, to do what we can to provide stability, to ensure that the recovery will be as strong as possible, and to limit lasting damage to the economy.

In discussing the actions we have taken, I will begin with monetary policy. In March, we lowered our policy interest rate to near zero, and we expect to maintain interest rates at this level until we are confident that the economy has weathered recent events and is on track to achieve our maximum-employment and price-stability goals.

In addition to these steps, we took forceful measures in four areas: open market operations to restore market functioning; actions to improve liquidity conditions in short-term funding markets; programs, in coordination with the Treasury Department, to facilitate more directly the flow of credit to households, businesses, and state and local governments; and measures to encourage banks to use their substantial capital and liquidity buffers built up over the past decade to support the economy during this difficult time.

Let me now turn to our open market operations. As tensions and uncertainty rose in mid-March, investors moved rapidly toward cash and shorter-term government securities, and the markets for Treasury securities and agency mortgage-backed securities, or MBS, started to experience strains. These markets are critical to the overall functioning of the financial system and to the transmission of monetary policy to the broader economy. In response, the Federal Open Market Committee purchased Treasury securities and agency MBS in the amounts needed to support smooth market functioning. With these purchases, market conditions improved substantially, and in early April we began to gradually reduce our pace of purchases. To sustain smooth market functioning and thereby foster the effective transmission of monetary policy to broader financial conditions, we will increase our holdings of Treasury securities and agency MBS over the coming months at least at the current pace. We will closely monitor developments and are prepared to adjust our plans as appropriate to support our goals.

Amid the tensions and uncertainties of mid-March and as a more adverse outlook for the economy took hold, investors exhibited greater risk aversion and pulled away from longer-term and riskier assets as well as from some money market mutual funds. To help stabilize short-term funding markets, we lengthened the term and lowered the rate on discount window loans to depository institutions. The Board also established, with the approval of the Treasury Department, the Primary Dealer Credit Facility (PDCF) under our emergency lending authority in section 13(3) of the Federal Reserve Act. Under the PDCF, the Federal Reserve provides loans against good collateral to primary dealers that are critical intermediaries in short-term funding markets. Similar to the large-scale purchases of Treasury securities and agency MBS that I mentioned earlier, this facility helps restore normal market functioning.

In addition, under section 13(3) and together with the Treasury Department, we set up the Commercial Paper Funding Facility, or CPFF, and the Money Market Mutual Fund Liquidity Facility, or MMLF. Millions of Americans put their savings into these markets, and employers use them to secure short-term funding to meet payroll and support their operations. Both of these facilities have equity provided by the Treasury Department to protect the Federal Reserve from losses. After the announcement and implementation of these facilities, indicators of market functioning in commercial paper and other short-term funding markets improved substantially, and rapid outflows from prime and tax-exempt money market funds stopped.

In mid-March, offshore U.S. dollar funding markets also came under stress. In response, the Federal Reserve and several other central banks announced the expansion and enhancement of dollar liquidity swap lines. In addition, the Federal Reserve introduced a new temporary Treasury repurchase agreement facility for foreign monetary authorities. These actions helped stabilize global U.S. dollar funding markets, and they continue to support the smooth functioning of U.S. Treasury and other financial markets as well as U.S. economic conditions.

As it became clear the pandemic would significantly disrupt economies around the world, markets for longer-term debt also faced strains. The cost of borrowing rose sharply for those issuing corporate bonds, municipal debt, and asset-backed securities (ABS) backed by consumer and small business loans. In effect, creditworthy households, businesses, and state and local governments were unable to borrow at reasonable rates and other terms, which would have further reduced economic activity. In addition, small and medium-sized businesses that traditionally rely on bank lending faced large increases in their funding needs as measures taken to contain the spread of the virus forced them to temporarily close or limit operations, substantially curtailing revenues.

To support the longer-term financing that is critical to economic activity, the Federal Reserve, in cooperation with the Department of the Treasury and using equity provided for that purpose under the CARES Act, announced a number of emergency lending facilities under section 13(3) of the Federal Reserve Act. These facilities are designed to ensure that credit would flow to borrowers and thus support economic activity.

On March 23, the Board announced that it would support consumer and business lending by establishing the Term Asset-Backed Securities Loan Facility (TALF). The TALF is authorized to extend up to $100 billion in loans and is backed by $10 billion in CARES Act equity. This facility lends against top-rated securities backed by auto loans, credit card loans, other consumer and business loans, commercial mortgage-backed securities, and other assets. The TALF supports credit access by consumers and businesses and provides liquidity to the broader ABS market. The facility made its first loans on June 25, and, to date, has extended $252 million in loans to eligible borrowers. Since the TALF was announced, ABS spreads have contracted significantly. Thus, the facility might be used relatively little and mainly serve as a backstop, assuring lenders that they will have access to funding and giving them the confidence to make loans to households and businesses.

To support the credit needs of large employers, the Federal Reserve also established the Primary Market Corporate Credit Facility (PMCCF) and the Secondary Market Corporate Credit Facility (SMCCF). These facilities primarily purchase bonds issued by U.S. companies that were investment grade on March 22, 2020. The two facilities have a combined purchase capacity of up to $750 billion and are backed by $75 billion in CARES Act equity. Final terms and operational details on the PMCCF were announced on June 29, and it stands ready to purchase newly issued corporate bonds and syndicated loans, serving as a backstop for businesses seeking to refinance their existing credit or obtain new funding. The SMCCF buys outstanding corporate bonds and shares in corporate bond exchange-traded funds (ETFs) to facilitate smooth functioning of the secondary market. The SMCCF complements the PMCCF, because improvements in secondary-market functioning associated with the SMCCF facilitate access by companies to bond and loan markets on reasonable terms. The SMCCF launched with ETF purchases on May 12. Earlier this month, the facility began gradually reducing purchases of ETFs as it started buying a broad and diversified portfolio of individual corporate bonds to more directly support smooth functioning and market liquidity in the secondary market. Purchase volumes are tied to market functioning and are currently at very low levels. The facility currently holds a total of about $10 billion in bonds and ETF shares.

Following the announcement of the two corporate credit facilities in late March, conditions in the corporate bond market improved significantly. Credit spreads on investment-grade bonds retraced much of the widening experienced in February and March, and issuance in the primary market rebounded strongly. In the secondary market, liquidity also improved, and by mid-April, flows out of mutual funds and ETFs specializing in corporate bonds reversed.1

The Federal Reserve also launched the Main Street Lending Program, which is designed to provide loans to small and medium-sized businesses that were in good financial standing before the pandemic; such firms generally are dependent on bank lending for credit because they are too small to tap bond markets directly. Under the Main Street program, banks originate new loans or increase the size of existing loans to eligible businesses and sell loan participations to the Federal Reserve. The facility is backed by $75 billion in CARES Act equity and can purchase up to $600 billion in loan participations. The Federal Reserve has published all of the legal documents that borrowers and lenders will need to sign under the program and lender registration began on June 15. Loan participations will be purchased soon. Additionally, the Federal Reserve recently sought feedback on a proposal to expand the Main Street program to include loans made to small and medium-sized nonprofit organizations, such as hospitals and universities. Nonprofits provide vital services around the country, and the program would likewise offer them support.

While businesses in certain sectors that were particularly hard hit by the pandemic have reported continued difficulty in accessing credit, the Small Business Administration's Paycheck Protection Program (PPP), which draws from existing bank lines, has apparently met the immediate credit needs of many small businesses. In the months ahead, Main Street loans may prove a valuable resource for firms that were in sound financial condition prior to the pandemic.

To bolster the effectiveness of the Small Business Administration's PPP, on April 16, the Federal Reserve launched the Paycheck Protection Program Liquidity Facility. The facility supplies liquidity to lenders backed by their PPP loans to small businesses and has the capacity to lend up to the full amount of the PPP. As of last week, the facility held over $65 billion in outstanding term loans to participating financial institutions. The most recent monthly survey from the National Federation of Independent Business released in May indicates that small businesses have been able to meet their funding needs in recent months largely due to the PPP.2

To help state and local governments better manage cash flow pressures in order to continue to serve households and businesses in their communities, the Federal Reserve, together with the Treasury Department, established the Municipal Liquidity Facility (MLF). The MLF is backed by $35 billion of CARES Act equity and has the capacity to purchase up to $500 billion of short-term debt directly from U.S. states, counties, cities, and certain multistate entities. The facility became operational on May 26, and, to date, the MLF has purchased $1.2 billion worth of short-term municipal debt. With the MLF and other facilities in place as a backstop to the private market, many parts of the municipal bond market have significantly recovered from the unprecedented stress experienced earlier this year. Municipal bond yields have declined considerably, issuance has been robust over the past two months, and market conditions have improved.3

The tools that the Federal Reserve is using under its 13(3) authority are for times of emergency, such as the ones we have been living through. When economic and financial conditions improve, we will put these tools back in the toolbox.

The final area where we took steps was in bank regulation. The Board made several adjustments, many temporary, to encourage banks to use their positions of strength to support households and businesses. Unlike the 2008 financial crisis, banks entered this period with substantial capital and liquidity buffers and improved risk-management and operational resiliency. As a result, they have been well positioned to cushion the financial shocks we are seeing. In contrast to the 2008 crisis when banks pulled back from lending and amplified the economic shock, in this crisis they have greatly expanded loans to customers and have helped support the economy.

The Federal Reserve has been entrusted with an important mission, and we have taken unprecedented steps in very rapid fashion over the past few months. In doing so, we embrace our responsibility to the American people to be as transparent as possible. With regard to the facilities backed by equity from the CARES Act, we have conducted broad outreach and sought public input that has been crucial in their development. For example, in response to comments received, the Treasury and the Federal Reserve have made a number of changes to expand the scope of the Main Street Lending Program to cover a broader range of borrowers and to increase the flexibility of loan terms. And we are now disclosing and will continue to disclose, on a monthly basis, names and details of participants in each facility; amounts borrowed and interest rate charged; and overall costs, revenues, and fees for each of these facilities.

We recognize that our actions are only part of a broader public-sector response. Congress's passage of the CARES Act was critical in enabling the Federal Reserve and the Treasury Department to establish many of the lending programs. The CARES Act and other legislation provide direct help to people, businesses, and communities. This direct support can make a critical difference not just in helping families and businesses in a time of need, but also in limiting long-lasting damage to our economy. We understand that the work of the Federal Reserve touches communities, families, and businesses across the country. Everything we do is in service to our public mission. We are committed to using our full range of tools to support the economy and to help assure that the recovery from this difficult period will be as robust as possible.

Thank you. I'd be happy to take your questions.

Notes

- See Nina Boyarchenko, Richard Crump, Anna Kovner, Or Shachar, and Peter Van Tassel (2020), "The Primary and Secondary Market Corporate Credit Facilities," Federal Reserve Bank of New York, Liberty Street Economics (blog), May 26.

- William C. Dunkelberg and Holly Wade (2020), NFIB Small Business Economic Trends (Washington: National Federation of Independent Business, May), https://assets.nfib.com/nfibcom/SBET-May-2020.pdf.

- See Board of Governors of the Federal Reserve System (2020), Financial Stability Report (Washington: Board of Governors, May).

INVESTIMENT

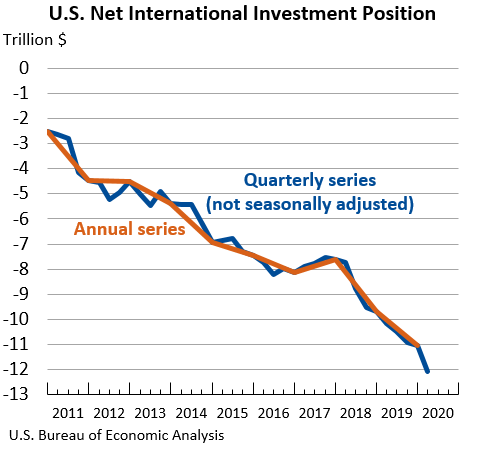

DoC. BEA. JUNE 30, 2020. U.S. International Investment Position, First Quarter 2020, Year 2019, and Annual Update. First Quarter 2020

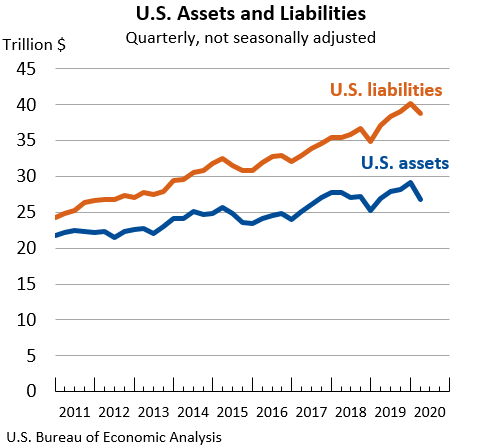

The U.S. net international investment position, the difference between U.S. residents’ foreign financial assets and liabilities, was –$12.06 trillion at the end of the first quarter of 2020, according to statistics released by the U.S. Bureau of Economic Analysis (BEA). Assets totaled $26.77 trillion and liabilities were $38.82 trillion.

At the end of the fourth quarter of 2019, the net investment position was –$11.05 trillion (Table 1).

The –$1.01 trillion change in the net investment position from the fourth quarter of 2019 to the first quarter of 2020 came from net financial transactions of –$184.2 billion and net other changes in position, such as price and exchange rate changes, of –$822.8 billion (Table A).

Coronavirus (COVID-19) Impact on First Quarter 2020 International Investment Position

In the first quarter of 2020, the declines in U.S. assets and liabilities reflect the impact of the COVID-19 pandemic. The disruption to global production and financial markets led to sharp declines in global stock prices, the appreciation of the U.S. dollar against most foreign currencies, and a shortage of U.S. dollar liquidity in foreign money markets. The stock price declines and the appreciation of the U.S. dollar are reflected in price changes and exchange rate changes. Currency swap transactions between the U.S. Federal Reserve System and several foreign central banks to alleviate the shortage of U.S. dollar liquidity contributed to record levels of U.S. acquisition of assets and U.S. incurrence of liabilities. The full economic effects of the COVID-19 pandemic cannot be quantified in the statistics for the first quarter because the impacts are generally embedded in source data and cannot be separately identified. For more information on the currency swaps, see the technical note that accompanied the June 19 international transactions accounts news release.

Table A. Quarterly Change in the U.S. Net International Investment Position

Billions of dollars, not seasonally adjusted

Billions of dollars, not seasonally adjusted

| Position, 2019 Q4 | Change in position in 2020 Q1 | Position, 2020 Q1 | |||

| Total | Attributable to: | ||||

| Financial transactions | Other changes in position 1 | ||||

| U.S. net international investment position | -11,050.5 | -1,007.0 | -184.2 | -822.8 | -12,057.5 |

| Net position excluding financial derivatives | -11,070.7 | -1,022.1 | -162.4 | -859.8 | -12,092.8 |

| Financial derivatives other than reserves, net | 20.2 | 15.2 | -21.8 | 37.0 | 35.3 |

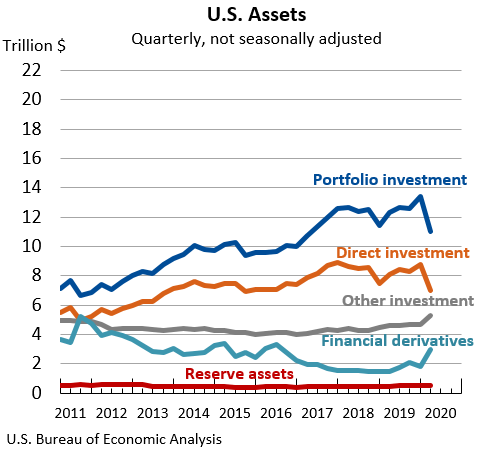

| U.S. assets | 29,152.8 | -2,385.7 | (2) | (2) | 26,767.1 |

| Assets excluding financial derivatives | 27,362.4 | -3,595.8 | 739.9 | -4,335.7 | 23,766.6 |

| Financial derivatives other than reserves | 1,790.4 | 1,210.1 | (2) | (2) | 3,000.5 |

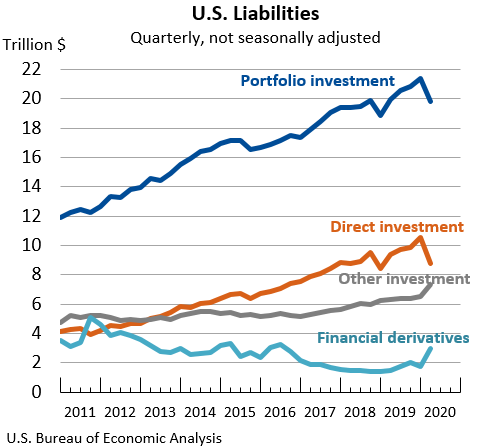

| U.S. liabilities | 40,203.3 | -1,378.7 | (2) | (2) | 38,824.6 |

| Liabilities excluding financial derivatives | 38,433.0 | -2,573.6 | 902.3 | -3,475.9 | 35,859.4 |

| Financial derivatives other than reserves | 1,770.3 | 1,194.9 | (2) | (2) | 2,965.2 |

| 1. Disaggregation of other changes in position into price changes, exchange rate changes, and other changes in volume and valuation is only presented for annual statistics (see table B and table 2 in this release). 2. Financial transactions and other changes in financial derivatives positions are available only on a net basis; they are not separately available for U.S. assets and U.S. liabilities. | |||||

U.S. liabilities decreased by $1.38 trillion, to a total of $38.82 trillion, at the end of the first quarter, mostly reflecting decreases in direct investment and portfolio investment liabilities that were partly offset by increases in financial derivatives and in other investment liabilities. Direct investment liabilities decreased by $1.78 trillion, to $8.77 trillion, and portfolio investment liabilities decreased by $1.61 trillion, to $19.78 trillion, mostly reflecting decreases in U.S. stock prices amid the COVID-19 pandemic.

The statistics in this release reflect the annual update of the U.S. international investment position (IIP). With this update, BEA has incorporated newly available and revised source data, and has reclassified certain U.S. government capital subscriptions or other contributions to international organizations from loan assets to other equity assets, a new category within other investment assets. The reclassification of other equity assets results in the addition of line items in the IIP and the international transactions accounts (ITAs) for transactions and positions in other equity assets and liabilities. Also, BEA updated other equity and loan assets to incorporate U.S. government transactions and positions that were not previously included. Quarterly statistics are revised for the first quarter of 2006 to the fourth quarter of 2019. Annual statistics are revised for 1976-2019.

For 1976-1999, the reclassification of other equity assets from loan assets results in offsetting revisions between these two investment categories, leaving the statistics for U.S. assets and for the net IIP unchanged.

For 2000-2015, the statistics for U.S. assets and for the net IIP are revised up by an average of $0.8 billion annually, reflecting the incorporation of U.S. government transactions and positions that were not previously included in other equity and loan assets.

For 2016-2019, revisions to the IIP statistics reflect newly available and revised source data that impact all major categories of assets and liabilities (Table 3).

Additional information on these changes is published in “Preview of the 2020 Annual Update of the International Economic Accounts” in the April 2020 issue of the Survey of Current Business. An article describing the revisions to the statistics will be published in the July 2020 issue.

Newly Available and Revised Source Data: Key Providers and Years Affected

The U.S. net international investment position was –$11.05 trillion at the end of 2019 compared to –$9.67 trillion at the end of 2018 (Table 2).

The –$1.38 trillion change in the net investment position from the end of 2018 to the end of 2019 came from net financial transactions of –$395.5 billion and net other changes in position, such as price and exchange rate changes, of –$980.5 billion (Table B).

U.S. assets increased by $3.92 trillion, to a total of $29.15 trillion, at the end of 2019, reflecting increases in all major categories of assets, particularly in portfolio investment and direct investment assets. Portfolio investment assets increased by $1.94 trillion, to $13.38 trillion, and direct investment assets increased by $1.35 trillion, to $8.80 trillion, driven mainly by foreign stock price increases.

U.S. liabilities increased by $5.30 trillion, to a total of $40.20 trillion, at the end of 2019, reflecting increases in all major categories of liabilities, particularly in portfolio investment and direct investment liabilities. Portfolio investment liabilities increased by $2.55 trillion, to $21.39 trillion, and direct investment liabilities increased by $2.15 trillion, to $10.55 trillion, driven mainly by U.S. stock price increases.

Table B. Annual Change in the U.S. Net International Investment Position

Billions of dollars

Billions of dollars

| Position, 2018 | Change in position in 2019 | Position, 2019 | |||||||

| Total | Attributable to: | ||||||||

| Financial transactions | Other changes in position | ||||||||

| Total | Price changes | Exchange rate changes | Changes in volume and valuation n.i.e | ||||||

| U.S. net international investment position | -9,674.4 | -1,376.1 | -395.5 | -980.5 | (1) | (1) | (1) | -11,050.5 | |

| Net position excl. derivatives | -9,716.5 | -1,354.2 | -357.2 | -997.0 | -1,104.9 | 119.5 | -11.5 | -11,070.7 | |

| Financial derivatives, net | 42.0 | -21.9 | -38.3 | 16.4 | (1) | (1) | (1) | 20.2 | |

| U.S. assets | 25,233.8 | 3,919.0 | (2) | (2) | (2) | (2) | (2) | 29,152.8 | |

| Assets excl. derivatives | 23,784.2 | 3,578.2 | 440.8 | 3,137.4 | 3,080.1 | 128.3 | -71.0 | 27,362.4 | |

| Financial derivatives | 1,449.6 | 340.8 | (2) | (2) | (2) | (2) | (2) | 1,790.4 | |

| U.S. liabilities | 34,908.2 | 5,295.1 | (2) | (2) | (2) | (2) | (2) | 40,203.3 | |

| Liabilities excl. derivatives | 33,500.7 | 4,932.4 | 798.0 | 4,134.4 | 4,185.0 | 8.8 | -59.4 | 38,433.0 | |

| Financial derivatives | 1,407.5 | 362.7 | (2) | (2) | (2) | (2) | (2) | 1,770.3 | |

| 1. Data are not separately available for price changes, exchange rate changes, and changes in volume and valuation n.i.e. (not included elsewhere). 2. Financial transactions and other changes in financial derivatives positions are available only on a net basis; they are not separately available for U.S. assets and U.S. liabilities. | |||||||||

________________

ORGANISMS

GLOBAL ECONOMY

IMF. 06/30/2020. F&D: Remittances to Fall by $100 Billion in 2020

COVID-19 is crippling the economies of rich and poor countries alike. Yet for many low-income and fragile states, the economic shock will be magnified by the loss of remittances. In a new article for F&D, the IMF's Antoinette Sayeh and Ralph Chami dig deeper into how the pandemic threatens to dry up this vital source of income, and what measures can be taken to tackle this challenge.

Remittance flows into low-income and fragile states represent a lifeline that supports households as well as provides much-needed tax revenue. As of 2018, remittance flows to these countries reached $350 billion, surpassing foreign direct investment, portfolio investment, and foreign aid as the single most important source of income from abroad (see Chart 1). A drop in remittance flows is likely to heighten economic, fiscal, and social pressures on governments of these countries already struggling to cope even in normal times.

Shocks to the economies of migrant-host countries—just the sorts of shocks being caused by the coronavirus pandemic—can be transmitted to those of the remittance-recipient countries. For example, for a recipient country that receives remittances representing at least 10 percent of its annual GDP, a 1 percent decrease in the host country’s output gap (the difference between actual and potential growth) will tend to decrease the recipient country’s output gap by almost 1 percent. Remittances represent much more than 10 percent of GDP for many countries, led by Tajikistan and Bermuda, at more than 30 percent (see Chart 2).

The pandemic will deliver a blow to remittance flows that may be even worse than during the financial crisis of 2008, and it will come just as poor countries are grappling with the impact of COVID-19 on their own economies. Migrant workers who lose their employment are likely to reduce remittances to their families back home. Recipient countries will lose an important source of income and tax revenue just when they need it most. In fact, according to the World Bank, remittance flows are expected to drop by about $100 billion in 2020, which represents roughly a 20 percent drop from their 2019 level (see Chart 3). Fiscal and trade balances would be affected, and countries’ ability to finance and service their debt would be reduced.

A prolonged crisis could worsen pressure in labor markets of rich countries, and out-of-work migrants could lose their resident status in host countries and be forced to return home. For example, in Gulf states such as Saudi Arabia and the United Arab Emirates, which rely on migrant labor from the Middle East, North Africa, and Southeast Asia, the drop in the price of oil and economic activity could result in migrants (some of whom are already infected with the virus) returning home. They are likely to join the jobless in their home countries—in labor markets already brimming with unemployed youth—as well as put more pressure on already fragile public health systems. This could heighten social pressure in countries already ill prepared to deal with the pandemic and possibly also fuel spillovers beyond their borders.

People escaping tough situations in their own countries are likely to seek other shores, but richer countries, also in the midst of fighting the virus, may have very little desire to allow migrants in—potentially leading to an even greater refugee crisis.

WHAT CAN BE DONE?

It is in the best interest of rich countries for migrants not to go home, as well as to provide resources for poor countries to fight the pandemic. Infection rates are much higher in rich countries and are especially high among migrant workers owing to their dismal working and housing conditions. Migrants who go home are at risk of taking the virus with them. If this happens, poor countries will provide a rich incubator for the virus that will boomerang as refugees seek new shores. Then it will take decades—and many lives—for the world to be rid of this virus.

THREE KEY ACTIONS:

First, host countries need to stabilize the employment opportunities of the migrant workers in their economies. Relief packages that target employment protection for citizens in rich countries can also help migrant workers remain employed.

Second, countries receiving returning migrants will need help to contain, mitigate, and reduce the escalation of outbreaks. Donor countries must help with the cost of virus mitigation, in an effort to lessen the severity of the crisis in local economies and stave off potential spillovers.

And third, given that poor countries’ governments have limited room for maneuver, these countries will need the assistance of international financial institutions and the donor community. International financial institutions need to shore up fiscal and balance of payments assistance to these countries. Perhaps now more than ever, the global effort to meet Sustainable Development Goal 10—reducing the high cost of remittances to 3 percent—could take center stage.

FINAL WORD

What does the remittance crisis look like in your country? What are some other ways in which we can tackle this challenge from a policy lens?

FULL DOCUMENT: https://www.imf.org/external/pubs/ft/fandd/2020/06/COVID19-pandemic-impact-on-remittance-flows-sayeh.htm?utm_medium=email&utm_source=govdelivery

CORONAVIRUS

IMF. 06/30/2020. REOPENING ASIA: HOW THE RIGHT POLICIES CAN HELP ECONOMIC RECOVERY

By Chang Yong Rhee

For the first time in living memory, Asia’s growth is expected to contract by 1.6 percent—a downgrade to the April projection of zero growth. While Asia’s economic growth in the first quarter of 2020 was better than projected in the April World Economic Outlook—partly owing to early stabilization of the virus in some countries, projections for 2020 have been revised down for most of the countries in the region due to weaker global conditions and more protracted containment measures in several emerging economies.

In the absence of a second wave of infections and with unprecedented policy stimulus to support the recovery, growth in Asia is projected to rebound strongly to 6.6 percent in 2021. But even with this fast pickup in economic activity, output losses due to COVID-19 are likely to persist. We project Asia’s economic output in 2022 to be about 5 percent lower compared with the level predicted before the crisis; and this gap will be much larger if we exclude China, where economic activity has already started to rebound.

Clouds on the horizon

Our projections for 2021 and beyond assume a strong rebound in private demand; however, this may be optimistic for several reasons:

- Slower growth in trade. Asia is heavily dependent on global supply chains and cannot grow while the whole world is suffering. Asia’s trade is expected to contract significantly due to weaker external demand, with total trade (exports plus imports) projected to decline by about 20 percent in 2020 in Japan, India, and the Philippines. Reorienting Asia’s growth model toward domestic demand and away from a heavy reliance on exports has begun but will take more time to be completed.

- Longer than expected lockdowns. Even when lockdown measures are fully relaxed, economic activity is not likely to return to full capacity, due to changes in individual behaviors and measures put in place to maintain physical distancing and reduce contagion. Our recent study shows that while a lockdown may lead to a contraction in economic activity—as measured by industrial production—of about 12 percent a month, a full reversal in containment measures may increase economic activity by only about 7 percent. In addition, many Asian economies—especially Pacific Islands countries—depend on tourism, remittances, and other services that require in-person contact, which will take a lot longer to recover.

- Rising inequality. Inequality had already been rising in Asia, and our recent research shows how past pandemics led to higher income inequality and hurt employment prospects of those with limited education. These effects are likely to be exacerbated in Asia due to the large proportion of informal workers, making the recovery more protracted.

- Weak balance sheets and geopolitical tensions. Weakened household and corporate balance sheets in many Asian countries can weigh negatively on investor sentiment and amplify the effect of increasing uncertainties associated with geopolitical tensions.

Policies for the recovery

Asian countries are experimenting re-opening, and policies must be geared toward supporting the nascent recovery without exacerbating vulnerabilities. They must use fiscal stimulus wisely and complement it with economic reforms. The priorities include:

Close coordination between monetary and fiscal policy. Monetary policy should help ensure the flow of credit to households and business. Countries facing higher fiscal constraints could also use the central bank’s balance sheet more flexibly, aggressively, and transparently to support bank lending to smaller firms. In the face of large outflows, balance sheet mismatches and limited scope for macroeconomic policy maneuver, temporary capital outflow measures may be needed.

Resource reallocation. A robust recovery hinges on exiting the current phase of support and transitioning to new policies that help ensure resources are reallocated appropriately beyond the initial focus on preventing bankruptcies of incumbent firms, and thereby strengthen the solvency of firms. For example, flattening the bankruptcy curve by streamlining the restructuring and insolvency frameworks; ensuring that banks are adequately capitalized; and facilitating equity injections into viable firms and risk capital for new firms.

Addressing inequalities. Access to health and basic services, finance, and the digital economy should be broadened. Social safety nets should be expanded to extend unemployment insurance coverage to informal workers. Addressing pervasive informality will also require comprehensive labor and product market reforms to improve the business environment and removing onerous legal and regulatory obstacles (especially for startups), and policies to rationale the tax system.

IMF support

Since the outbreak of the pandemic, the IMF has offered policy advice, financial assistance, and other support—including virtual initiatives to enhance skills and develop capacity among government officials—to all its member countries. To date, the Fund has provided emergency support to 7 countries across the Asia-Pacific region, with others expressing interest in our emergency financing instruments. Given the large and looming uncertainties at this moment, countries with sound fundamentals may want also to consider use of the Fund’s precautionary credit lines such as the Flexible Credit Line and the Short-Term Liquidity Line to insure against an abrupt tightening in external liquidity. Indeed, S&P Global and Fitch have both published notes stating that facilities like the Fund’s precautionary credit lines could, by cushioning economies, support ratings.

FULL DOCUMENT: https://blogs.imf.org/2020/06/30/reopening-asia-how-the-right-policies-can-help-economic-recovery/?utm_medium=email&utm_source=govdelivery

________________

ECONOMIA BRASILEIRA / BRAZIL ECONOMICS

DESEMPREGO

IBGE. 30/06/2020. PNAD Contínua: taxa de desocupação é de 12,9% e taxa de subutilização é de 27,5% no trimestre encerrado em maio de 2020

A taxa de desocupação (12,9%) no trimestre móvel encerrado em maio de 2020 cresceu 1,2 ponto percentual em relação ao trimestre de dezembro de 2019 a fevereiro de 2020 (11,6%) e 0,6 ponto percentual em relação ao mesmo trimestre de 2019 (12,3%).

| Indicador/Período | Mar-Abr-Maio 2020 | Dez-Jan-Fev 2020 | Mar-Abr-Maio 2019 |

|---|---|---|---|

| Taxa de desocupação | 12,9% | 11,6% | 12,3% |

| Taxa de subutilização | 27,5% | 23,5% | 25,0% |

| Rendimento real habitual | R$2.460 | R$2.374 | R$2.344 |

| Variação do rendimento habitual em relação a: | 3,6% | 4,9% | |

A população desocupada (12,7 milhões de pessoas) teve aumento de 3,0% (368 mil pessoas a mais) frente ao trimestre móvel anterior (12,3 milhões de pessoas) e ficou estatisticamente estável frente a igual trimestre de 2019 (13,0 milhões de pessoas).

A população ocupada (85,9 milhões) caiu 8,3% (7,8 milhões de pessoas a menos) em relação ao trimestre anterior e de 7,5% (7,0 milhões de pessoas a menos) em relação ao mesmo trimestre de 2019. Ambas as quedas foram recordes da série histórica.

O nível da ocupação (percentual de pessoas ocupadas na população em idade de trabalhar) caiu para 49,5%, o menor da série histórica iniciada em 2012, com redução de 5,0 p.p. frente ao trimestre anterior (54,5%) e de 5,0 p.p. frente a igual trimestre de 2019 (54,5%).

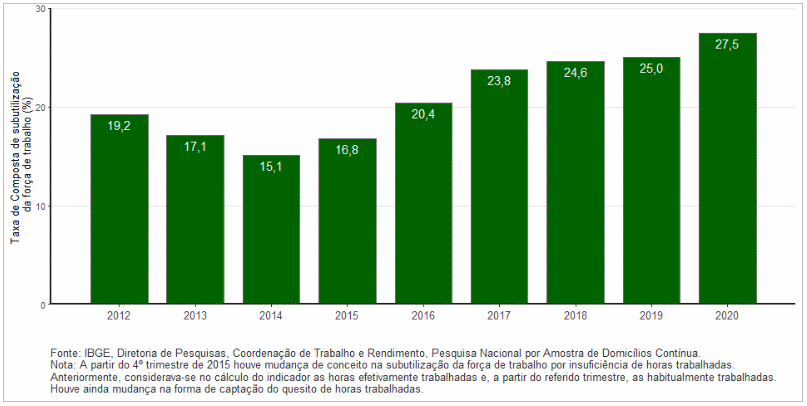

A taxa composta de subutilização (27,5%) foi recorde da série, com elevação de 4,0 p.p. em relação ao trimestre anterior (23,5%) e 2,5 p.p em relação a 2019 (25,0%).

A população subutilizada (30,4 milhões de pessoas) foi recorde da série, crescendo 13,4%, (3,6 milhões de pessoas a mais), frente ao trimestre anterior (26,8 milhões) e 6,5% (1,8 milhão de pessoas a mais) frente a igual período de 2019 (28,5 milhões de pessoas).

A população fora da força de trabalho (75,0 milhões de pessoas) apresentou um incremento de 9,0 milhões de pessoas (13,7%) quando comparada com o trimestre anterior e de 10,3 milhões de pessoas (15,9%) frente ao mesmo trimestre de 2019.

A população desalentada (5,4 milhões) registrou mais um recorde na série, aumentando 15,3% frente ao trimestre anterior e (10,3%) frente a igual período de 2019.

O percentual de desalentados em relação à população na força de trabalho ou desalentada (5,2%) também foi recorde, registrando alta de 1,0 p.p. em relação ao trimestre anterior (4,2%) e de 0,8 p.p. na comparação com o mesmo trimestre de 2019 (4,4%).

O número de empregados com carteira de trabalho assinada no setor privado (exclusive trabalhadores domésticos) caiu para 31,1 milhões, menor nível da série, sendo 7,5% abaixo (-2,5 milhões de pessoas) do trimestre anterior e 6,4% abaixo (-2,1 milhões de pessoas a menos) do mesmo período de 2019.

O número de empregados sem carteira assinada no setor privado (9,2 milhões de pessoas) apresentou uma redução de 2,4 milhão de pessoas (-20,8%) em relação ao trimestre anterior e 2,2 milhões de pessoas (-19,0%) em relação ao mesmo trimestre do ano anterior.

O número de trabalhadores por conta própria caiu para 22,4 milhões de pessoas, uma redução de 8,4% frente ao trimestre anterior e de 6,7% frente a igual período de 2019.

A taxa de informalidade foi de 37,6% da população ocupada, ou 32,3 milhões de trabalhadores informais, o menor da série, iniciada em 2016. No trimestre anterior, a taxa havia sido 40,6% e no mesmo trimestre de 2019, 41,0%.

O rendimento real habitual (R$ 2.460) subiu 3,6% frente ao trimestre anterior e 4,9% frente ao mesmo período de 2019. Já a massa de rendimento real habitual (R$ 206,6 bilhões de reais), recuou 5,0% em relação ao trimestre anterior e 2,8% em relação a 2019.

A massa de rendimento inclui apenas rendimentos provenientes de trabalho, não incluindo, portanto, rendimentos de outras fontes, tais como: Aposentadoria, Aluguel, Bolsa Família, BPC, Auxílio Desemprego, Auxílio Emergencial etc. O Auxílio Emergencial pago para as pessoas por estarem afastadas do trabalho não está incluído no rendimento de trabalho da PNAD Contínua. Os rendimentos provenientes de outras fontes são captados na PNAD Contínua de forma a serem divulgados no consolidado do ano, não permitindo, portanto, a sua disponibilização na divulgação trimestral.

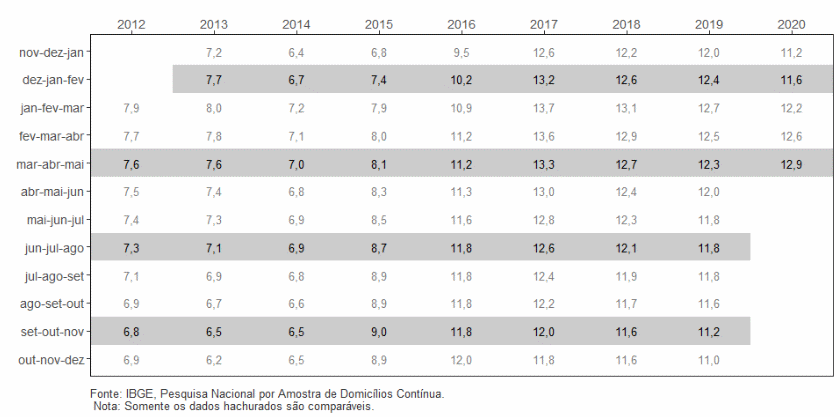

Taxa de desocupação – Brasil – 2012-2020 (%)

Nos grupamentos de atividades, em relação ao trimestre móvel anterior, houve aumento apenas no grupamento de Administração pública, defesa, seguridade social, educação, saúde humana e serviços sociais (4,6%).

Por outro lado, houve redução em nove grupamentos: Agricultura, pecuária, produção florestal, pesca e aquicultura (-4,5%), Indústria (-10,1%), Construção (-16,4%), Comércio, reparação de veículos automotores e motocicletas (-11,1%), Transporte, armazenagem e correio (-8,4%), Alojamento e alimentação (-22,1%), Informação, Comunicação e Atividades Financeiras, Imobiliárias, Profissionais e Administrativas (-3,2%), Outros serviços (-13,3%) e Serviços domésticos (-18,7%).

Frente a igual trimestre de 2019, também só houve aumento no grupamento que envolve a Administração pública (3,6%). Já as quedas foram: Agricultura, pecuária, produção florestal, pesca e aquicultura (-6,8%); Indústria (-7,8%); Construção (-15,6%); Comércio e reparação de veículos (-9,4%); Transporte, armazenagem e correio (-6,8%); Alojamento e alimentação (-19,5%); Outros serviços (-11,4%) e Serviços domésticos (-18,6%).

A força de trabalho (pessoas ocupadas e desocupadas), estimada em 98,6 milhões de pessoas caiu 7,0% (7,4 milhões de pessoas a menos) comparada com ao trimestre anterior e 6,9% (7,3 milhões de pessoas a menos) frente ao mesmo período de 2019.

O número de empregadores (4,0 milhões de pessoas) recuou 8,5% (-377 mil pessoas) frente ao trimestre anterior e 8,8% em relação ao mesmo trimestre de 2019 (-388 mil).

A categoria dos trabalhadores domésticos, estimada em 5,0 milhões de pessoas, recuou 18,9% frente ao trimestre anterior e de 18,6% frente a igual período do ano anterior.

Já o grupo dos empregados no setor público (12,3 milhões de pessoas), que inclui servidores estatutários e militares, apresentou aumento de 7,8% frente ao trimestre anterior e de 6,2% frente a igual período do ano anterior.

O número de subocupados por insuficiência de horas trabalhadas (5,8 milhões) recuou 10,7% (697 mil pessoas a menos) frente ao trimestre anterior e 19,9% em relação ao mesmo trimestre de 2019, quando havia no Brasil 7,2 milhões de pessoas subocupadas.

Taxa composta de subutilização – trimestres de março a maio – 2012 a 2020 – Brasil (%)

Quanto ao rendimento médio real habitual, em relação ao trimestre móvel anterior houve aumento nas categorias: Indústria (5,6%) e Construção (7,9%). Os demais grupamentos não apresentaram variação significativa. Frente ao mesmo período de 2019, o aumento foi nas categorias Indústria (8,8%) e Outros serviços (8,4%), sem variação significativa no demais.

Entre as categorias de ocupação, frente ao trimestre anterior, houve aumento no rendimento médio real habitual dos empregados com carteira de trabalho assinada (2,6%) e também dos sem carteira (7,8%). Já em relação ao mesmo período de 2019, essas mesmas categorias mostraram aumentos de 3,8% e 13,4%, respectivamente.

Rendimento médio mensal real habitualmente recebido no mês de referência, de todos os trabalhos das pessoas ocupadas – Brasil – 2012/2020 (R$)

PNAD Contínua. Pela primeira vez, menos da metade das pessoas em idade de trabalhar está ocupada. Da queda recorde de pessoas que saíram do mercado de trabalho, 5,8 milhões eram trabalhadores informais

O percentual de pessoas ocupadas na população em idade de trabalhar chegou a 49,5% no trimestre encerrado em maio, queda de cinco pontos percentuais em relação ao trimestre até fevereiro. É mais baixo nível da ocupação desde o início da Pesquisa Nacional por Amostra de Domicílios Contínua (PNAD Contínua), em 2012. Os dados da pesquisa foram divulgados hoje (30) pelo IBGE.

“Pela primeira vez na série histórica da pesquisa, o nível da ocupação ficou abaixo de 50%. Isso significa que menos da metade da população em idade de trabalhar está trabalhando. Isso nunca havia ocorrido na PNAD Contínua”, explica a analista da pesquisa, Adriana Beringuy. São 85,9 milhões de pessoas ocupadas.

A taxa de desocupação passou de 11,6%, no trimestre até fevereiro, para 12,9% no trimestre terminado em maio, atingindo 12,7 milhões de desempregados. São mais 368 mil pessoas à procura de trabalho em relação ao trimestre anterior. No mesmo período, 7,8 milhões de pessoas saíram da população ocupada, uma queda de 8,3%.

“É uma redução inédita na pesquisa e atinge principalmente os trabalhadores informais. Da queda de 7,8 milhões de pessoas ocupadas, 5,8 milhões eram informais”, destaca Beringuy.

Os trabalhadores informais somam os profissionais sem carteira assinada (empregados do setor privado e trabalhadores domésticos), sem CNPJ (empregadores e por conta própria) e sem remuneração. O número de empregados no setor privado sem carteira assinada caiu 20,8%, significando 2,4 milhões a menos no mercado de trabalho. Já os trabalhadores por conta própria diminuíram em 8,4%, ou seja, 2,1 milhões de pessoas. Com isso, a taxa de informalidade caiu de 40,6% para 37,6%, a menor desde 2016, quando o indicador passou a ser produzido.

“Numericamente nós temos uma queda da informalidade, mas isso não necessariamente é um bom sinal. Significa que essas pessoas estão perdendo ocupação e não estão se inserindo em outro emprego. Estão ficando fora da força de trabalho”, analisa a pesquisadora.

Ela explica ainda que, com a redução no número de trabalhadores informais, grupo que geralmente ganha remunerações menores, o rendimento médio habitual teve aumento de 3,6%, chegando a R$ 2.460, o maior desde o início da série. Já a massa de rendimento real foi estimada em R$ 206,6 bilhões, uma queda de 5% frente ao trimestre anterior.

1,2 milhão de trabalhadores domésticos saíram do mercado de trabalho

O número de trabalhadores domésticos, estimado em 5 milhões de pessoas, teve uma queda de 18,9% em relação ao trimestre encerrado em fevereiro. São 1,2 milhão de trabalhadores a menos no mercado de trabalho. Já o contingente de empregados no setor privado com carteira assinada (sem contar os trabalhadores domésticos) teve uma queda de 7,5%, ou seja, menos 2,5 milhões de pessoas no mercado, totalizando 31,1 milhões e atingindo o menor nível da série.

Com essas reduções, o contingente na força de trabalho (pessoas ocupadas e desocupadas) chegou a 98,6 milhões de pessoas, uma queda de 7,4 milhões (-7%) em relação ao trimestre encerrado em fevereiro.

“Uma parte importante da população fora da força é formada por pessoas que até gostariam de trabalhar, mas que não estão conseguindo se inserir no mercado, muito provavelmente em função do cenário econômico, das dificuldades em encontrar emprego, seja devido ao isolamento social, seja porque o consumo das famílias está baixo e as empresas também não estão contratando. Então esse mês de maio aprofunda tudo aquilo que a gente estava vendo em abril”, conclui Beringuy.

Comércio perde dois milhões de pessoas ocupadas

O único grupamento de atividade que teve aumento em relação ao trimestre encerrado em fevereiro foi o de administração pública, defesa, seguridade social, educação, saúde humana e serviços sociais, que cresceu 4,6% no período. Isso significa um aumento de 748 mil pessoas no setor.

Entre os outros grupamentos de atividade, o que apresentou a maior queda em relação ao número de pessoas ocupadas foi o Comércio, reparação de veículos automotores e motocicletas (-11,1%), com menos 2 milhões de empregados. Já a Indústria perdeu 1,2 milhão de pessoas (-10,1%) e a Construção, 1,1 milhão (-16,4%).

DOCUMENTO: https://agenciadenoticias.ibge.gov.br/agencia-sala-de-imprensa/2013-agencia-de-noticias/releases/28110-pnad-continua-taxa-de-desocupacao-e-de-12-9-e-taxa-de-subutilizacao-e-de-27-5-no-trimestre-encerrado-em-maio-de-2020

ECONOMIA

FGV. IBRE. 30/06/2020. Incerteza da Economia permanece em patamar extremamente elevado

O Indicador de Incerteza da Economia (IIE-Br) da Fundação Getulio Vargas caiu 16,7 pontos em junho de 2020, para 173,6 pontos. Com a segunda queda consecutiva, o indicador passou a devolver 39% da alta de 95,4 pontos observada no bimestre março-abril. Ainda assim, permanece 36,8 pontos acima do recorde anterior à pandemia de Covid-19, de 136,8 pontos, em setembro de 2015.

“O patamar ainda extremamente elevado do Indicador de Incerteza da FGV IBRE reflete problemas em três diferentes frentes: a evolução sem tréguas da pandemia de covid-19 no Brasil, o cenário econômico recessivo e a instabilidade do ambiente político. O componente de Expectativas recuou pela primeira vez desde o início da pandemia, mas perdeu apenas 2% das altas ocorridas entre março e maio, mostrando a enorme dificuldade de se formular cenários futuros para a economia brasileira no momento. Diante de tantas dificuldades é pouco provável que a incerteza retorne a níveis moderados neste ano”, afirma Anna Carolina Gouveia, Economista da FGV IBRE.

Em junho, os dois componentes do Indicador de Incerteza caminharam na mesma direção. O componente de Mídia, recuou 18,6 pontos, para 152,5 pontos, contribuindo negativamente em 16,2 pontos para a queda do índice geral no mês. O componente de Expectativas recuou 2,1 pontos, para 228,0 pontos, após acumular alta de 112,8 pontos entre março e maio, com contribuição negativa de 0,5 ponto para o comportamento do IIE-Br.

DOCUMENTO: https://portalibre.fgv.br/noticias/incerteza-da-economia-permanece-em-patamar-extremamente-elevado

CNI. 29/06/2020. Segurança jurídica será essencial para retomada de investimentos, diz Robson Andrade. Presidente da CNI participou de live do jornal O Globo, ao lado do ex-presidente da CNI Armando Monteiro; do presidente da Câmara, Rodrigo Maia; do presidente eleito do STF, Luiz Fux; e do ministro do STJ Luís Salomão

O presidente da Confederação Nacional da Indústria (CNI), Robson Braga de Andrade, afirmou que a segurança jurídica está entre os fatores mais importantes para a retomada dos investimentos e a consequente recuperação econômica do Brasil no momento pós-pandemia. Ele participou nesta segunda-feira (29) da live “Justiça e Cidadania — a importância do Judiciário na retomada da economia”, realizada pelo jornal O Globo.

Robson Andrade destacou que os investimentos estrangeiros no país serão imprescindíveis para a geração de empregos. Ele observou que há grandes oportunidades de concessões na área de infraestrutura e observou que um importante passo nesse sentido foi a aprovação do novo marco legal do saneamento básico. O presidente da CNI pontuou, no entanto, que a insegurança jurídica poderá afastar potenciais investidores.

“Vai ser muito difícil ter investidor brasileiro neste momento. Por outro lado, o investidor estrangeiro, que tem muitos fundos e busca bons ativos e boas oportunidades de negócios, olha para o Brasil e diz que o país tem muita insegurança jurídica. Esse é o grande problema que temos para investimentos no Brasil”, enfatizou Robson Andrade. Ele apontou que esse cenário é causado principalmente pelo excesso de leis, mudanças repentinas de jurisprudência nos tribunais, instabilidade das agências reguladoras e do Ministério Público.

O debate também contou com as presenças do presidente da Câmara dos Deputados, Rodrigo Maia; do presidente eleito do Supremo Tribunal Federal (STF), ministro Luiz Fux; do ministro do Superior Tribunal de Justiça (STJ) Luís Felipe Salomão; do ex-presidente da Ordem dos Advogados do Brasil (OAB) Marcus Vinícius Furtado Coêlho; do conselheiro da CNI e ex-senador Armando Monteiro Neto; e do presidente do Instituto Justiça e Cidadania, Tiago Salles. A moderação foi feita pela jornalista Flávia Oliveira.

Dificuldade das indústrias para acessar crédito em meio à pandemia

Durante a live, Robson Andrade defendeu a aprovação de uma nova lei de recuperação judicial e a regulamentação do Fundo Garantidor de Investimentos, para que empresas possam ter acesso a créditos e, assim, evitar demissões e sobreviver à crise. Ele citou que dos R$ 40 bilhões colocados à disposição de micro e pequenas empresas somente R$ 3 bilhões foram acessados.

“Estamos aguardando a regulamentação do Fundo, que é importante porque entendo que os bancos e o setor financeiro têm dificuldade de aprovar créditos para uma empresa que ele não sabe como vai estar depois da pandemia. É preciso que haja realmente uma garantia pelo Tesouro Nacional”, afirmou.

De acordo com o presidente da CNI, a ociosidade nas fábricas é de cerca de 60%, em razão da crise causada pela Covid-19, sendo que somente alguns setores da indústria não foram afetados, como os de medicamentos e produtos alimentícios.

“A ajuda do governo de R$ 600 para os trabalhadores contribuiu para o consumo de produtos essenciais e básicos. Mas o restante da indústria está trabalhando com extrema dificuldade, como o de eletrodomésticos e vestuário”, disse. “A não uniformidade entre ações dos diversos estados dificulta o trabalho da indústria. Isso tem gerado um ambiente de insegurança muito grande na indústria brasileira”, completou.

O presidente da Câmara, Rodrigo Maia, reconheceu que as medidas de crédito não estão chegando aos empresários e que a queda econômica do país no segundo semestre tende a ser maior que a projetada. “As medidas relacionadas ao crédito, de fato, não chegaram e elas não chegando, a nossa economia vai cair mais do que o que está projetado hoje”, disse. “E se o crédito não chegar, nossos problemas com o Judiciário serão maiores. Nós teremos mais problemas com as pequenas, médias e microempresas certamente”, acrescentou.

Maia disse também que a nova lei de recuperação judicial está pronta para ser votada. “Parece que o texto está muito bem organizado e acho que ela pode contribuir bastante. Se votou um projeto de algo emergencial, mas parece que o próprio texto da Câmara não foi, digamos assim o melhor, o próprio Senado não tratou da matéria”, contou.

Tratamento diferenciado entre trabalhador da iniciativa privada e servidor público

O ex-presidente da CNI Armando Monteiro Neto considera que a rigidez dos gastos públicos e a limitação que o Brasil enfrenta de não ter espaço para criar outras formas de arrecadação – em razão da já elevada carga tributária – colocam o país em um cenário em que só conseguirá resolver o quadro fiscal a partir do crescimento econômico.

“O Poder Judiciário tem papel fundamental, pois o Brasil precisará de investimentos privados. Na área de infraestrutura, o país tem uma atratividade natural, que exigirá segurança jurídica e um ambiente macroeconômico equilibrado. São contratos longos que exigem muita segurança jurídica”, destacou.

Ao fazer uma pergunta ao ministro do STF Luiz Fux, Armando Monteiro criticou o tratamento diferenciado dado a trabalhadores do setor público. “Ao setor privado todos os riscos da flutuação do mercado: a perda de emprego, a redução do salário – aliás a MP 936 foi sábia ao introduzir o mecanismo de flexibilização, porque a rigidez produz desemprego. Eu pergunto: E na esfera pública? Por que mesmo em meio a um quadro de tantas dificuldades que envolvem os entes subnacionais, como imaginar nesse cenário que não se possa fazer sequer acordos de redução de jornada no setor público e algum contingenciamento na transferência de recursos para os demais poderes”, questionou.

Luiz Fux disse que não há como tratar da mesma forma trabalhadores da iniciativa privada e servidores públicos, uma vez que, segundo ele, no setor privado é possível ter “três, cinco ou dez empregos”, enquanto no público só um. “Há uma distinção entre público e privado. O público só pode fazer aquilo que está previsto na lei. O privado pode fazer tudo, salvo o que não está previsto na lei”, opinou.

Ao longo do debate, Fux reconheceu a importância da segurança jurídica e de o Supremo apreciar com celeridade questões que envolvem a economia do país para formular teses jurídicas que possam ser seguidas por todo o Judiciário. “Ninguém vive sem previsibilidade”, afirmou. Ele contou que pretende usar a inteligência artificial para solucionar litígios judiciais que forem criados durante o período de pandemia. “Vamos ter plataforma de inteligência artificial para solução dos conflitos intersubjetivos”, adiantou.

No debate, o ministro do STJ Luís Felipe Salomão também reconheceu a importância da segurança jurídica para o país e disse, por exemplo, que em meio à pandemia é razoável que as empresas tenham redução de aluguel, bem como que haja diminuição do valor de cobranças de contratos educacionais.

Marcus Vinícius Furtado Coêlho apontou, por sua vez, que um dos problemas que causam insegurança jurídica no país é a divergência entre previsões para o Legislativo e Judiciário. “Se a Constituição Federal fala que a lei não pode retroagir para prejudicar ato jurídico perfeito, as decisões judiciais também não deveriam. A boa-fé deve ser sempre respeitada”, frisou. “A conciliação é uma saída para achatar a curva de demandas do Judiciário brasileiro. Mas a segurança jurídica é fundamental na construção dessas saídas”, emendou.

POLÍTICA FISCAL

BACEN. 30/06/2020. BC divulga Estatísticas Fiscais com os dados atualizados até maio de 2020.

1. Resultados fiscais

O setor público consolidado registrou déficit primário de R$131,4 bilhões em maio. O Governo Central e os governos regionais tiveram déficits respectivos de R$127,1 bilhões e de R$4,8 bilhões, e as empresas estatais, superávit de R$422 milhões. No ano, até maio, o déficit primário acumulado do setor público consolidado atingiu R$214,0 bilhões, ante superávit de R$7 bilhões no mesmo período do ano anterior, e no acumulado em doze meses o déficit primário atingiu R$282,9 bilhões (3,91% do PIB).

Os juros nominais do setor público consolidado, apropriados por competência, somaram R$9 bilhões em maio, comparativamente a R$34,5 bilhões no mesmo mês de 2019. Contribuíram para essa evolução as reduções na taxa Selic e no IPCA no período, além da trajetória favorável das operações de swap cambial (ganho de R$3,5 bilhões, em maio de 2020, ante perda de R$1,6 bilhão, no mesmo mês de 2019). Nos últimos doze meses, os juros nominais atingiram R$355,7 bilhões (4,91% do PIB), comparativamente a R$384,4 bilhões (5,46% do PIB) no acumulado até maio do ano anterior.

O resultado nominal do setor público consolidado, que inclui o resultado primário e os juros nominais apropriados, foi deficitário em R$140,4 bilhões em maio. No acumulado em 12 meses, o déficit nominal alcançou R$638,6 bilhões (8,82% do PIB), elevando-se 1,33 p.p. do PIB em relação ao déficit acumulado até abril.

2. Dívida Líquida do Setor Público (DLSP) e Dívida Bruta do Governo Geral (DBGG)

A DLSP alcançou R$3.983,4 bilhões (55,0% do PIB) em maio, aumento de 2,3 p.p. do PIB em relação ao mês anterior. Esse resultado refletiu, em especial, o impacto do déficit primário no mês (aumento de 1,8 p.p.), do efeito da variação do PIB nominal (aumento de 0,4 p.p.) e dos juros nominais apropriados (aumento de 0,1 p.p.). No ano, a relação DLSP/PIB reduziu-se 0,7 p.p., evolução decorrente, sobretudo, da desvalorização cambial acumulada de 34,6% (redução de 5,2 p.p.), do ajuste da paridade da cesta de moedas da dívida externa líquida (redução de 0,6 p.p.), do déficit primário acumulado (aumento de 3,0 p.p.) e dos juros nominais apropriados (aumento de 2,1 p.p.).

A DBGG – que compreende o Governo Federal, o INSS e os governos estaduais e municipais – alcançou R$5.929,1 bilhões em maio, equivalente a 81,9% do PIB, aumento de 2,1 p.p. do PIB em relação ao mês anterior. Essa evolução decorreu de emissões líquidas de dívida bruta (aumento de 1,3 p.p.), do efeito da variação do PIB nominal (aumento de 0,5 p.p.) e da incorporação de juros nominais (aumento de 0,3 p.p.). No ano, o aumento de 6,1 p.p. na relação DBGG/PIB decorreu das emissões líquidas de dívida (aumento de 2,5 p.p.), da incorporação de juros nominais (aumento de 1,9 p.p.), da desvalorização cambial acumulada (aumento de 1,6 p.p.), do efeito da variação do PIB nominal (aumento de 0,2 p.p.) e do ajuste da paridade da cesta de moedas da dívida externa (redução de 0,1 p.p.).

3. Elasticidades da DLSP e da DBGG

A tabela a seguir atualiza as elasticidades da DLSP e da DBGG a variações na taxa de câmbio, na taxa de juros e nos índices de preços para o mês de maio.

DOCUMENTO: https://www.bcb.gov.br/content/estatisticas/docs_estatisticasfiscais/Nota%20para%20a%20Imprensa%20-%20Estat%C3%ADsticas%20Fiscais.pdf

IPEA. 30/06/2020. Ipea prevê crescimento da dívida pública e redução de margem fiscal. Análise trimestral destaca necessidade de disciplina fiscal e reformas

A deterioração fiscal causada pela pandemia de Covid-19 pode fazer com que a proporção da dívida bruta do governo federal em relação ao PIB passe de 75,8% no final de 2019 para 93,7% no final de 2020. De acordo com o Instituto de Pesquisa Econômica Aplicada (Ipea), o impacto pode ser ainda maior caso os atuais programas emergenciais de apoio à economia sejam estendidos além do tempo previsto. As previsões estão na análise trimestral de conjuntura econômica, divulgada nesta terça-feira, 30.

O documento, chamado de Visão Geral da Conjuntura, traz projeções das despesas fiscais nos próximos anos e conclui que, em 2023, o espaço fiscal - que indica quanto o governo pode gastar com despesas discricionárias - atingiria nível equivalente a 64% do valor estimado para 2020, em termos reais – já descontada a inflação. Isso colocaria em risco o funcionamento da máquina pública e a continuidade de diversas políticas sociais, e reforça a importância de medidas voltadas para a contenção dos gastos obrigatórios.

No que diz respeito ao endividamento público, a análise mostra duas possíveis trajetórias. Os cenários se diferenciam pelo ritmo de crescimento do PIB nos próximos anos, mas ambos pressupõem esforço fiscal compatível com a manutenção do teto de gastos até 2036. Os resultados mostram que, no cenário de crescimento mais baixo, a disciplina fiscal seria capaz de estabilizar a razão dívida-PIB e fazê-la cair gradualmente a partir de 2029, mas deixaria o país vulnerável a choques adversos durante longo período de tempo. Já no cenário caracterizado por crescimento mais elevado, a dívida em proporção do PIB diminuiria a partir de 2022 e convergiria mais rapidamente para patamares menos arriscados. A recomendação é a combinação de disciplina fiscal com um conjunto de medidas e reformas que aumentem a eficiência e a produtividade na economia brasileira.

As previsões macroeconômicas para 2020 e 2021 divulgadas no início de junho estão mantidas: queda de 6% no Produto Interno Bruto (PIB) para 2020 e alta de 3,6% para 2021. Apesar da projeção de queda de 10,5% no segundo trimestre do ano corrente, há expectativa de retomada da atividade econômica nos próximos trimestres. O mês de abril foi considerado o fundo do poço devido às quedas em relação ao mês de março na indústria (-18,8%), no comércio (-17,5%) e nos serviços (-11,7%), de acordo com pesquisas mensais do IBGE.

Visão geral da conjuntura

Por José Ronaldo de C. Souza Júnior, Marco A. F. H. Cavalcanti e Paulo Mansur Levy

Esta seção apresenta uma análise da conjuntura econômica internacional e brasileira por meio de um amplo conjunto de indicadores e projeções. A despeito da forte redução da atividade econômica observada no final de março e ao longo de abril, vários indicadores apontam no sentido de que a atividade econômica voltou a crescer a partir de maio. Um fator importante para essa recuperação é a implementação efetiva do auxílio emergencial, que parece ter coberto parcela substancial da renda dos trabalhadores informais e em condição de vulnerabilidade. Sob a hipótese de que o processo de flexibilização gradual das restrições à mobilidade e ao funcionamento das atividades econômicas iniciado em junho se manterá, projeta-se a recuperação gradual do PIB no terceiro e quarto trimestres. A queda projetada para o ano é de 6%, mas a trajetória de recuperação no segundo semestre deixará um carry-over de quase 2% para 2021, cujo crescimento projetado é de 3,6%.

A pandemia interrompeu temporariamente o processo de consolidação fiscal pelo qual passava a economia brasileira. Durante o período de crise sanitária e econômica, a prioridade passou a ser, evidentemente, a proteção da vida e da saúde das pessoas, bem como a preservação de empregos, renda e empresas. Assim, o governo lançou um amplo conjunto de medidas emergenciais de apoio à saúde e à economia, muitas das quais envolvem um custo fiscal significativo, tanto pelo lado da despesa como pelo lado da receita. Espera-se que, em função da deterioração fiscal causada pela pandemia, a dívida bruta do governo geral (DBGG) em proporção do PIB aumente de 75,8% no final de 2019 para 93,7% no final de 2020. Apesar da expectativa de que as medidas emergenciais não se estendam além de 2020, a crise da Covid-19 aumentou também para o futuro os desafios fiscais do país, que sairá da crise com uma dívida pública muito mais alta, e níveis de produção e arrecadação muito mais baixos que antes. Logo, o esforço fiscal que vinha sendo realizado terá que ser reforçado, visando reafirmar o compromisso com o equilíbrio das contas públicas e com uma trajetória sustentável para a dívida pública.

DOCUMENTO: https://www.ipea.gov.br/portal/images/stories/PDFs/conjuntura/200630_cc_47_visao_geral.pdf

MEconomia. 30/06/2020. PRISMA FISCAL. Mercado estima crescimento de 26% na despesa primária do governo central para 2020. Analistas demonstram confiança de que as medidas fiscais emergenciais ficarão restritas a este ano

A Secretaria de Política Econômica do Ministério da Economia (SPE/ME) publicou nesta terça-feira (30/6) a “Nota Informativa - Prisma Fiscal/SPE - Expectativa da Despesa Total do Governo Central para o período 2021 a 2023”. O texto destaca que, para o mercado, as despesas primárias do governo central em 2020 devem crescer 26% em comparação com 2019.

A nota ressalta que, desde abril, a despesa total esperada para o próximo triênio (2021, 2022 e 2023) vem sendo reduzida, indicando que, para os analistas, as medidas fiscais emergenciais ficarão restritas a 2020.

“A manutenção da confiança do mercado em um período tão atípico de nossa história, reflete a solidez conquistada pela equipe econômica liderada pelo ministro Paulo Guedes. O governo sempre foi claro e objetivo em suas declarações e ações. Não há espaço para o desrespeito às regras fiscais.”

O estudo destaca ainda que, mesmo com o impacto fiscal decorrente das ações do governo no enfrentamento à pandemia, o mercado continua a demonstrar confiança de que o processo de consolidação fiscal será mantido em médio e longo prazos por meio da contenção dos gastos públicos e da manutenção do Teto de Gastos.

Prisma Fiscal

O Prisma Fiscal é um sistema de coleta de expectativas de mercado elaborado pela SPE para acompanhar a evolução das principais variáveis fiscais brasileiras: arrecadação das receitas federais, receita líquida do governo central, despesa total do governo central, resultado primário do governo central e dívida bruta do governo geral.

Ele oferece uma oportunidade para o aprimoramento dos estudos fiscais no país, além de facilitar o controle social a partir de uma ancoragem das expectativas quanto ao desempenho destas variáveis.

DOCUMENTO: https://www.gov.br/economia/pt-br/centrais-de-conteudo/publicacoes/notas-informativas/2020/ni-despesa-prisma_junho-2020-5a-versao-1.pdf/view

INVESTIMENTO

MEconomia. 30/06/2020. FINANCIAMENTO. Cofiex aprova cerca de US$ 790 milhões em recursos externos para projetos no Brasil. Operações vão beneficiar programas de defesa do setor produtivo e do emprego, do BNDES e do Bandes, além da área de saneamento básico do Ceará

A Comissão de Financiamentos Externos (Cofiex) do Ministério da Economia aprovou o início da preparação de projetos financiados com recursos externos de bancos multilaterais de desenvolvimento, no valor de US$ 780 milhões e € 7 milhões. As operações vão beneficiar três projetos, nas áreas de saneamento básico em comunidades rurais e setor produtivo, em especial micro, pequenas e médias empresas (MPMEs).

O maior volume de recursos, US$ 750 milhões, será para o Programa Global de Crédito Emergencial BID-BNDES, de Financiamento às MPMEs para a Defesa do Setor Produtivo e o Emprego. O valor será financiado pelo Banco Interamericano de Desenvolvimento (BID) e terá abrangência nacional.

Também com recursos do BID, o Banco de Desenvolvimento do Espírito Santo (Bandes) vai obter US$ 30 milhões para ações do Programa Global de Crédito para a Defesa do Setor Produtivo e o Emprego naquele estado.

Outro projeto é de caráter não-reembolsável, com € 7 milhões em recursos da União Europeia. O financiamento, via KfW Bankengruppe, banco estatal de fomento alemão, vai ser destinado a ações complementares do Programa Águas do Sertão, no Ceará.

Agilidade na decisão

Os projetos foram submetidos aos membros do colegiado por meio de consulta eletrônica, de acordo com os novos procedimentos da Cofiex, previstos na Resolução nº 2, de 13 de abril de 2020. O novo formato de avaliação das propostas leva em consideração o caráter extraordinário do estado de calamidade pública causada pela pandemia do novo coronavírus, a fim de agilizar a decisão da comissão.

A Cofiex é um órgão colegiado integrante da estrutura organizacional do Ministério da Economia, composta por representantes dos ministérios da Economia e das Relações Exteriores. A aprovação na Cofiex é a primeira etapa para a obtenção dos financiamentos externos com a garantia da União.

SERVIÇOS

FGV. IBRE. 30/06/2020. Confiança de Serviços reage positivamente pelo 2° mês consecutivo depois de fortes quedas no início da pandemia

O Índice de Confiança de Serviços (ICS), da Fundação Getulio Vargas, subiu 11,2 pontos em junho, para 71,7 pontos. Apesar de ter acumulado 20,6 pontos nos últimos dois meses, o índice recupera apenas 48% das perdas sofridas no bimestre março-abril desse ano.

“A confiança de serviços reage positivamente pelo segundo mês consecutivo depois de fortes quedas no início da pandemia. Apesar da expressiva alta de junho, é preciso cautela porque a base de comparação é muito baixa. Outro ponto a ser considerado é a dinâmica dessa recuperação, ainda muito mais influenciada pela melhora das expectativas com os próximos meses. O pior momento parece estar ficando para trás, mas a elevada incerteza deixa o cenário de retomada ainda sem precisão”, avaliou Rodolpho Tobler, economista da FGV IBRE.

Houve variação positiva do ICS nos 13 segmentos pesquisados, com uma melhora razoável, porém ainda menor das avaliações sobre o momento atual e um novo avanço consistente das expectativas em relação aos próximos meses. O Índice de Situação Atual (ISA-S) subiu 7,0 pontos, para 64,0 pontos, ainda assim fechando o semestre com perda de 28,9 pontos no ano. O Índice de Expectativas (IE-S) cresceu 15,1 pontos, para 79,8 pontos, e mesmo acumulando 32,5 pontos de crescimento nos meses de maio e junho, isso não foi suficiente para retornar ainda ao nível pré-pandemia.

O Nível de Utilização da Capacidade Instalada (NUCI) do setor de serviços diminuiu 0,8 ponto percentual para 77,2%, atingindo um novo mínimo histórico da série iniciada em abril de 2013. Contudo, a queda nesse mês foi inferior às apresentadas em abril (-3,5 p.p.) e em maio (-1,5 p.p.).

Apesar de encerrar o semestre em alta, setor de Serviços fecha primeira metade do ano em baixa

Embora a confiança das empresas que prestam serviços ter aumentado consideravelmente nos últimos dois meses, o resultado geral do setor foi negativo nos dois primeiros trimestres do ano, em especial o 2° trimestre onde foi registrado a maior queda trimestral da série iniciada em 2008. O resultado bastante negativo também foi disseminado em todos os grandes segmentos do setor. A recuperação dos dados mensais mostra que o terceiro trimestre pode ser menos negativo do que se observou neste último trimestre.

DOCUMENTO: https://portalibre.fgv.br/noticias/confianca-de-servicos-reage-positivamente-pelo-2deg-mes-consecutivo-depois-de-fortes

CULTURA