CANADA ECONOMICS

Consumer Price Index

StatCan. 2017-06-23. Consumer Price Index, May 2017

Consumer Price Index

May 2017

1.3% increase

(12-month change)

Source(s): CANSIM table 326-0020.

The Consumer Price Index (CPI) rose 1.3% on a year-over-year basis in May, following a 1.6% gain in April.

Overall, energy prices rose less year over year in May than they did in April, with the year-over-year growth rate in gasoline prices slowing to half of what it was the previous month. Declines in food prices continued to moderate.

Excluding food and energy, the CPI was up 1.4% on a year-over-year basis in May, after posting a 1.5% increase in April.

Chart 1 Chart 1: The 12-month change in the Consumer Price Index (CPI) and the CPI excluding food and energy

The 12-month change in the Consumer Price Index (CPI) and the CPI excluding food and energy

12-month change in the major components

Prices were up in six of the eight major components in the 12 months to May, with the shelter and transportation indexes contributing the most to the year-over-year rise in the CPI. The clothing and footwear index and the food index declined on a year-over-year basis.

Chart 2 Chart 2: Consumer prices increase in six of the eight major components

Consumer prices increase in six of the eight major components

Shelter costs grew 1.9% in May on a year-over-year basis, after increasing 2.2% in April. This deceleration was led by the electricity index (-5.5%), which declined year over year for a fifth consecutive month. On a monthly basis, electricity prices were down 3.3% in May, led by declines in Ontario. On a year-over-year basis, the natural gas index rose less in May than in April. Conversely, homeowners' replacement costs were up more in May (+4.4%) than in April (+3.9%).

The transportation index rose 2.2% over the 12-month period ending in May, compared with 4.2% in April. Gasoline prices contributed the most to this deceleration, up 6.8% on a year-over-year basis in May, after a 15.9% gain in April. The purchase of passenger vehicles index edged up 0.2% in the 12 months to May, marking its smallest year-over-year increase since February 2015. At the same time, the price of air transportation rose more in the 12-month period to May than in April.

The recreation, education and reading index rose 2.5% in the 12 months to May, following a 3.3% increase in April. The travel tours index was up 6.8% year over year in May, after a 9.4% increase in April. Prices for video equipment fell more on a year-over-year basis in May than in April. At the same time, the traveller accommodation index rose 6.3% over the 12-month period ending in May, following a 5.7% increase in April.

In May, the food index was down 0.1% on a year-over-year basis, following a 1.1% decline in April. Prices for food purchased from stores decreased 1.2% year over year in May, with the meat and bakery products indexes contributing the most to the drop. The decline in fresh fruit prices (-1.0%) slowed in May, following a 6.2% decrease in April. Prices for fresh vegetables rose year over year for the first time since August 2016. Meanwhile, prices for food purchased from restaurants posted a 2.4% increase in the 12 months to May.

12-month change in the provinces

Year over year, consumer prices rose less in May than in April in all provinces. Growth in the CPI decelerated most in Manitoba, while the smallest deceleration in the growth of prices occurred in Quebec.

Chart 3 Chart 3: Consumer prices rise at a slower rate in all provinces

Consumer prices rise at a slower rate in all provinces

The CPI in Manitoba was up 1.0% year over year in May, following a 1.6% increase in April. The gasoline index registered a 0.9% decline in the 12 months to May, following an increase of 12.5% in April. Manitoba was the only province to post a year-over-year decline in gasoline prices. Natural gas prices in the province fell 4.9% in the 12-month period ending in May, providing the largest downward contribution to the natural gas index at the national level. At the same time, passenger vehicle insurance premiums rose 3.4% over the course of the year ending in May.

Consumer prices in Ontario rose 1.4% in the 12 months to May, after a 1.9% increase in April. Electricity prices declined 16.1% year over year in May, partly reflecting decreases in the time-of-use rates. Among the provinces, the cost of women's clothing fell the most in Ontario, declining 5.0% in the 12-month period ending in May. At the same time, the homeowners' replacement cost index registered a 7.9% year-over-year increase in May, the largest gain among the provinces, following a 6.8% increase in April.

In Quebec, consumer prices rose 0.7% year over year in May, following a 0.8% increase in April. The Internet access services index fell 11.7% in the 12-month period ending in May, the largest decline among the provinces. In contrast, fresh vegetable prices increased more in Quebec than in any other province on a year-over-year basis in May.

Seasonally adjusted monthly Consumer Price Index

On a seasonally adjusted monthly basis, the CPI fell 0.2% in May, after rising 0.4% in April.

Chart 4 Chart 4: Seasonally adjusted monthly Consumer Price Index

Seasonally adjusted monthly Consumer Price Index

Four major components decreased on a seasonally adjusted monthly basis in May, while four increased.

On a seasonally adjusted monthly basis in May, the transportation index (-1.1%) posted the largest decline, while the clothing and footwear index (+0.6%) recorded the largest gain.

Chart 5 Chart 5: The gasoline index, annual average, Canada, 1950 to 2016

The gasoline index, annual average, Canada, 1950 to 2016

FULL DOCUMENT: http://www.statcan.gc.ca/daily-quotidien/170623/dq170623a-eng.pdf

REUTERS. Jun 23, 2017. Canada inflation rate cools in May, making July rate hike less likely

By Leah Schnurr

OTTAWA (Reuters) - Canada's annual inflation rate cooled more than expected in May, moving it further away from the Bank of Canada's target and reducing the odds of an interest rate hike next month.

The annual inflation rate declined to 1.3 percent from April's 1.6 percent, Statistics Canada said on Friday, the lowest level since November 2016 and below forecasts for 1.5 percent.

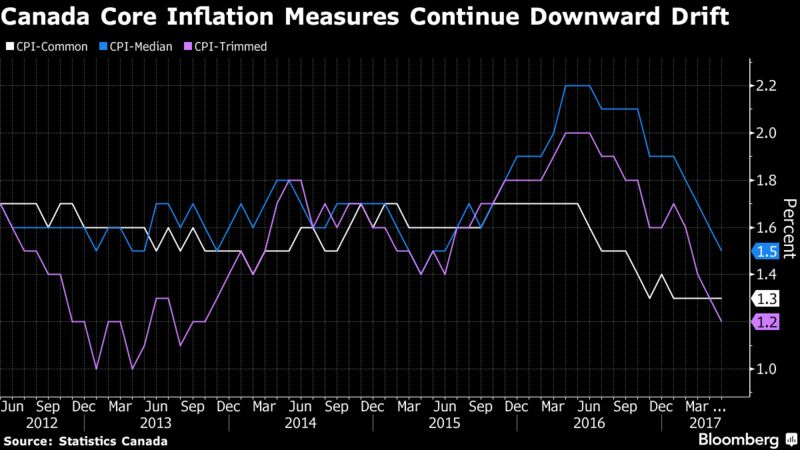

The three measures of core inflation the Bank of Canada set last year remained subdued, with two of them declining.

Economists said the figures give the central bank room to hold off on raising interest rates at its next meeting in July after hawkish comments from two top policymakers last week set the stage for hikes sooner than had been anticipated.

"When we're looking for reasons for the bank to take its time in raising rates, core inflation has been exhibit A," said Doug Porter, chief economist at Bank of Montreal.

"Certainly very modest core inflation continues to rumble in the background as a pretty strong reason for the bank not to rush the proceedings. That story was just pounded home today."

The Canadian dollar weakened against the greenback, while markets reduced the likelihood of a July hike to 22 percent from 34.8 percent before the report was released. [CAD/]

Nonetheless, a hike by the end of the year is nearly fully priced in, suggesting markets do not expect weak inflation to delay the bank for long.

The bank, which has an inflation target of 2 percent, has held rates at 0.50 percent since 2015 when it cut borrowing costs twice to offset the hit from cheaper oil.

CPI common, which the central bank says is the best gauge of the economy's underperformance, held at 1.3 percent. CPI median, which shows the median inflation rate across CPI components, declined to 1.5 percent, while CPI trim, which excludes upside and downside outliers, dipped to 1.2 percent.

Food prices fell on an annual basis for the eighth month in a row, down 0.1 percent as consumers paid less for meat and fresh fruit.

Still, food price declines have been moderating in recent months and the cost of fresh vegetables rose for the first time since August 2016.

Gasoline prices were up 6.8 percent, slowing significantly from April's 15.9 percent annual increase. Shelter costs also moderated as electricity prices fell, particularly in Ontario, where the provincial government has introduced measures to alleviate high electricity costs.

(Additional reporting by Susan Taylor in Toronto; Editing by Chizu Nomiyama, Bernard Orr)

BLOOMBERG. 2017 M06 23. Canadian Core Inflation Slows to Lowest Since 1999

By Theophilos Argitis

- Sluggish inflation will test Bank of Canada’s rate hike talk

- Consumer price index rose 1.3 percent in May from year ago

Canadian inflation continued to ease in May, with a key gauge of price pressures at the lowest since 1999, a trend that will challenge the Bank of Canada’s recent efforts to set the stage for a rate increase.

The consumer price index rose 1.3 percent in May from a year ago, down from an annual pace of 1.6 percent in April, Statistics Canada reported Friday from Ottawa.

Measures of annual core inflation, a key indicator tracked by the Bank of Canada that excludes volatile components such as gasoline, fell to the lowest in almost two decades. The average of the central bank’s three core measures declined to 1.3 percent, the lowest since March 1999.

Key Points

- The Bank of Canada last week began to play down sluggish inflation numbers, suggesting they were simply capturing the lagged effects of past excess capacity. But the numbers are below their forecasts. Inflation for the first two months of the second quarter is averaging 1.5 percent, versus Bank of Canada forecasts of 1.7 percent.

- Economists surveyed by Bloomberg had forecast inflation would slow to 1.5 percent from 1.6 percent in April on lower gasoline prices.

- Prices rose 0.1 percent on a monthly basis, lagging the 0.2 percent median economist forecast.

- The Bank of Canada’s ‘common’ core rate was 1.3 percent in May, the ‘median’ core rate was 1.5 percent and the ‘trim’ measure was 1.2 percent.

- Recent changes in electricity policy in Ontario seems to be having an impact. Electricity prices in that province were down 16.1 percent year over year in May, bringing inflation down in Ontario to 1.4 percent from 1.9 percent in April.

Big Picture

Inflation is important to the central bank since its mandate is to target inflation at 2 percent, an objective it has largely failed to deliver on over the past five years. When it talks about being less concerned about inflation, the Bank of Canada gives itself more leeway to talk about hiking interest rates, as it’s started do.

Other Details

- On a seasonally adjusted basis, consumer prices fell 0.2 percent in May.

- Gasoline prices fell 4 percent in May. Year-over-year, gasoline prices were up 6.8 percent. That’s down from a 15.9 percent increase in April.

- The gap between goods and services inflation is widening. Price increases for services were 2.3 percent in May, compared with 0.1 percent for goods. The difference between the two rates was the widest since 2015.

What Economists Say

Nick Exarhos, CIBC Economics: Services inflation “is a better indicator of domestic slack, and where underlying inflation trends are heading. All told, a softer indicator on CPI, but something the market has gotten used to, and the trend in crude may be more instructive over the coming weeks for the path of inflation breakevens.”

ECONOMY

Department of Finance Canada. June 22, 2017. Government's Plan to Build a Strong Middle Class Receives Royal Assent

Ottawa, Ontario – The Canadian economy is growing stronger, creating more opportunities for Canada's middle class. Budget 2017 is the next phase in the Government's ambitious plan to give every Canadian the chance to succeed in the new economy and be part of a strong middle class.

Finance Minister Bill Morneau today welcomed Royal Assent of the Budget Implementation Act, 2017, No. 1, which implements many of Budget 2017's measures, including preparing Canadians for the jobs of the future, strengthening Canada's health care system to meet the needs of Canadian families, and keeping Canada on the path to building a fairer, more inclusive country that reflects the priorities of Canadians.

With the passage of the Act, the following priorities will be implemented:

- Immediate down payment on 2017–18 funding for home care and mental health services to provinces and territories that have accepted the federal offer of $11 billion over 10 years;

- Establishment of the Canada Infrastructure Bank, an arm's-length organization that will work with provincial, territorial, municipal, Indigenous and private sector investment partners to transform the way infrastructure is planned, funded and delivered in Canada. The Canada Infrastructure Bank will be responsible for investing at least $35 billion in revenue-generating infrastructure projects that are in the public interest, and attracting private sector capital to those projects so that more infrastructure can be built across Canada;

- Expansion of Employment Insurance (EI) benefits to offer more flexibility for families with different needs by allowing parents to choose to receive EI parental benefits over an extended period of up to 18 months, and allowing women to claim EI maternity benefits up to 12 weeks before their due date, if they so choose;

- Greater support for Canada's veterans and their families to support a successful transition from military to civilian life, including the creation of a new Education and Training Benefit, and greater assistance for the families of disabled veterans;

- Simplification of the existing system of tax relief for caregivers by replacing three existing tax credits with the single Canada Caregiver Credit, which will better support those who need it most, apply to caregivers whether or not they live with their family member, and help families with caregiving responsibilities;

- Expansion of the range of courses eligible for the Tuition Tax Credit to include occupational skills courses that are undertaken at a post-secondary institution in Canada. In addition, the full amount of bursaries received for such courses would qualify for the scholarship exemption (where conditions are otherwise met);

- Support for a Pan-Canadian Artificial Intelligence Strategy to retain and attract top academic talent, and to increase the number of post-graduate trainees and researchers studying artificial intelligence and deep learning; and

- Strengthening of the Parliamentary Budget Office (PBO) by making it truly independent, recasting the head of the PBO as an officer of Parliament, supported by a team that is separate from the Library of Parliament, and with the authority to report directly to Parliament.

Quote

"I am pleased to see the implementation of this next phase of our government's long-term plan for growth and a strong middle class. By making these smart and responsible investments, we will ensure that all Canadians can succeed in the economy of tomorrow, with good, well-paying jobs and opportunities."

– Bill Morneau, Minister of Finance

Department of Finance Canada. June 22, 2017. Canada to Chair 2017 Commonwealth Finance Ministers Meeting

Ottawa, Ontario – The Government of Canada is continuing to build confidence in the middle class by deepening our engagement with other countries around the world and focusing on key partnerships that will help build an economy that works for all Canadians. Working towards this goal, Finance Minister Bill Morneau will chair the 2017 Commonwealth Finance Ministers Meeting (CFMM) in Washington, D.C., this October.

As the Commonwealth's third largest economy and a member of the G7 and G20, Canada is committed to contributing to global growth prospects that will lead to greater fairness and prosperity for Canadians and people around the world.

The Government of Canada's approach to creating long-term growth that works for the middle class and those working hard to join it has received international recognition and complements the theme of this year's CFMM, which is Advancing Jobs and Resilience through Innovation.

The CFMM will bring together 52 Commonwealth countries to discuss common economic challenges and opportunities. The meeting will take place on the margins of the Annual Meetings of the International Monetary Fund and World Bank Group, October 13-15, 2017. The CFMM date and other details will be announced in the coming months.

Quote

"I am proud that Canada has been asked to chair this meeting and to share our approach of creating the kind of economic growth that works to strengthen our middle class. Given this time of rapid global change, it is important that all countries work together to address our shared challenges and seize new opportunities. Above all, it is critical that the benefits of the growth we create in Canada and around the world are widely shared."

- Bill Morneau, Minister of Finance

NAFTA

The Globe and Mail. 23 Jun 2017. No need for a ‘Plan B’ for NAFTA: Trudeau

MARK RENDELL

With North American free-trade agreement renegotiation talks only months away, Prime Minister Justin Trudeau said he is “100 per cent” confident there will still be a deal in place in a year’s time.

Speaking at a public event hosted by The New York Times in Toronto on Thursday, Mr. Trudeau emphasized that “there’s no need for a Plan B” when it comes to negotiating the trade deal. That’s despite dealing with a mercurial U.S. President, who threatened to tear up NAFTA as recently as March, before reportedly changing his mind following a phone call from Mr. Trudeau.

“NAFTA has been improved a dozen times over the years, and we will do it again to update it to what the challenges we’re facing now are,” Mr. Trudeau said.

The Prime Minister said that while he and President Donald Trump differ on many issues, the President is open to reasonable arguments.

“I highlighted the fact, fairly straightforward I thought, that in any trade deal, particularly one 25 years old, there has been certain momentum … and that to terminate it suddenly would be far more disruptive than renegotiating it, even if theoretically one could imagine a much better deal some time down the road,” Mr. Trudeau said of his phone call with Mr. Trump. “There was an openness to that.”

The sense of optimism about a successful NAFTA renegotiation is shared by David Jacobson, who served as the U.S. ambassador to Canada from 2009 to 2013 and is now the vice-chair of BMO Financial Group.

“Nobody can give you a guarantee, but I am confident it will work out because it is in the best interests of all of the parties involved that it work out,” Mr. Jacobson told The Globe and Mail after speaking at the Institute of Corporate Directors’ national conference in Toronto on Thursday.

He stressed, however, the timeline to secure a successful renegotiation is tight, particularly as Mexico heads into an election year in 2018.

“President [Enrique] Pena Nieto’s party, who will be the ones who are negotiating [NAFTA], is not going to want to be perceived, as the election approaches, as making compromises with the Trump administration, because the other side will make much of it.”

Revamping a major trade deal in five months – between the expected August start date and the end of the year – “would be a record,” Mr. Jacobson said.

However, the fact it follows on the heels of the extensive TransPacific Partnership negotiations, scuttled by the Trump administration earlier this year, could expedite the process, he added. Many of the issues that were hashed out in the TPP – electronic commerce, intellectual property rights, environmental protection – are likely to form the core of the NAFTA renegotiation.

“I would be surprised if when people sit down to negotiate, particularly when they’re under some time pressure, if they aren’t going to look back and say, ‘Well gee, we spent three years doing this, let’s at least take a look,’” Mr. Jacobson said. A number of the U.S. government bureaucrats who worked on the TPP deal will be on the NAFTA renegotiation team, even if the top political leadership has changed, he added.

Despite the confidence expressed about NAFTA, Mr. Trudeau did take a harder view of other pressure points between the two countries.

“We’re not reopening and renegotiating Paris, that’s simply not on the table,” Mr. Trudeau said of the Paris climate accord, which the United States pulled out of earlier this month. He also took objection to the U.S. investigation into national security implications of the Canada-U.S. steel trade.

“I made this point directly to the President, that Canada has no business being on a list of possible national security concerns,” Mr. Trudeau said.

REUTERS. Jun 22, 2017. Canada prime minister says steel exports not U.S. security threat

OTTAWA (Reuters) - Prime Minister Justin Trudeau on Thursday dismissed the idea that Canadian steel exports posed a national security threat to the United States and expressed confidence Canada would escape any punitive measures.

The U.S. administration of President Donald Trump is probing whether foreign-made steel imports pose a risk. The investigation is almost complete, officials say.

Trudeau told a public event in Toronto it was "just silly" to imagine Canadian exports were a threat to the United States, given how closely the two nations' militaries and security forces cooperated.

"I made this point directly to the President, that Canada has no business being on a list of possible national security concerns and I am confident we're moving in the right direction on that," he said. The two leaders spoke last Friday.

Foreign steel companies are concerned the probe may be aimed at shoring up American producers and cutting out foreign competition.

Reuters reported in March that Canadian officials fear any U.S. action against the highly integrated steel industry could result in major job losses.

(Reporting by David Ljunggren; Editing by Bernard Orr)

INTERNATIONAL TRADE

Trade Commissioner Trade. 23/06/2017. Canadians Diversifying Export Markets

Countries don’t trade; firms do and recent data analysis shows that while the United States remains important, Canadian businesses are increasingly diversifying their markets.

Information on bilateral trade between countries may be the norm, but businesses are actually the ones doing the trading and statisticians worldwide—including Statistics Canada—are increasingly recognizing that fact by producing and analyzing more data about the firms that buy and sell beyond their countries’ borders.

It is widely‑known that the U.S. accounts for a large majority of Canadian merchandise exports—more than 76 percent—of total exports by value in 2016. The U.S. market is even more important in terms of the number of exporters. In 2016, 81.4 percent of exporting firms were selling to the U.S., and more than two‑thirds of those—mostly small and medium‑sized enterprises (SMEs)—exported only to the U.S..

Destinations with Largest Increases in Number of Exporters

(excluding the U.S.)

Data: Statistics Canada, Trade by Enterprise Characteristics

Source: Office of the Chief Economist, Global Affairs Canada

More extensive analysis of data collected for the 2010‑2016 period, provides evidence that Canadian businesses are increasing selling to markets other than the U.S.. Between 2010 and 2016, the number of firms exporting to non‑U.S. markets increased, with China, the United Arab Emirates, and Vietnam witnessing the largest increases in numbers of Canadian exporters.

In 2016, 43,255 enterprises in Canada exported goods, according to recently‑released data by Statistics Canada. That’s 667 fewer Canadian businesses exporting than in the previous year. The figure represents a decline of 1.5 percent spread across numerous sectors, but a 6.5 percent increase from 2010, the first year for which the information is available.

Of the 43,255 exporters in 2016, the majority—97.4 percent—are SMEs (based on the widely‑accepted definition of SMEs as firms with fewer than 500 employees). These SMEs account for 40.7 percent of Canadian merchandise exports by value; the 1,129 large firms (those with 500 or more employees) which make up only 2.6 percent of the total number of exporters, by contrast, account for nearly 60 percent of the value of Canadian goods exports.

The Upshot

While the U.S. retains its dominant position as Canada’s most important trading partner, Canadian companies are increasingly diversifying their export markets. More extensive data analysis is providing an increasingly nuanced view of Canadian exports.

HOUSING BUBBLE

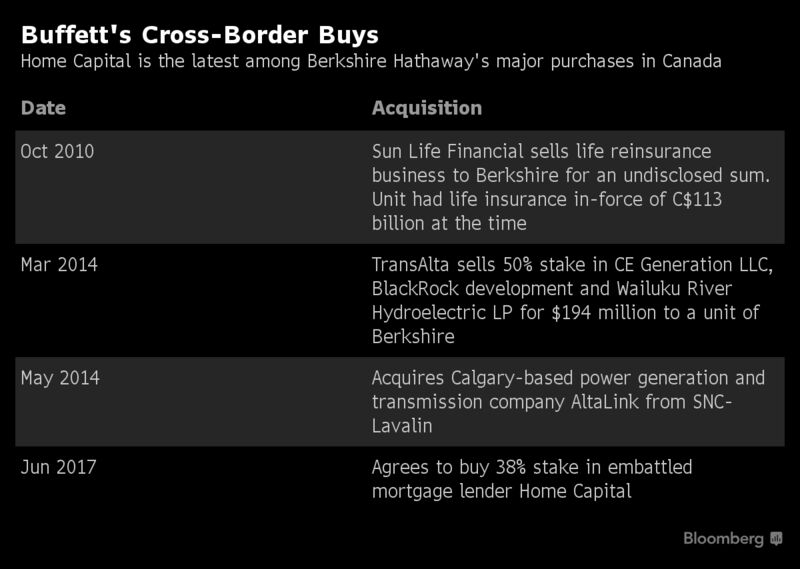

The Globe and Mail. 23 Jun 2017. How Warren Buffett struck Home Capital handshake deal in three days

JAMES BRADSHAW

JACQUELINE NELSON

ANDREW WILLIS

CHRISTINA PELLEGRINI

Investing guru says short e-mail from Canadian banker sparked his interest in troubled mortgage lender Legendary value investor Warren Buffett’s interest in rescuing Home Capital Group Inc. was piqued by an e-mail from 82-yearold Don Johnson, a Canadian banker who sends his thoughts to the investing guru now and then.

“This one wasn’t long, but it was to the point and that got my interest,” Mr. Buffett, a fellow octogenarian at 86, told The Globe and Mail by telephone from his office in Omaha, Neb.

After that, a deal in which a subsidiary of Mr. Buffett’s Berkshire Hathaway Inc. is poised to invest as much as $400-million into troubled Canadian mortgage lender Home Capital came together at breakneck speed – from first contact to a handshake deal in three days flat. Berkshire arrived late on the scene, where an array of financial firms were circling, catching even sophisticated financial players tracking the process by surprise. Mr. Buffett said he’s bullish on Canada in general, though he insists he has no fixed expansion plans for the country, and no particular insight into the direction of the Canadian housing market. Rather, he figured that by lending his firm’s name to the struggling alternative mortgage provider, he could shore up faith in its stability and have a shot at healthy long-term returns, while collecting steady interest payments over the next year.

“I really thought we could bring something to the party in addition to money in restoring confidence,” Mr. Buffett said.

The chair of Home Capital’s board, Brenda Eprile, hopes the investment “represents a turning point” for the company, which has been hammered by a crisis of market confidence and a run on deposits since it ran afoul of securities regulators over a failure to disclose concerns about mortgage fraud inside its business. » It soon became clear to directors that the company needed a reputable “sponsor” to burnish its battered reputation. Berkshire Hathaway is set to become Home Capital’s largest shareholder through a two-stage agreement that could give it a 38-per-cent equity stake at a significant discount if investors give the green light at a September vote.

Berkshire also signed on to provide a new $2-billion line of credit with slightly less onerous terms than the emergency loan from the Healthcare of Ontario Pension Plan (HOOPP) that has kept Home Capital afloat since April.

Eventually, Home Capital hopes to rebuild its portfolio of guaranteed investment certificates (GICs) as its core funding source. Home Capital’s stock soared 27 per cent to $19 a share on Thursday as shareholders embraced the news.

Berkshire must hold the Home Capital shares for at least four months. Mr. Buffett claims he didn’t even know that – “it must have been something the lawyers stuck in,” he said – and insists Berkshire is here to stay.

“I can tell you, we have no intention whatsoever of getting out in four months or eight months or 12 months,” he said.

In fact, Mr. Buffett could move deeper into the market.

While he waits for his investment to mature, he will learn more about Home Capital’s competitors and might explore opportunities for further acquisitions. “Six months from now or a year from now, as we see how this develops, you always think about that in any industry. But I have absolutely no grand plan for now,” Mr. Buffett said.

He added: “I don’t rule out anything in the future, either.”

In the month since the worst of the panic subsided, Home Capital refreshed its board, bringing on director Alan Hibben to replace retiring founder Gerald Soloway.

The company also tapped financial advisers at RBC Dominion Securities Inc. and BMO Nesbitt Burns Inc. to evaluate its options.

Investment bankers worked the phones, approaching potential investors and processing non-disclosure agreements for more than 70 interested parties granted access to a confidential data room. The names of some private-equity firms eyeing the lender began to leak into the market, with Toronto-based Onex Corp. and Brookfield Business Partners LP among the potential bidders. But none of the offers that were tabled proved attractive.

Then came the investment pitch via e-mail from Mr. Johnson, a veteran at Bank of Montreal. He reminded Mr. Buffett of their meetings over the past few decades, attaching a photo to the e-mail from an encounter in Omaha, and passed along a colleague’s contact information.

Mr. Buffett “did some thinking on it” with one of his lieutenants, Ted Weschler, and on June 12, they made their move. They sent a formal, no-conditions offer on June 13, and Mr. Weschler was dispatched to Toronto to discuss it. He reported back to Mr. Buffett that he was impressed with Home Capital’s directors.

True to Berkshire’s style, there wasn’t much negotiating, though the two sides did have to tweak some specific terms to fit Canadian laws and regulations, which Mr. Buffett was studying on the fly. Mr. Weschler “went up and just explained what we would do. And then it was up to them,” Mr. Buffett said.

By June 14, the two sides had agreed in principle.

“We’ve bought a lot of entire businesses here with what would look to a typical lawyer or investment banker as being a very peculiar way of doing due diligence,” Mr. Buffett said. “But, essentially, we’ve got our own way of evaluating facts and sometimes we make mistakes. And hopefully our batting average is decent over time. It’s not conventional.”

There were good reasons to move quickly. Home Capital is still trying to narrow its shortlist and hire a full-time chief executive officer – a role it hopes to fill by July. Mr. Buffett hopes it will be easier “getting him or her to join the place” with “an anchor shareholder like Berkshire.”

Home Capital also had concerns over staff morale. “It’s very difficult if you’re coming to work every day and you’ve got a bunch of guys chirping about your stock going to zero,” Mr. Hibben said, referring to shortsellers betting against the company.

The deal was announced just after 11 p.m. on Wednesday night, and in Shanghai, where it was already late morning, Hugo Chan was in shock. Mr. Chan, whose investment firm Kingsferry Capital bought up Home Capital shares after the share price plunged in late April, was surprised Mr. Buffett’s massive firm would get involved in such a relatively small investment. But he approves of the pact.

“In the short run, yeah, it’s a big dilution. But at the same time, I think with the support of Berkshire, Home Capital will just have enormous potential to emerge into a more profitable business,” he said.

The deal may seem like pocket change for Berkshire Hathaway, a financial juggernaut with nearly $100-billion (U.S.) available to invest. But at its core, the strategy is simple.

“Guys like that like to make money and so I suspect that was part of their motivation,” Mr. Hibben said.

Home Capital expects to seal further asset sales and deals in the near future and will use the Buffett name to woo depositors. At its peak, the company was collecting between $25-million (Canadian) and $35-million in deposits a day, before confidence in the firm evaporated and jittery investors began pulling their money.

Mr. Hibben hopes to return to accepting roughly $30-million a day.

If they’re successful, “it’s not victory, but it is certainly going in the right direction,” he said.

The Globe and Mail. Jun. 22, 2017. The nuts and bolts behind Home Capital’s deal with Berkshire Hathaway

CHRISTINA PELLEGRINI - CAPITAL MARKETS REPORTER

Warren Buffett doesn’t come cheap. Just ask Home Capital Group Inc.

His Berkshire Hathaway Inc. has agreed to indirectly buy $400-million of Home Capital’s shares – at a steep discount to the current trading price – and provide a new $2-billion line of credit on slightly better terms than the emergency loan the Toronto-based mortgage lender received in April.

Here’s how the financing will work.

The equity portion of the deal is broken up into two chunks.

Berkshire, through subsidiary Columbia Insurance Co., will make an initial investment of $153.2-million to acquire more than 16 million shares of Home Capital, which represents a stake of nearly 20 per cent in the company. Each share will be issued at $9.55, which is about half of Thursday’s closing price of $19.

Home Capital says the discount is not as large as it seems, because Berkshire actually made its final offer on June 13. The shares closed at $11.30 that day. Since then, the company announced a major asset sale to raise cash and stabilize its financial position and reached a settlement in a regulatory case with the Ontario Securities Commission. Both moves caused the share price to rise.

While such a stock sale would normally be subject to a shareholder vote, Home Capital is trying to bypass this and speed things up by relying on an infrequently-used clause in the Toronto Stock Exchange’s company manual called the “financial hardship exemption.”

Home Capital expects the TSX will approve its proposed use of the exemption after five business days, in which case it will close on June 29.

Berkshire has agreed to make another investment – also through Columbia – of $246.8-million to buy another 24 million shares of Home Capital at $10.30 a share. This deal, however, requires a green light from investors, which will be sought at a special meeting in September.

If both transactions are completed, Berkshire will own a stake of almost 39 per cent in Home Capital at an average price of $10 a share. Private placements such as these have to be held for at least four months.

Berkshire is also lending Home Capital $2-billion to repay its existing credit facility, which was given in April by the Healthcare of Ontario Pension Plan (HOOPP).

It is slightly cheaper than the HOOPP loan: There is no upfront commitment fee. The interest rate on outstanding balances will decline to 9.5 per cent from the current 10 per cent, while the standby fee on undrawn funds will decrease to 1.75 per cent from the current 2.5 per cent.

Once Berkshire makes its initial investment in Home Capital, these amounts will drop to 9 per cent and 1 per cent, respectively.

The Globe and Mail. 23 Jun 2017. Investors who choose to follow the lead of Warren Buffett and buy into Home Capital are not making the same bet.

DAVID BERMAN

There is one thing to keep in mind if you are considering investing in Home Capital Group Inc.: You are not Warren Buffett.

Mr. Buffett, a legendary investor who attracts copycats with his every move, has agreed to provide financial backing to the beleaguered Canadian mortgage lender, in the form of a $400million equity investment and a $2-billion line of credit.

Investors love it. Home Capital shares jumped 27.2 per cent on Thursday, closing at $19 – for a gain of 225 per cent from the stock’s low point in early May.

The impressive rebound suggests renewed confidence in Home Capital, two months after its share price collapsed amid fleeing deposits that raised questions about the company’s ability to survive.

However, while Mr. Buffett’s financial backing appears to be a wildly bullish argument in favour of buying Home Capital shares, the deal he has struck cannot be replicated by other investors: If you choose to follow Mr. Buffett, you are not making the same bet.

The deal resembles the one Mr. Buffett struck with Goldman Sachs Group Inc. during some of the darkest days of the financial crisis last decade. In September, 2008, Mr. Buffett’s Berkshire Hathaway Inc. provided a much-needed cash infusion to the Wall Street investment bank.

Mr. Buffett bought $5-billion (U.S.) worth of preferred shares yielding 10 per cent annually. He also got warrants that would give him the right to buy 43.5 million Goldman Sachs common shares at $115 each (or $5-billion in total) – giving him an easy profit if the shares rose above this price. And they did. But investors couldn’t piggyback on this exact deal. It was a made-for-Buffett deal.

His agreement with Home Capital, also through Berkshire Hathaway, has similar qualities. Yes, Mr. Buffett will become a significant shareholder in the mortgage lender if the deal goes through, which speaks volumes about the perceived quality of the company’s loan book.

But Mr. Buffett is getting a few things here that new investors are not. For one, his first investment of about 16 million shares is priced at just $9.55 a share.

That is a 15-per-cent discount to the five-day volume-weighted average price, as Home Capital’s press release helpfully points out – and it is a dazzling 36 per cent below Wednesday’s close.

Based on Thursday’s closing price of $19, new investors who decide to ride on Mr. Buffett’s coattails are buying shares that are already about 100 per cent more expensive than Mr. Buffett’s sweetheart deal.

Mr. Buffett is also getting a steep discount on a second investment of about 24 million Home Capital shares. These will be priced at $10.30 each, or 31 per cent below Wednesday’s close.

Berkshire Hathaway has also agreed to extend a $2-billion line of credit to Home Capital that will pay an interest rate of 9.5 per cent on drawn funds. Try getting that on a fixed-income investment.

This deal is good for Mr. Buffett, who stands to double his equity investment the minute the deal goes through (expected later this month). It’s also good for Home Capital, which has found a highprofile investor, a new financial lifeline and the best confidence booster it could hope to get.

But for new investors hoping to tag along with Mr. Buffett, the deal is bittersweet. Home Capital is on safer ground and you might do fairly well if you hold on to your shares for the long run. Tha Oracle, however, is a giant step ahead of you.

The Globe and Mail. 23 Jun 2017. Why Buffett is a bull on Canada. Warren Buffett’s warm feelings for Canadian investments date back to his childhood.

ANDREW WILLIS

Just don’t ask the Oracle of Omaha where house prices will be in 12 months. The legendary value investor said he made a potential $2.4-billion debt-andequity investment in Home Capital Group Inc., the country’s largest alternative mortgage lender, “with no specific view on whether home prices are going to be up 10 per cent or down 10 per cent in a year’s time. No one knows that.”

In a deal that combined the folksy charm and financial acumen that has made him one of the world’s wealthiest men, the chairman and CEO of Berkshire Hathaway Inc. said in an interview with The Globe and Mail that he first considered backing Home Capital, which came close to collapse in early May, after getting an e-mail from a Bank of Montreal executive who occasionally passes along interesting opportunities.

That note was a seed landing in fertile soil. Mr. Buffett’s warm feelings for Canadian investments date back to his childhood – he owned shares in miner Noranda as a 13-year-old. The upbeat outlook was reinforced in May when Mr. Buffett listened to Prime Minister Justin Trudeau and Finance Minister Bill Morneau speak about Canada’s prospects at a Microsoftsponsored CEO summit in Seattle.

“I always have been enthusiastic on Canada generally, but I felt even more so after talking to them,” Mr. Buffett said, adding in a can’t-make-this-up moment that he was impressed by the country’s Prime Minister after watching Mr. Trudeau “win that prize fight” – his famous charity boxing match with Senator Patrick Brazeau in 2012 – on YouTube.

The attraction of Home Capital was simple, to hear Mr. Buffett tell it. This was a solid company facing a lapse in confidence and a run on the bank. Mr. Buffett said: “Financial institutions trade on confidence, and we believed Berkshire could bring something in terms of confidence, to improve an already secure situation.”

Home Capital’s clients are folks who can’t borrow from banks, including immigrants and the self-employed, and Mr. Buffett said he and his colleagues were impressed by company’s ability to lend to homeowners who pay back mortgages and avoid deadbeats.

Berkshire also sees an opportunity to expand Home Capital’s business, potentially through acquisitions, in a fragmented market for alternative mortgages.

“A lot of people who don’t fit the cookie-cutter approach to borrowing are perfectly decent credits,” he said. Mr. Buffett, who is famously paid just $100,000 (U.S.) to run Berkshire, added: “I’m not sure whether I’d qualify very well on loans, when you get right down to it … if you look at my salary.”

While Mr. Buffett’s thesis for investing in Home Capital started with an optimistic view of Canada – with a strengthening economy and inflow of immigrants – and a positive take on the company’s credit culture and prospects, it was Berkshire’s ability to make quick decisions that sealed this deal.

More than 70 suitors looked at Home Capital’s books after the Toronto-based lender was effectively put up for sale in May. Berkshire’s team went from a first meeting to a handshake deal in three short days, warp speed in deal-making terms.

“Our style is never to really haggle over price,” said Mr. Buffett, who can draw on the deep financial resources within Berkshire to fix balance sheet woes at Home Capital – the conglomerate has some $90-billion (U.S.) in cash. “We’ve bought a lot of businesses. … We’ve got our way of doing things. Hopefully, our batting average is decent over time.”

Mr. Buffett’s batting average at Berkshire has turned a theoretical $1,000 investment when he arrived at the company in 1964 into a stake worth more than $10-million today. For Berkshire, the Home Capital transaction is a small one – but it should nevertheless enhance that track record. Assuming all parts of the deal close, he has already turned a paper profit of $360million on the Home Capital shares he has agreed to buy.

The Globe and Mail. 23 Jun 2017. Berkshire to the rescue: How Home Capital’s deal works

CHRISTINA PELLEGRINI

His Berkshire Hathaway Inc. has agreed to indirectly buy $400-million of Home Capital’s shares – at a steep discount to the current trading price – and provide a new $2-billion line of credit on slightly better terms than the emergency loan the Toronto-based mortgage lender received in April.

Here’s how the financing will work.

The equity portion of the deal is broken up into two chunks.

Berkshire, through subsidiary Columbia Insurance Co., will make an initial investment of $153.2-million to acquire more than 16 million shares of Home Capital, which represents a stake of nearly 20 per cent in the company. Each share will be issued at $9.55, which is about half of Thursday’s closing price of $19.

Home Capital says the discount is not as large as it seems, because Berkshire actually made its final offer on June 13. The shares closed at $11.30 that day. Since then, the company announced a major asset sale to raise cash and stabilize its financial position and reached a settlement in a regulatory case with the Ontario Securities Commission, Both moves caused the share price to rise.

While such a stock sale would normally be subject to a shareholder vote, Home Capital is trying to bypass this and speed things up by relying on an infrequently-used clause in the Toronto Stock Exchange’s company manual called the “financial hardship exemption.”

Home Capital expects the TSX will approve its proposed use of the exemption after five business days, in which case it will close on June 29.

Berkshire has agreed to make another investment – also through Columbia – of $246.8million to buy another 24 million shares of Home Capital at $10.30 a share. This deal, however, requires a green light from investors, which will be sought at a special meeting in September.

If both transactions are completed, Berkshire will own a stake of almost 39 per cent in Home Capital at an average price of $10 a share. Private placements such as these have to be held for at least four months.

Berkshire is also lending Home Capital $2-billion to repay its existing credit facility, which was given in April by the Healthcare of Ontario Pension Plan (HOOPP).

It is slightly cheaper than the HOOPP loan: There is no upfront commitment fee. The interest rate on outstanding balances will decline to 9.5 per cent from the current 10 per cent, while the standby fee on undrawn funds will decrease to 1.75 per cent from the current 2.5 per cent.

Once Berkshire makes its initial investment in Home Capital, these amounts will drop to 9 per cent and 1 per cent, respectively. Home Capital Group (HCG) Close: $19, up $4.06

Berkshire Hathaway (BRK.B) Close: $168.32 (U.S.), down $1.30

The Globe and Mail. 23 Jun 2017. Home Capital GICs: A new layer of confidence. With Buffett’s Berkshire Hathaway offering financial support, the company may not need to offer premium rates for long

ROB CARRICK

Warren Buffett is widely seen as one of the investing world’s best judges of companies offering value.

Capital enough to invest in its shares, then there’s less reason to hold back on the company’s GICs.

That 3.25-per-cent, five-year guaranteed investment certificate that Home Capital’s selling under its Oaken Financial brand? Get it while you can. With Mr. Buffett’s Berkshire Hathaway helping to financially support Home Capital, the company may not need to offer premium rates like this for long.

I argued against buying Home Capital’s GICs in a May 25 column after seeing how freaked out investors were about the company’s struggles following a run-in with regulators that has since been settled. Some people spoke of cashing in Home Capital GICs, even though combined principal and interest are protected by Canada Deposit Insurance Corp. to a maximum of $100,000 per eligible deposit.

Getting financial support from Mr. Buffett’s holding company is a big win for Home Capital. The deal, which has yet to be finalized, seems calculated to soothe investor concerns about buying a supposed safe-investment product from a troubled company. There’s no question that with Mr. Buffett on board, people buying GICs from Home Trust, Home Bank or Oaken Financial now have an additional reason for confidence beyond CDIC’s trustworthy backing.

That reason is Mr. Buffett’s acumen. The man is a legendary investor who has made plenty of scandal-free wealth over the years for Berkshire Hathaway shareholders. Mr. Buffett is so divorced from the usual investment industry spin and salesmanship that he encourages people to buy low-cost index funds instead of picking their own stocks like he does.

Mr. Buffett has made mistakes, as anyone who manages money does from time to time, but he’s widely seen as one of the investing world’s best judges of companies offering value. If he’s willing to buy shares of Home Capital and provide a line of credit to the company, that’s a significant endorsement.

The Home Capital shares that Berkshire Hathaway is buying were priced at a steep discount to the trading price. This demonstrates how Mr. Buffett has found an angle on profiting from a Home Capital rebound that isn’t available to everyone. You could buy some Home Capital shares yourself, but they jumped 12.5 per cent in the first 30 minutes of trading on Thursday on news of the Berkshire deal and were already up about 62 per cent in the past month.

Negative news about Home Capital in the future would send those shares right back down again. So consider those GICs from Oaken, Home Trust and Home Bank. The latter two outfits deal through deposit brokers or investment dealers and offer slightly lower rates than Oaken, which deals directly with investors. In the Home Capital organizational chart, Oaken GICs are protected through the CDIC membership of Home Capital or Home Trust. Oaken itself is not a CDIC member.

Oaken offered 2.75 per cent for a one-year GIC as of early Thursday, Home Bank offered 2.55 per cent and Home Trust 2.5 per cent. Compared with Oaken’s 3.25 per cent over five years, Home Bank offered 3 per cent and Home Trust 2.95 per cent. Posted rates from the big banks were a bit less than 1 per cent for one year, and no more than 1.6 per cent for five years. GICs are basically pointless if this is all you’re getting.

When it introduced its current rates a couple of weeks ago, Home Capital was desperate to attract money from investors to sustain its business of lending out money to so-called alternative mortgage clients – entrepreneurs and immigrants, for example. These are premium rates that beat the competition cleanly, while also addressing the main reason for being wary of GICs today – returns lag or barely keep up with inflation.

Oaken’s five-year GIC rate is a little more than double the mostrecently reported 1.6-per-cent inflation rate. That said, the sweet spot in Oaken’s GIC offerings just might be the three-year term at 3.05 per cent. You still hit that elusive 3-per-cent threshold, but you only have to lock up your money for three years.

The Berkshire deal destresses the experience of investing in Home Capital GICs a lot. But even with Mr. Buffett on board and CDIC protection in place, there could still be a certain level of drama associated with the company. Continue to avoid Home Capital if you’re investing in GICs to escape the financial headlines.

The Globe and Mail. Jun. 22, 2017. Investment advisers regaining confidence in Home Capital savings products

CLARE O’HARA - WEALTH MANAGEMENT REPORTER

As Warren Buffett swoops in to save the day for Home Capital Inc., a surge of renewed confidence has been restored throughout the investment community.

Earlier this year, Home Capital was seen as an attractive mortgage lender that was able to offer better-than-average interest rates for both high-interest savings accounts (HISAs) and guaranteed investment certificates (GICs). But after regulatory concerns surfaced within their mortgage business, brokers at other financial institutions grew wary and a flood of investment dollars was immediately pulled from the company’s HISAs.

Over the past several months, balances in those accounts dropped to approximately $112-million from $1.9-billion.

Total GIC deposits, including Oaken and broker GICS, stood at approximately $12.03-billion and Oaken savings accounts stood at approximately $142-million, as of Wednesday.

In hopes of drawing in new investment dollars, Home Capital has remained aggressive in both the HISA and GIC markets offering attractive interest rates that at times were more than double what Canadian banks were offering.

Currently, Oaken Financial GICs are offering 2.75 per cent for a one-year GIC, while Home Trust is slightly less at 2.5 per cent (Home Trust GICs are sold through the adviser channel while Oaken GICs are sold directly to investors).

Despite aggressive rates and the security of Canadian Deposit Insurance Corp. (which insures the majority of deposits under the $100,000 threshold) many advisers were hesitant to take on the risk of their clients money being tied up in the case Home Capital had to shut its doors. Several financial institutions – including Scotia Wealth Management – placed a capped limit of $100,000 of Home Capital product an adviser could sell to a client. (That capped limit still remains for Scotia wealth advisers.)

Now, with Berkshire Hathaway agreeing to indirectly acquire $400-million of Home Capital’s common shares, confidence is being restored and many financial advisers – and their clients – may be more willing to turn to the mortgage lender for attractive cash options.

Here is what investment advisers are saying about the potential backing of Berkshire Hathaway in Home Capital:

Brian Evans, chair of the Registered Deposit Brokers Association and head of Brian J. Evans Financial Services

“We never stopped recommending Home Capital products because we were pretty confident that there would not be a failure in the company but there were some clients who chose to stay clear of potential risks with their deposit products. Now I wouldn’t be surprised if some of these same clients would be looking at Home Capital in a different light than they did a few weeks ago. For both the retail investor, and the deposit brokers, seeing an investment partner, like Berkshire, come on-board adds strength and confidence to the firm. We know this is the start of the anticipated resolution to the matter.”

Darren Coleman, portfolio manager with Raymond James

“This news about Warren Buffett buying in brings a huge vote of confidence for deposit holders. Not only is there an injection of capital into the company, but now there is also a steady hand at the wheel for deposit holders to see. Warren Buffett is one of the most highly respected investors in the industry and has obviously done the due diligence to make an investment in the company. This would make me very comfortable as an investor now. But what will really be interesting is whether the company will drop the interest rates back down. The company ramped up interest rates to draw in funds … if the perception of risk goes down then it would make sense that the rates would follow suit.”

Brad Brain, portfolio manager at Aligned Capital Partners Inc.

“Unquestionably, this is good news. I am a long-term Buffettophile and am very familiar with his philosophy and his previous transactions. This is exactly in his circle of competence and he doesn’t work with management teams that he doesn’t have full faith and confidence in.”

Darren Farwell, director of wealth management with The Farewell Group at Scotia Wealth Management

“There is no question that as of today, with a strong corporate sponsor like Berkshire Hathway, there is a higher level of comfort for any Home Capital depositors and stakeholders. But, for these kinds of investment products, I am reluctant to expose my clients to that unnecessary kind of risk in a product that has so little differentiation in a rate of return.”

The Globe and Mail. 23 Jun 2017. Foreign buyers are a limited part of Montreal housing: CMHC

NICOLAS VAN PRAET

MONTREAL - Foreign buyers are pushing into Montreal’s real estate market in increasing numbers but they remain a limited part of the property picture, data from Canada’s national housing agency confirms.

About 235 foreign buyers snapped up property in the Montreal area from January to April this year, a 40-per-cent jump from the first four months of 2016, the Canada Mortgage and Housing Corp. (CMHC) said in a research note Thursday. That continues an upward trend from last year as a whole, when there were 60 per cent more buyers than in 2015.

The increases are large in percentage terms and signal a continued interest by people outside Canada in Quebec’s largest city. But they are small when considered as part of the wider market, with 235 buyers representing just 1.8 per cent of all residential real estate transactions.

“A slight shift in demand from Vancouver to Montreal may have occurred after the introduction of the foreign buyers’ tax on housing in Vancouver” in August, 2016, the housing agency said. Given the introduction by Ontario of a similar tax in April of this year, the agency said it will continue to follow the situation closely over the coming months.

Prices in Montreal climbed 6 per cent in May compared with the same month last year and sales volume set a record for the month with 15-per-cent growth, according to the Québec Federation of Real Estate Boards. The federation says Montreal’s market is being driven by demand from local buyers in an economy with record low unemployment and low interest rates, not by foreign-based purchasers.

Buyers from the United States and France still make up the largest pool of foreign buyers in Montreal, according to the CMHC data. The housing agency said the number of Chinese buyers in Montreal more than tripled to 100 over the eightmonth span after Vancouver’s tax was introduced compared with the same span the year before.

Condominiums remained the first choice of property type for foreign investors in Montreal, the CHMC said. Chinese buyers were more inclined than buyers from the United States and France to opt for single-family homes.

BLOOMBERG. 2017 M06 23. Short-Seller Nailed Home Capital, Then Got Stung by Buffett

By Noah Buhayar and Katia Dmitrieva

- Cohodes says lender’s Berkshire deal is sign of desperation

- I’m not wrong just because Buffett shows up, Cohodes says

- Buffett Follows Goldman Model in Bailout for Home Capital

Marc Cohodes was having dinner Wednesday with a friend at the Slanted Door, an upscale Vietnamese restaurant on San Francisco’s Embarcadero, when he saw the news: Warren Buffett’s Berkshire Hathaway Inc. had just thrown a lifeline to Home Capital Group Inc.

“I said, ‘Boy, that’s interesting,”’ he remembers. “I’m surprised Berkshire Hathaway would show up in something like this.”

It was a mild reaction for an investor who’s shown time and again he’s got brass. More than anyone, Cohodes has tried to discredit Home Capital. A former hedge fund manager and veteran short seller, he began betting against the stock in 2014, publicizing his view that the Canadian mortgage provider had lax underwriting and poor management.

It didn’t take long for the wager to net returns. Two years ago, the company said it found fraudulent data in documents provided by partner brokers who submitted about C$2 billion in mortgages. The lender cut ties with them, prompting a lower profit forecast.

The troubles didn’t end there. The Ontario Securities Commission alleged in April that company executives had misled investors about the extent of the mortgage fraud. Clients began withdrawing funds from savings accounts. From its peak in 2014, Home Capital stock fell about 90 percent.

Cohodes seemed to be riding a wave of vindication. So many other investors piled into the trade that, at one point, almost two-thirds of Home Capital’s shares were sold short.

Stock Rebound

In recent weeks, though, things started to turn around. The stock began to climb on news of asset sales and partners willing to invest in the mortgage lender. The company and former executives settled the regulatory probe this month.

Then, late Wednesday, the bombshell: Berkshire agreed to take a 38 percent stake in the company for about C$400 million ($300 million) and provide a line of credit. Home Capital’s stock rocketed 27 percent on Thursday to C$19. The shares added another 43 cents as of 9:52 a.m. in Toronto.

“Partnering with an investor with the pedigree of Berkshire should go a long way in restoring confidence, particularly with depositors,” Dylan Steuart, an analyst at Industrial Alliance Securities Inc., said in a note Friday. “This transaction, combined with the recent settlement with the OSC, will likely lead to funding inflows as the smoke continues to clear.”

Few investors would want to be on the opposite side of such an economic force. But Cohodes isn’t backing down. He said he still thinks Home Capital’s stock could go to zero and that he continues to bet on a decline, though he won’t disclose the size of his wager.

“I may lose,” he said in a phone interview on Thursday, while pacing around his his chicken farm about an hour north of San Francisco. “It may go to C$20. It may go to C$30. But I’m in a whole lot higher. I’m willing to see more rounds.”

Desperate, Horrible

Cohodes says he takes comfort in the way the deal with Buffett was structured and believes there’s a scenario where both he and the billionaire can make money. In addition to getting discounted shares in Home Capital, Berkshire agreed to provide a C$2 billion credit line that will eventually carry a 9 percent interest rate, generating returns for Berkshire even if the lender’s shares slump. Cohodes sees the deal terms as a validation of his skepticism.

“This move shows how desperate this thing really is,” he said. “If it weren’t Warren Buffett’s name, it would be destroyed today, just absolutely destroyed, because it’s that horrible of a deal.”

Home Capital declined to comment about Cohodes, but said in its statement Wednesday that the Berkshire investment was a “very strong validation and endorsement.” In the same announcement, Buffett added that Home Capital was a good bet because of its “strong assets, its ability to originate and underwrite well-performing mortgages, and its leading position in a growing market sector.”

Buffett, 86, has spent decades building Berkshire’s reputation as a source of capital for troubled companies. During the 2008 financial crisis, he plowed billions into Goldman Sachs Group Inc. and General Electric Co. He also propped up Bank of America Corp. when that lender ran into trouble in 2011. In exchange for putting money and his reputation on the line, he’s negotiated preferential returns for Berkshire shareholders.

As with those previous deals, Berkshire moved quickly with Home Capital. For Cohodes, who’s spent years digging into the mortgage lender, that’s another sign that his thesis may still be right.

“I got the goods,” he said. “I’m not wrong just because he shows up.”

BLOOMBERG. 2017 M06 23. Buffett’s Home Capital Bet Backs Turbulent Canada Housing Market

By Katia Dmitrieva

- Berkshire head supports lender as housing concerns mount

- Toronto housing market cools after record price gains

- Buffett Poised for Immediate Gain From Home Capital

Warren Buffett’s deal to back Home Capital Group Inc. does more than support a struggling mortgage lender -- it’s a vote of confidence for a housing market that everyone from investors to global ratings companies say is a bubble ready to burst.

Buffett’s Berkshire Hathaway Inc., is buying a 38 percent stake in Home Capital for about C$400 million ($300 million) and providing a C$2 billion credit line to backstop the Toronto-based lender. With the deal, the billionaire investor is wading into a housing market that’s been labeled overvalued and over-leveraged, with home prices in Toronto and Vancouver soaring as household debt hits record levels.

Naysayers “have been dissing our banks and dissing our real estate market for years because we didn’t go into the can the way that the Americans did in 2008 to ’09, and they’ve been waiting for a collapse in our markets,” said Ross Healy, chairman of Toronto-based Strategic Analysis Corp. and a Home Capital investor who bought shares when they dipped to C$6 last month. “Am I concerned about that? Nope. So thank you, Warren Buffett.”

Home Capital became a poster child for the ills in Canada’s housing market after it was accused by regulators in April of misleading investors about mortgage fraud. That sparked a run on deposits and raised concerns it would be the catalyst to bring down the housing market that organizations including Fitch Ratings Inc. and the International Monetary Fund warned was already at risk of correction.

Buffett’s equity investment and credit line for Home Capital suggest he’s not betting on a collapse anytime soon. At the same time, he’s being rewarded for the risk, buying shares at a 33 percent discount and making 9 percent interest on any tapped portion of the loan.

‘Leading Position’

“Home Capital’s strong assets, its ability to originate and underwrite well-performing mortgages, and its leading position in a growing market sector make this a very attractive investment,” Buffett said in a Home Capital statement late Wednesday night.

Buffett joins a long list of investors who have taken a look Home Capital’s assets, even amid the housing-market risk and run on deposits. The company drew interest from Onex Corp., Brookfield Asset Management Inc., Catalyst Capital Group Inc. and others, according to people familiar with the matter. Home Capital was also in discussions with Canada’s major banks about refinancing its existing line of credit with a Canadian pension fund. Home Capital this week sold a C$1.2 billion portfolio of commercial mortgages to KingSett Capital Inc., a Toronto-based private equity firm.

Buffett’s investment could only be positive in a country where risks of housing are overblown, said Alan Hibben, one of the new board members put in place in May to rescue the company. In Toronto, average home prices have rallied 130 percent in the past decade to C$863,910 last month. In Vancouver, they’re up 115 percent to C$1.1 million in the same period. Though home price gains have slowed over the past six weeks, there is little risk of a crash, Hibben said.

Home Capital is “a very attractive business here in a marketplace that has already been cooled to some extent by government policy and may be cooling a bit more,” Hibben, a former RBC Capital Markets banker, said on Bloomberg Television. “While obviously we’re very interested and looking very closely at home values -- particularly in Toronto and greater Vancouver area -- we’re not seeing this to be as dire as some commentators might see it, particularly those outside of Canada.”

Fitch seemed to mirror that view, saying that although unsustainable home prices and historically high debt make Toronto and Vancouver vulnerable to a correction, the housing system would likely not follow the housing-sparked downturn in the U.S. in 2008.

“Canadian banks are subject to rigorous oversight and regulations requiring prudent mortgage lending and underwriting standards. What’s more, credit quality for Canadian mortgage loans remains strong,” Fitch analysts led by Kate Lin said in a report Thursday. Non-prime originations in Canada account for about 10 percent of volume, compared with a pre-crisis peak of 50 percent in the U.S., according to the report.

Home Capital mortgages account for about 1 percent of the country’s home loans, but it’s one of the biggest lenders to new immigrants -- about 250,000 of whom move to Canada each year -- as well as the self-employed, first-time buyers and those with poor credit histories. It’s become a more important player in the past few years as federal mortgage regulations made it harder for these borrowers to work with banks, which now require better credit scores and charge higher rates.

Lower Arrears

Despite dealing with riskier borrowers, Home Capital has fewer loans in arrears than traditional lenders do. Non-performing loans comprised only 0.24 percent of Home Capital’s gross book, according to the company’s first-quarter results. Canadian lenders had an average arrears rate of 0.28 percent as of February, according to the Canadian Bankers Association.

Consumers holding C$1.4 trillion in total mortgage debt nationwide aren’t defaulting on their home loans even with the record levels of debt. They’ve been helped by low mortgage rates -- as low as 2 percent -- and an economy that’s growing at the fastest pace among Group of Seven countries.

Despite the boost from Buffett’s investment, the troubles aren’t over yet for Home Capital. The company still needs to find a replacement chief executive officer after Martin Reid was forced to leave the firm, and founder and former CEO Gerald Soloway retired from the role last year. Board directors said on a conference call Thursday that the search was progressing well and a new CEO would be announced in July.

High Costs

The terms of the credit facility Buffett gave are also not that much better than a C$2 billion loan Home Capital had from Healthcare of Ontario Pension Plan, said James Price, director of capital markets products at Richardson GMP Ltd. Home Capital will pay 9 percent on any drawn capital and 1 percent on the standby amount. Hibben said the company expects to tap the new line soon to pay off part of the HOOPP loan.

“Home Capital certainly can’t run their business with a 9 percent cost of capital,” Price said by phone from Toronto. “Frankly, outside of the Buffett halo, the terms don’t look that good for existing shareholders. They get significantly diluted and they get diluted at a much lower price than they’re trading at.”

The company also needs to win back depositors to inject funds into the savings accounts that back its mortgages, said Stephen Boland, an analyst at GMP Securities LP. Home Capital’s high-interest deposit levels have stabilized at about C$110 million, down from C$1.4 billion in early April. The level of guaranteed investment certificates have fallen to about C$12 billion.

“You need a stamp of approval from somebody that will hopefully bring back the agent, the broker that buys a GIC for their client,” Boland said. “Warren Buffett is certainly the biggest name. The question is: will it bring them back?”

BLOOMBERG. 2017 M06 22. Buffett’s Home Capital Deal Kicked Off by 82-Year-Old Banker

By Doug Alexander

- Banker Johnson reached out to Buffett 23 years after meeting

- BMO piques Buffett interest amid Home Capital crisis

- Buffett Follows Goldman Model in Bailout for Home Capital

Warren Buffett’s surprise investment in Home Capital Group Inc. all started with a single email from a Canadian investment banker who first met the billionaire 23 years ago.

Don Johnson, 82, an advisory board member at Bank of Montreal’s BMO Capital Markets unit, reached out to Buffett in a June 9 email, adding a photo of the two of them to remind Berkshire Hathaway Inc.’s chairman of their past connections.

“I just brought to his attention this Home Capital opportunity," Johnson said of his message to Buffett. “I informed him that BMO Capital Markets had been retained as one of the financial advisers to Home Capital, and so I sort of summarized the opportunity and put him in touch with the head of our financial institutions group."

Buffett clearly listened. The investor agreed to buy Home Capital shares at a deep discount and provided a fresh credit line for the struggling Canadian mortgage company, tapping a formula he used to prop up lenders from Goldman Sachs Group Inc. to Bank of America Corp. Berkshire will buy a 38 percent stake for about C$400 million ($300 million) and provide a C$2 billion credit line with an interest rate of 9 percent to backstop the Toronto-based lender.

Home Capital had been seeking financial stability after facing accusations by Ontario’s securities regulator in April of misleading shareholders on mortgage fraud some two years earlier. That sent its shares tumbling, accelerated deposit withdrawals and forced the firm to seek a costly emergency loan from a pension fund. Royal Bank of Canada and Bank of Montreal had been hired by Home Capital to advise on financing and other transactions.

Best Time

Johnson remembered Buffett’s criteria that the best time to consider an investment is when no one else wants to buy -- and Home Capital seemed to fit the bill. He suggested Buffett reach out to BMO Capital Markets bankers including Bradley Hardie, who heads the financial institutions group at the Toronto-based firm.

“I just opened the door, that was all," Johnson said. “I just made the introduction and he turned it over to one of his right-hand men and they contacted Brad Hardie on the Monday, right after my email on the Friday."

Buffett had already been showing interest in Canada in recent weeks. He spoke to Prime Minister Justin Trudeau and Finance Minister Bill Morneau at a CEO summit hosted by Microsoft Corp. in Seattle last month, and asked several questions about the Canadian economy, according to a person familiar with the discussions who asked not to be identified. Buffett’s other investments in the country include AltaLink LP, an Alberta utility. A Morneau spokesman later confirmed the meeting.

‘Strong Canadian Economy’

Morneau and Buffett “talked about the strong Canadian economy, the fundamental advantages of Canada as an investment destination, and the risks to the economy from mortgage debt, which, while real, are different than in the U.S.," Morneau said Thursday in a statement. The investment “is proof the system is working," he said.

Buffett didn’t immediately respond to a message seeking comment.

Alan Hibben, a Home Capital director, said Thursday in an interview at Bloomberg’s Toronto office that Berkshire’s involvement was due to "outreach" by Bank of Montreal.

“We had the company on our list for quite a while, so it wasn’t exactly inbound," said Hibben, who’s never met Buffett. “I had requested that our advisers touch base with him to see what we could do, and they did. And he came back very, reasonably quick.”

Buffett, 86, has been leaning more in recent years on his deputy investment managers, Todd Combs and Ted Weschler. Both are former hedge fund managers and were hired in the past decade to help pick stocks at Berkshire. Each runs a stock portfolio valued at about $10 billion. But they’ve also taken on special projects for the billionaire, vetting deals and serving as chairmen of some of Berkshire’s subsidiaries.

They’re also a cornerstone of Buffett’s succession plan at Berkshire. The billionaire -- who serves as the company’s chairman, chief executive officer and head of investments -- has said the deputies will one day oversee the company’s massive stock portfolio, which was valued at about $135 billion at the end of March.

Old Connection

Johnson’s connection to Buffett began more than two decades ago, when he was working on a potential Canadian deal and crossed paths with the investor. Johnson, who once was vice chairman of investment banking for the BMO Nesbitt Burns unit, stayed in touch over the years, attending one of Berkshire Hathaway’s annual meetings and seeing him in October 2007 when Buffett was a guest speaker at a fundraising dinner for the Royal Ontario Museum.

“I also invited him to my 80th birthday party, but Paul Anka was performing and he knows Paul Anka very well," said Johnson, who turned 82 on June 18.

Johnson said he feels great to be able to play a role in the deal, and reached out to Buffett as it was announced.

"I just sent Warren an email congratulating him on the decision," Johnson said. “It was a great investment for Berkshire Hathaway but it was also great for all the shareholders of Home Capital and all the stakeholders."

Not Retired

Johnson began his career in the investment industry when he joined Burns Bros. and Denton Ltd. in 1963. Over the years, he held a series of management roles and became president of Burns Fry in 1984. In 1989, he became vice chairman of investment banking for BMO Nesbitt Burns and its predecessor companies. He retired as vice chairman in 2004, but continues his involvement as a member of the advisory board of BMO Capital Markets.

“I wouldn’t say I’m retired," Johnson said. “I’m starting to slow down. I only go to the office five days a week, the other days I work from home."

AVIATION - BOMBARDIER

The Globe and Mail. The Canadian Press. 23 Jun 2017. Boeing plays down Bombardier spat, aims to sell jets to Canada

LEE BERTHIAUME

OTTAWA - A senior Boeing Co. official says the U.S. aerospace giant’s trade dispute with Montreal-based rival Bombardier Inc. is a “company-to-company issue,” and that it still hopes to sell Super Hornet jets to Canada.

Leanne Caret, the head of Boeing’s multibillion-dollar defence and space division, made the comments on the sidelines of the Paris Air Show this week, where her company was snubbed by Canadian officials.

Members of the Canadian government met F-35 manufacturer Lockheed Martin and other fighter jet makers in Paris on Monday and Tuesday, but refused to have any contact with Boeing.

Economic Development Minister Navdeep Bains specifically cited Boeing’s complaints to the U.S. Commerce Department about Canadian rival Bombardier as the reason for the cold shoulder.

Ms. Caret, however, highlighted in an interview with U.S.-based Defense News what she said was Boeing’s nearly 100-year “working relationship” with Canada and the federal government.

“This is very much a companyto-company issue that we’re working through,” she said of the dispute with Bombardier.

“I’m looking forward to continued dialogue with the Canadian government in terms of the capabilities that they need, and how our best products might be best suited.”

The comments are the first

from a senior Boeing official since the Liberal government threatened last month to scrap plans to buy 18 “interim” Super Hornets over the company’s dispute with Bombardier.

Last November, the Trudeau government announced plans to purchase the planes to temporarily fill a critical shortage of fighter jets until a full competition to replace Canada’s aging CF-18s.

The government said at the time that the Super Hornet was the only aircraft able to meet its immediate requirements, including being a mature design compatible with U.S. fighters.

But that was before Boeing lodged a complaint with the U.S. Commerce Department that alleged Bombardier was selling its C Series jet liners at an unfair price with help from federal government subsidies.

U.S. authorities are currently investigating the complaint and are expected to decide in the coming weeks or months whether to penalize Bombardier with fines or tariffs.

A government source confirmed this week that Boeing’s rivals used their meetings with Canadian officials in Paris to pitch their own jets in the event the Liberals follow through on their threat to Boeing.