US ECONOMICS

FED. December 13, 2017. Federal Reserve issues FOMC statement

Information received since the Federal Open Market Committee met in November indicates that the labor market has continued to strengthen and that economic activity has been rising at a solid rate. Averaging through hurricane-related fluctuations, job gains have been solid, and the unemployment rate declined further. Household spending has been expanding at a moderate rate, and growth in business fixed investment has picked up in recent quarters. On a 12-month basis, both overall inflation and inflation for items other than food and energy have declined this year and are running below 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed, on balance.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. Hurricane-related disruptions and rebuilding have affected economic activity, employment, and inflation in recent months but have not materially altered the outlook for the national economy. Consequently, the Committee continues to expect that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace and labor market conditions will remain strong. Inflation on a 12‑month basis is expected to remain somewhat below 2 percent in the near term but to stabilize around the Committee's 2 percent objective over the medium term. Near-term risks to the economic outlook appear roughly balanced, but the Committee is monitoring inflation developments closely.

In view of realized and expected labor market conditions and inflation, the Committee decided to raise the target range for the federal funds rate to 1-1/4 to 1‑1/2 percent. The stance of monetary policy remains accommodative, thereby supporting strong labor market conditions and a sustained return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. The Committee will carefully monitor actual and expected inflation developments relative to its symmetric inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

Voting for the FOMC monetary policy action were Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; Patrick Harker; Robert S. Kaplan; Jerome H. Powell; and Randal K. Quarles. Voting against the action were Charles L. Evans and Neel Kashkari, who preferred at this meeting to maintain the existing target range for the federal funds rate.

Implementation Note issued December 13, 2017

Decisions Regarding Monetary Policy Implementation

The Federal Reserve has made the following decisions to implement the monetary policy stance announced by the Federal Open Market Committee in its statement on December 13, 2017:

- The Board of Governors of the Federal Reserve System voted unanimously to raise the interest rate paid on required and excess reserve balances to 1.50 percent, effective December 14, 2017.

- As part of its policy decision, the Federal Open Market Committee voted to authorize and direct the Open Market Desk at the Federal Reserve Bank of New York, until instructed otherwise, to execute transactions in the System Open Market Account in accordance with the following domestic policy directive:"Effective December 14, 2017, the Federal Open Market Committee directs the Desk to undertake open market operations as necessary to maintain the federal funds rate in a target range of 1-1/4 to 1-1/2 percent, including overnight reverse repurchase operations (and reverse repurchase operations with maturities of more than one day when necessary to accommodate weekend, holiday, or similar trading conventions) at an offering rate of 1.25 percent, in amounts limited only by the value of Treasury securities held outright in the System Open Market Account that are available for such operations and by a per-counterparty limit of $30 billion per day.The Committee directs the Desk to continue rolling over at auction the amount of principal payments from the Federal Reserve's holdings of Treasury securities maturing during December that exceeds $6 billion, and to continue reinvesting in agency mortgage-backed securities the amount of principal payments from the Federal Reserve's holdings of agency debt and agency mortgage-backed securities received during December that exceeds $4 billion. Effective in January, the Committee directs the Desk to roll over at auction the amount of principal payments from the Federal Reserve's holdings of Treasury securities maturing during each calendar month that exceeds $12 billion, and to reinvest in agency mortgage-backed securities the amount of principal payments from the Federal Reserve's holdings of agency debt and agency mortgage-backed securities received during each calendar month that exceeds $8 billion. Small deviations from these amounts for operational reasons are acceptable.The Committee also directs the Desk to engage in dollar roll and coupon swap transactions as necessary to facilitate settlement of the Federal Reserve's agency mortgage-backed securities transactions."

- In a related action, the Board of Governors of the Federal Reserve System voted unanimously to approve a 1/4 percentage point increase in the primary credit rate to 2.00 percent, effective December 14, 2017. In taking this action, the Board approved requests to establish that rate submitted by the Boards of Directors of the Federal Reserve Banks of Boston, New York, Philadelphia, Cleveland, Richmond, Atlanta, Kansas City, Dallas, and San Francisco.

This information will be updated as appropriate to reflect decisions of the Federal Open Market Committee or the Board of Governors regarding details of the Federal Reserve's operational tools and approach used to implement monetary policy.

FULL DOCUMENT: https://www.federalreserve.gov/monetarypolicy/files/monetary20171213a1.pdf

FED. December 13, 2017. Federal Reserve Board and Federal Open Market Committee release economic projections from the December 12-13 FOMC meeting

The attached table and charts released on Wednesday summarize the economic projections and the target federal funds rate projections made by Federal Open Market Committee participants for the December 12-13 meeting.

The table will be incorporated into a summary of economic projections released with the minutes of the December 12-13 meeting. Summaries of economic projections are released quarterly.

Projections: https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20171213.pdf

FED. REUTERS. DECEMBER 13, 2017. Fed raises interest rates, keeps 2018 policy outlook unchanged

Howard Schneider, Lindsay Dunsmuir

WASHINGTON (Reuters) - The Federal Reserve raised interest rates by a quarter of a percentage point on Wednesday, as anticipated, but left its rate outlook for the coming years unchanged even as policymakers projected a short-term acceleration in U.S. economic growth.

The move, coming at the final policy meeting of 2017 and on the heels of a flurry of relatively bullish economic data, represented a victory for a central bank that has vowed to continue a gradual tightening of monetary policy.

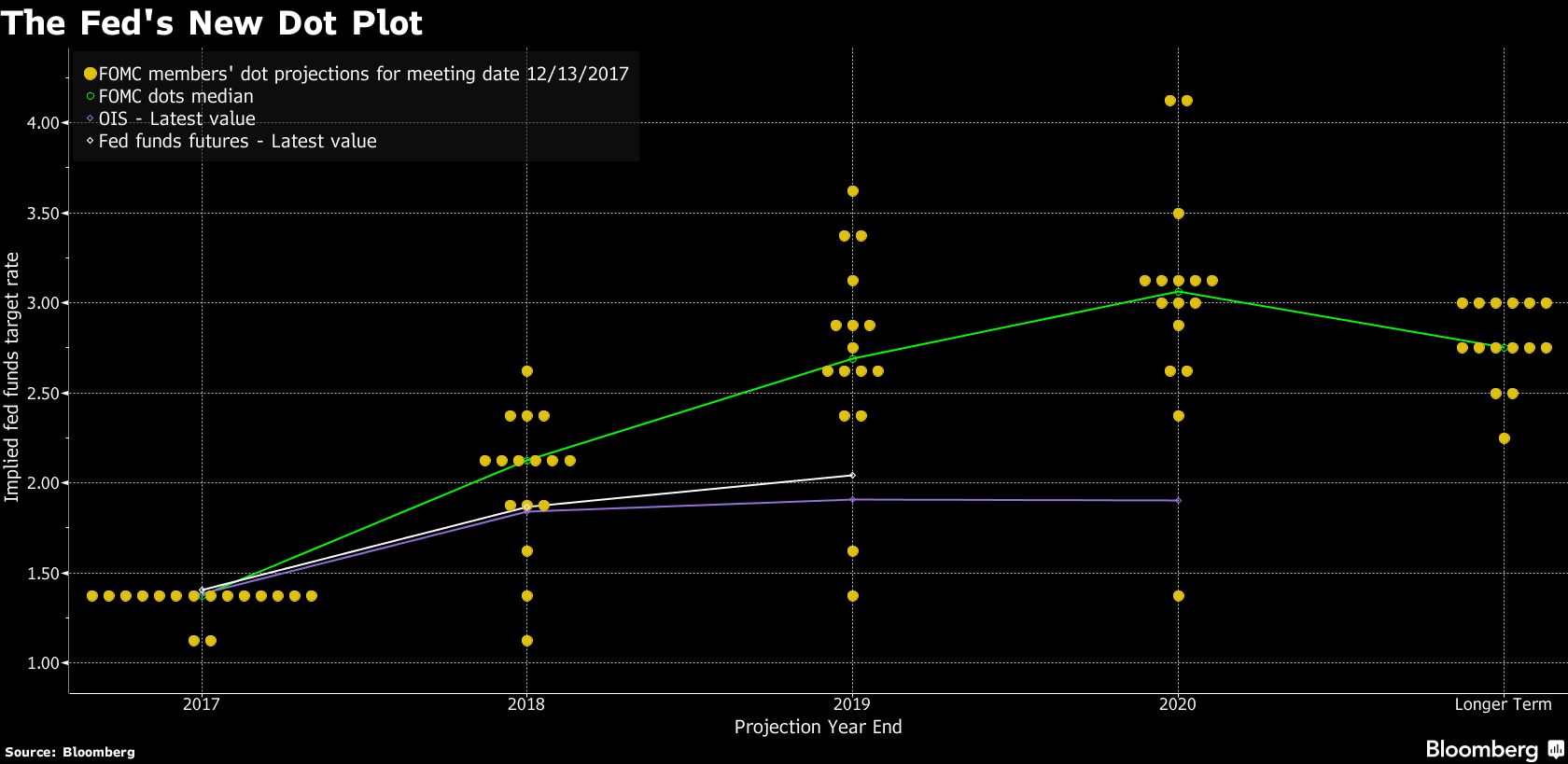

Having raised its benchmark overnight lending rate three times this year, the Fed projected three more hikes in each of 2018 and 2019 before a long-run level of 2.8 percent is reached. That is unchanged from the last round of forecasts in September.

“Economic activity has been rising at a solid rate ... job gains have been solid,” the Fed’s policy-setting committee said in a statement announcing the federal funds rate had been lifted to a target range of 1.25 percent to 1.50 percent.

U.S. stocks extended their gains after the release of the policy statement, while Treasury yields dropped to session lows.

Fed Chair Janet Yellen is due to hold a press conference at 2:30 p.m. ET (1930 GMT).

INFLATION CONCERNS

Fed officials acknowledged in their latest forecasts that the economy had gained steam in 2017 by raising their economic growth forecasts and lowering the expected unemployment rate for the coming years.

Gross domestic product is expected to grow 2.5 percent in 2018, up from the 2.1 percent forecast in September, while the unemployment rate is seen falling to 3.9 percent next year, compared to 4.1 percent in the last set of projections.

But inflation is projected to remain shy of the Fed’s 2 percent goal for another year, with weakness on that front remaining enough of a concern that policymakers saw no reason to accelerate the expected pace of rate increases.

That means that the Trump administration’s tax overhaul, if passed by Congress, would take effect without the central bank having flagged any likely response in the form of higher rates or concerns of a jump in inflation.

“It shows at least some members of the Fed don’t see any reason to keep hiking rates in an environment where the economy is growing more strongly but certainly not overheating and where inflation hasn’t become a problem and doesn’t look like it is going to be one,” said Kate Warne, investment strategist at Edward Jones.

Policymakers do see the federal funds rate rising to 3.1 percent in 2020, slightly above the 2.8 percent “neutral” rate they expect to maintain in the long run. That indicates possible concerns about a rise in inflation pressures over time.

As it stands, inflation is expected to remain below the Fed’s target in the near term and is being monitored “closely” by policymakers.

Chicago Fed President Charles Evans and Minneapolis Fed President Neel Kashkari dissented in the policy statement on Wednesday.

The Fed also said that, as of January, it would raise the amount of Treasury bonds and mortgage-backed securities that it would not reinvest on a monthly basis to $12 billion and $8 billion, respectively. That is consistent with its balance sheet reduction plan.

Reporting by Howard Schneider; Editing by David Chance and Paul Simao

BLOOMBERG. 13 December 2017. Fed Raises Rates, Eyes Three 2018 Hikes as Yellen Era Nears End

By Christopher Condon and Craig Torres

- Central bank expects labor market to ‘remain strong’

- Kashkari, Evans dissent, preferring to leave rates unchanged

- Fed Raises Rates and Still Sees Three Hikes in 2018

Federal Reserve officials followed through on an expected interest-rate increase and raised their forecast for economic growth in 2018, even as they stuck with a projection for three hikes in the coming year.

“This change highlights that the committee expects the labor market to remain strong, with sustained job creation, ample opportunities for workers and rising wages,” Chair Janet Yellen told reporters Wednesday in Washington following the decision. In her final scheduled press conference before before stepping down on Feb. 3, Yellen also said she would do her utmost to ensure a smooth transition to her nominated successor, Jerome Powell.

In a key change to its statement announcing the decision, the Federal Open Market Committee omitted prior language saying it expected the labor market would strengthen further. Instead, Wednesday’s missive said monetary policy would help the labor market “remain strong.” That suggests Fed officials expect improvement in the job market to slow.

The yield on 10-year U.S. Treasury notes fell after the Fed announcement, as did the Bloomberg Dollar Spot Index. Trading at record highs recently, stocks jumped after the Fed’s announcement before paring gains. Asked during a press conference about rising asset prices, Yellen said the high valuations don’t necessarily mean that they’re overvalued and that she’s not seeing a worrisome buildup of leverage or credit.

The 7-2 vote for the rate move, the Fed’s third this year, raises the benchmark lending rate by a quarter percentage point to a target range of 1.25 percent to 1.5 percent. In another move that could tighten monetary conditions, the Fed confirmed that it would step up the monthly pace of shrinking its balance sheet, as scheduled, to $20 billion beginning in January from $10 billion.

Through the policy adjustments and the statement, the Fed continued to seek a delicate balance between responding to positive news on growth and unemployment that encouraged gradual tightening, while signaling caution due to persistently weak inflation readings that have befuddled policy makers.

That puzzle continued earlier Wednesday when Labor Department data showed consumer inflation, excluding food and energy, was lower than expected at 1.7 percent in the 12 months through November.

Inflation Developments

“Hurricane-related disruptions and rebuilding have affected economic activity, employment and inflation in recent months but have not materially altered the outlook for the national economy,” the Fed said. Repeating language used since June, the FOMC said that “near-term risks to the economic outlook appear roughly balanced, but the committee is monitoring inflation developments closely.”

In the latest set of quarterly forecasts released Wednesday, the median estimate for economic growth next year jumped to 2.5 percent from 2.1 percent. It wasn’t immediately clear how much of the change reflected confidence that the tax-cut legislation moving through Congress will boost growth, or other factors such as pickups in business spending and global growth.

At the same time, the committee’s median forecast for long-run expansion was unchanged at 1.8 percent, suggesting officials aren’t yet convinced the tax package will significantly affect the economy’s capacity for growth.

Minneapolis Fed President Neel Kashkari and the Chicago Fed’s Charles Evans both dissented against the interest-rate decision, preferring to leave them unchanged. It was the first meeting with more than one dissent since November 2016; Kashkari’s dissent was his third this year. Evans dissented for the first time since 2011.

WHAT OUR ECONOMISTS SAY:

“The most important takeaway from the December FOMC meeting is that even though policy makers are becoming more bullish on economic prospects, they are not shifting to a more hawkish policy stance. An extended inflation soft patch is giving the Powell-Fed a free pass to continue along Janet Yellen’s gradualist path toward policy normalization.”

-- Carl Riccadonna and Yelena Shulyatyeva, Bloomberg Economics.

That follows a solid rebound for the expansion since a disappointing start to 2017. Gross domestic product grew at more than a 3 percent annualized pace in both the second and third quarters, and is on track to expand in the fourth quarter by 2.9 percent, according to the Atlanta Fed’s GDPNow tracking estimate.

Rate Path

Despite the upgrade in near-term growth expectations, policy makers left the number of hikes projected for 2018 effectively unchanged. The median forecast pegged the federal funds rate at 2.1 percent at the end of next year.

That could, in part, reflect lingering concerns over sluggish wage and price gains. The Fed’s preferred gauge of inflation, based on consumer spending, gained just 1.6 percent in the year through October.

Weighed against unemployment, which has dropped to a 16-year low at 4.1 percent, that weakness has puzzled economists and made some policy makers declare the Fed should hold off on additional rate increases until prices respond more briskly.

The committee lowered its median estimate for the unemployment rate, expecting it to hit 3.9 percent by the end of 2018, compared with a September projection of 4.1 percent.

The committee left its median estimate for the lowest sustainable level of long-run unemployment at 4.6 percent, suggesting that officials still expect the drop in joblessness to eventually boost inflation. Forecasts showed little change in the inflation outlook over the next three years.

Yellen is expected to chair the committee’s next meeting on Jan. 30-31 for what will be her last FOMC gathering of her time on the committee spanning three decades as chair, vice chair, San Francisco Fed president and governor.

Other Details of Projections

- Median estimate for 2019 federal funds rate held at 2.7 percent; 2020 projection rose to 3.1 percent from 2.9 percent, while long-run rate remained at 2.8 percent

- Median inflation forecasts all unchanged except for 2017 headline PCE forecast, which rose to 1.7 percent from 1.6 percent

- 2019 median economic-growth forecast rose to 2.1 percent from 2 percent; 2020 projection moved to 2 percent from 1.8 percent

- Median 2019 unemployment-rate projection fell to 3.9 percent from 4.1 percent; 2020 estimate declined to 4 percent from 4.2 percent

— With assistance by Matthew Boesler, Jeanna Smialek, and Steve Matthews

________________

LGCJ.: